Advance tax certainty for major projects (HTML)

Updated 31 March 2025

© Crown copyright 2025

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/consultations/advance-tax-certainty-for-major-projects-consultation/advance-tax-certainty-for-major-projects-html

1. Introduction

Background

Kickstarting economic growth is the central mission of the government. It is through this growth mission that the government will drive up prosperity and living standards across the UK.

The government has already made significant commitments towards its growth mission: at Autumn Budget, it announced increases public investment by more than £100 billion over the next five years to boost growth and help crowd in private investment.

The government is further the crucial role of investment by businesses in driving this growth by: creating the National Wealth Fund, which is expected to catalyse over £70 billion of private investment; setting out plans for a modern Industrial Strategy to support investment in growth-driving sectors and launching a pensions review to unlock greater investment into UK growth assets.

In their engagement to date, businesses and tax experts have been clear that a stable and predictable tax environment provides the confidence needed to support investment. This is why at Autumn Budget the government published its Corporate Tax Roadmap for the Parliament.

The Roadmap includes a commitment to cap the Corporation Tax rate at 25%; maintain the Small Profits Rate and marginal relief at current rates and thresholds; and maintain key features such as Full Expensing, the Annual Investment Allowance, R&D relief rates, and the Patent Box.

The Roadmap also sets out the government’s approach to tax administration: it is committed to creating a business tax environment where taxpayers are confident that they understand the tax rules with which they are required to comply.

Building on strong existing practice (see Box 1.A) the government has further committed to, and is now consulting on, developing a new process giving major investment projects increased tax certainty in advance.

This will further improve the UK as a stable and transparent tax environment, by reducing tax uncertainty for the major projects that are eligible, and in turn support the UK as a hospitable investment destination.

This is in addition to other ongoing work on improving tax certainty by providing clearance on:

-

the treatment of Cost Contribution Arrangements (CCAs) through Advance Pricing Agreements (APAs) (see Chapter 5); and,

-

the availability of R&D tax reliefs, expanding on the current system to reduce error and fraud in, provide certainty to businesses, and improve the customer experience.

Box 1.A Existing routes to certainty on tax administration

Clearances, rulings, and agreements:

HMRC currently provide advance tax rulings through several established processes designed to give businesses and individuals certainty about the tax treatment of specific transactions, reducing the risk of unexpected tax liabilities and ensuring compliance with tax laws.

Advance Pricing Agreements (APAs): Provide assurance on transfer pricing by agreeing on the method for determining the arm’s length price for transactions between related parties.

Statutory Clearances: Provide official confirmation that specific transactions or arrangements will not be subject to certain anti-avoidance rules. Examples include clearances for company reorganisations, share transactions, and Income Tax on share sales.

Non-Statutory Clearances: Provide rulings where there is genuine uncertainty about how tax legislation applies to specific circumstances, where the transaction is not covered by a more appropriate statutory clearance route.

Advance Tariff Rulings: Provide legally binding decisions on the correct commodity code for importing or exporting goods.

Advance Valuation Rulings: Confirm the correct method for valuing goods for import declarations.

R&D clearances: Allow taxpayers to send HMRC details of their company’s R&D work, before claiming R&D tax relief on company tax returns. This is available to first-time claimants with a turnover below £2 million and fewer than 50 employees. In addition to this consultation, the government is also consulting on reforming existing assurances to reduce error and fraud, increase certainty and improve customer experience.

Other support offered by HMRC:

Customer Compliance Managers (CCMs): Are responsible for the relationship between the UK’s largest businesses and HMRC. They engage constructively with customers on their tax affairs in real time.

Temporary CCMs (tCCMs): Provide temporary one-to-one compliance support to mid-sized business customers with greater complexity, those with multiple interactions with HMRC and/or those going through key business life-cycle events.

Inward Investment Support (IIS): Facilitates meetings between investors and the relevant technical specialists within HMRC, and where appropriate, supports a clearance application or appointment of a tCCM. This service is for investments of £30 million and over, or of significant importance to the national or regional economy.

Guidance manuals: Give comprehensive technical guidance on HMRC’s interpretation of tax law, available on GOV.UK.

Guidelines for Compliance (GfC): Help businesses, and their advisers understand HMRC’s perspective on complex, novel, or widely misunderstood areas of tax. GfC assists in managing tax compliance risks by offering insights into the practical application of tax laws and HMRC’s administrative approaches in these challenging areas.

Proposal

Decisions by business on whether and where major investments are made are driven by their fundamental economic viability and projections of their future return on investment. But there are also broader factors, including tax certainty, which materially support business confidence in this decision-making.

Many of these factors firmly align with the UK’s inherent strengths – our established legal system, language, and access to our leading higher education and professional services sectors.

Our tax system is also a key strength. The UK offers a competitive headline rate of Corporation Tax, supported by generous allowances and deductions for capital and R&D expenditure, a competitive regime for intangible assets, and a world-leading tax treaty network.

The UK also strives to provide certainty over how its tax rules are applied, through clear legislation, thorough guidance, and an approach of “co-operative compliance” for the country’s largest businesses to manage any tax risks which remain.

Feedback from businesses and tax experts has been positive on HMRC’s professional, pragmatic, and considered approach to tax administration. It is expected that this will continue to work well for the majority, including many large investment projects where business models are well-established.

However, the government recognises the need to go further for the very largest and most innovative investment projects, given their scale, complexity and range of tax implications. It is therefore consulting on a dedicated service, tailored to these types of projects, which provides statutory certainty over how the tax rules will be applied to a project if it proceeds as planned.

That will not mean exhaustively providing certainty on every tax implication, but rather allowing for a flexible, open discussion with HMRC to agree areas where tax certainty would be of most value and could be suitably provided to the timelines the project is working to.

This should enable the projects involved to more precisely estimate the impact of tax on their rate of return, and so invest more confidently.

This is a significant and innovative proposal, which is more wide-reaching than existing offerings. To ensure this is deliverable, the focus will be on the very largest major investment projects entailing significant expenditure.

The government intends to ensure there are benefits to this approach beyond its immediate beneficiaries where possible, and as such wishes to consult on the advantages and disadvantages of publishing summarised and anonymised clearances.

This proposal takes account of the approaches of other jurisdictions which provide forms of advance tax certainty, including through providing taxpayers with a clearer understanding of their tax obligations and increased assurance.

Many major projects will interact with a range of departments across government, including the Office for Investment and the Department for Business and Trade. Recognising this, the government intends to integrate this new process alongside other relevant services.

Consultation process

This consultation will run for twelve weeks and will close on 17 June 2025.

The government welcomes contributions from stakeholders with an interest in the proposal, including businesses – through industry groups or directly – and tax and investment experts.

The government will be consulting relevant stakeholders and interested parties on the proposals through meetings during the consultation period. If you would like to be included in a consultative meeting, please contact the departments involved via advancetaxcertainty@hmtreasury.gov.uk and advancetaxcertainty@hmrc.gov.uk by 15 April 2025.

Written responses can be sent to the same email addresses during the period the consultation is open. Supporting data is welcome where possible, recognising sensitivities around tax and commercial information.

Once the consultation has closed, the government will then assess the responses and issue a formal response, including next steps. All respondents will be listed by name within that document, with the exception of individuals or where anonymity is expressly requested.

It is the government’s intention to implement the new process in 2026, and it will lay any required legislation ahead of this, including primary legislation via a Finance Bill.

2. Eligibility

Context

This chapter sets out the approach to giving eligibility to taxpayers and investments for the new process, and requests views on this.

Clear parameters will be needed to ensure that HMRC resources are focussed where the greatest impact can be. Focussing on the largest and most complex major projects will facilitate HMRC’s ability to deliver the process and resource it in a way that meets the expectations of applicants. The government remains committed to improving guidance and customer service for all taxpayers, including those that do not benefit from this process.

Entities eligible

The government initially proposes that it should be the corporate entities directly undertaking major investment projects which are eligible for advance tax certainty. At time of application, entities may not have an existing UK presence, but intend to once their investment project formally proceeds. To ensure these are captured, the government proposes the entities eligible to be those that are, or will be, subject to CT.

This approach excludes some structures, and it may be unclear whether others – particularly more complex arrangements – would be eligible under it. The government welcomes examples which would benefit from being in scope which fall into these categories.

It is anticipated that there will be benefits to those investing indirectly through eligible entities from any advance tax certainty obtained at the corporate level.

Question 1: What is the impact of giving eligibility to corporate entities that are or will be subject to CT and are directly undertaking major investment projects? Does this exclude any other structures investing in major projects which would significantly benefit from being in scope?

Question 2: How can advance tax certainty provide material wider benefit beyond the entity receiving the clearance?

Threshold

It is the government’s intention to have a clear quantitative threshold that will identify the largest and most significant projects. This is to ensure applicants have clarity as it would allow projects that exceed this to be clearly in scope.

This threshold would be set in terms of the authorised project spend for major projects investing in fixed and intangible assets. Views are invited on the nature of intangible assets to be included within scope for the threshold.

Views are similarly welcomed on how the threshold could work with phased projects and how best to define project boundaries in an objective way.

There will be a need for safeguards to prevent inappropriate bundling of separate projects for the purposes of meeting the threshold.

In reviewing the level for the threshold, and the period over which it should be calculated, the government will need to also consider HMRC’s capacity to deliver this service: effective delivery of the service will require HMRC to recruit new highly skilled tax professionals, who are limited in number across the UK labour market. The government anticipates initially setting a threshold that would entail dozens, rather than hundreds, of projects being serviced per year, each likely to entail qualifying expenditure in the hundreds of millions. It is proposed this initial threshold be open to review as the process is implemented and develops to ensure it meets both the policy aim and its operational deliverability.

A high financial threshold on its own in isolation may not capture some projects that are of national or strategic importance or are highly impactful on a relative basis within their sector. Respondents are invited to provide examples of such projects, to inform development targeted criteria which would bring these projects within scope, while maintaining the deliverability of the process.

There will be a need for exclusion criteria to prevent abuse of the process, including speculative applications and those where tax avoidance is in point.

Question 3: What is the best way of quantifying the fixed and intangible investment for the purposes of assessing whether a project meets the threshold? Do you agree that authorised project spend is a suitable metric?

Question 4: Is there a set amount of expenditure that would prompt you to seek a clearance or certainty, or would this be more attributable to the amount of tax and uncertainty in treatment?

Question 5: Are there supplementary criteria, which are objective and measurable, which could capture projects below the quantitative threshold which are nevertheless of a national or strategic importance, are highly impactful on a relative basis within their sector, or that have large growth potential despite starting small?

3. Scope

Taxes and issues

Issue scope

The process will be available to give clearances in a way that the current Non-Statutory Clearance service does not: it will not require the demonstration of genuine uncertainty.

The existing Non-Statutory Clearance process will remain in place for those investments that do not qualify for the process.

Any clearance will need to provide the maximum certainty possible without undermining anti-avoidance rules, and this is likely to be reflected in any final scope with regards to main purpose tests.

Interaction with other avenues to certainty

This new process will attempt to avoid duplicating existing processes for clearances, and will allow applicants and HMRC to focus on the most material areas to facilitate quick results.

Where there is an existing, more appropriate advance certainty process, this service will not seek to duplicate it but instead act as a front door. For example, where certainty is sought on the correct transfer pricing method, an introduction would be made to the APA programme.

Tax scope

Corporation Tax will be the core tax on which investors can seek advance certainty, as those entities that make the largest investments in the UK are within the charge to CT.

Feedback from stakeholders to date has been that Corporation Tax would benefit most from advance certainty, but the government is open to exploring the case for expanding the process to other areas such as VAT, Stamps Taxes and Employer Duties with the caveat that this would not seek to duplicate existing forward-looking processes such as Partial Exemption Special Methods (PESM) for VAT and Customs rulings

Question 6: In which areas of UK tax legislation would advance tax certainty have the most impact on investment decisions? Where possible please give examples of where lack of certainty has had a negative effect on an investment decision.

Question 7: Are there areas for which certainty would be of value that are not currently addressed by the non-statutory clearance process? What do you see as potential benefits and barriers to their inclusion?

Form of clearance

The government proposes that tax certainty would be available as to HMRC’s position on specific issues under the clearance process. Clearance applications would therefore set out a specific question regarding taxation of a material aspect of a major project, rather than general tax matters or hypothetical questions.

As stated in the introduction, clearances will not mean exhaustively providing certainty on every tax implication within a project but rather agreeing with HMRC the issues of most value for inclusion in a clearance.

An advance certainty clearance is a binding decision as to HMRC’s application of the law to the facts on a specific tax matter where this is fully disclosed and not misrepresented. This means HMRC would not seek to change its reading of the law as it applies to the issues and fact patterns on which clearance is given where recipients rely upon it, except in specific circumstances.

Circumstances in which HMRC would cease to be bound include where key assumptions are no longer met, or where changes in law render the clearance or part of the clearance obsolete. The process section below details how taxpayers could approach HMRC for clarity in such instances.

Because the clearance given could relate to a transaction which has not yet happened, or is in progress, clearances would be underpinned by a series of key assumptions. A project would be required to remain consistent with these for the clearance to be valid.

Views are sought on whether, and to what extent, the clearance opinion should be mutually binding, recognising that certainty as to HMRC’s position is the main aim of the process, and that there will be instances where HMRC’s technical interpretation does not accord with that of the taxpayer.

Specifically, views are welcomed on the circumstances under which advance tax certainty clearances would or would not bind HMRC or the taxpayer, and how any protections should be given effect. Were clearances not binding on taxpayers, it would also be necessary to consider how taxpayers might notify HMRC where they have chosen not to rely on the clearance.

Clearances will be processed by a central function that understands the needs of those going through the process. That central function will then utilise technical and policy specialists, as well as leveraging existing business and customer relationship knowledge.

This will allow both consistency in policy approaches and transparency and continuity once tax returns covered by the clearance are filed.

Question 8: Who do you consider should be bound by an advance certainty clearance and to what extent. What form should that take?

Question 9: What are the circumstances under which you consider it important to be able to continue to rely on a clearance?

4. Process

Obtaining certainty

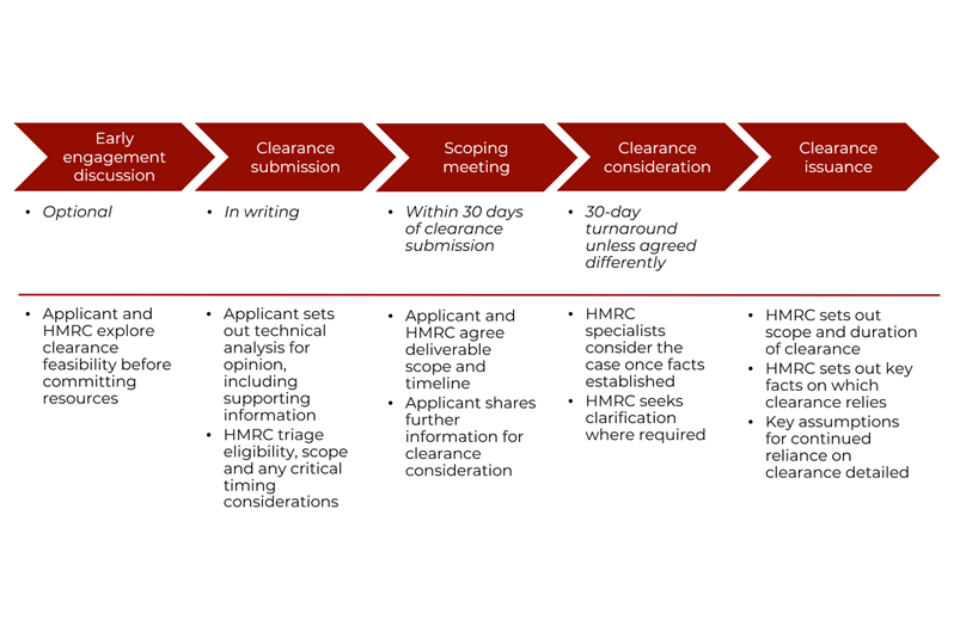

Box 4.A Proposed phases and milestones of the process

Fees

Any new clearance service would be both voluntary and valuable to those who are eligible. The government is therefore considering whether to charge for this service in order to support its timely and resilient delivery. Alternatively, it could operate as an unpaid service, consistent with HMRC’s and other tax authorities’ general approach. Views are invited on whether taxpayers would be willing to pay for access to this process, and whether this would alter their expectations of the steps outlined in this chapter.

Early engagement discussion

For taxpayers seeking comfort on their eligibility, or whether the subject matter of the clearance is within scope or feasible within a particular timeframe, the government is proposing an optional early engagement meeting with HMRC to minimise unnecessary resource commitment for customers.

Early engagement meetings may also be of use where customers are unsure as to whether an advance clearance is the most appropriate route for increased certainty out of those available, or where they are unsure of when to time their formal clearance application to ensure they can provide sufficient facts and analysis for HMRC to give an opinion.

These discussions would be open to those that qualify for the clearance process, or believe that they would, and would not be part of the formal process.

Question 10: Do you consider that an early engagement facility would be helpful and why?

Clearance submission

Advance certainty clearance applications will be required to be made in writing. The government anticipate that applications can be made:

-

In advance of investment of a major project where board approval has been given, or the clearance is the deciding factor in a go/no go investment decision.

-

In advance of finalisation of accounts for a period to support appropriate tax reporting.

-

In advance of submission of the CT return to support correct filing.

Timing is likely to be influenced by the customer having sufficient reliable facts on which to base a technical conclusion.

Applications would confirm their eligibility for the process and set out the technical analysis and conclusions as to the tax treatment of the issue on which clearance is sought. Supporting information to allow HMRC to consider the application would also need to be provided upfront. For valid applications, a designated point of contact is envisaged through the process.

Applications deemed ineligible would be notified in writing together with the basis for this judgement. These would not be appealable through processes such as tribunals, given they are about giving tax certainty to a transaction (or transactions) for which a tax return has yet to be filed. HMRC expects to operate an internal process for reconsideration.

Question 11: How would this process work with typical commercial decision-making timescales?

Question 12: What facility would be helpful for unsuccessful clearance applications? Do you consider for example that the process should include reconsideration by HMRC on request?

Scoping meeting

HMRC propose that a scoping meeting with HMRC for valid applications be held no later than 30 calendar days from receipt of an application, though HMRC may agree to accelerate this in early engagement where the clearance is a deciding factor in go/no go decisions for investment.

Scoping meetings would be used to discuss indicative timelines, further information required, areas of priority focus and any refinements to scope if needed. This would ensure all clearances progressed are both valuable to the applicant and able to be resourced and delivered by HMRC to a mutually acceptable timeframe.

For some, the scoping meeting itself may provide sufficient reassurance to the extent that a full clearance may not ultimately be pursued.

Question 13: Do you consider a scoping meeting to obtain clarity on scope of clearance, timing and inputs to be useful? What would a scoping conversation need to include?

Clearance consideration

Clearances will be considered by a team including deep technical specialists and policy leads where relevant, supported by their process administrator. Where an applicant has an existing working relationship with HMRC, for example through a Customer Compliance Manager, they would be fully involved in the clearance process. The clearance process would allow the clearance team to approach the customer for any final information, discussion or clarification necessary to form a technical view and agree timeframes for delivery of the information and any impact on the clearance timeline.

For clearance applications where the time available to process the clearance prior to filing is limited, the situation may arise where the clearance process is not competed by the filing date.

In such circumstances, responsibility for tax certainty could move from the clearance team to the responsible compliance team via a handover designed to utilise analysis performed to date and allow for continued handling of the issue in evaluation of the filed return.

Question 14: Are there process elements you would consider helpful during the clearance consideration phase?

Clearance issuance

Clearances will be issued in written form and state whether HMRC agree with the technical analysis included in the application, detailing the key facts and assumptions which must continue to be met for the clearance to apply. They will state the duration of the clearance which is unlikely to exceed five years before renewal is required. The clearance issuance process will be subject to an internal governance process to ensure consistency in clearance handling.

Publication

The government intends for the certainty benefit to be available beyond applicants and wishes to consult on the advantages and disadvantages of publishing summarised and anonymised clearances. Publication to a wider taxpayer audience could drive further tax certainty beyond the clearance process and build trust in the tax system.

Although other taxpayers may not rely on the clearance, publication provides potential benefits in helping to clarify HMRC’s position, address legal interpretation uncertainty, and improve policy understanding and consistency.

Many jurisdictions publish advance tax rulings in such an edited form, with delayed publication or redactions to protect sensitive information, including business details and commercially sensitive transactions. In most cases the business will review and agree the summary before publication, with some jurisdictions making publication a prerequisite of clearance consent.

HMRC are conscious of the need to preserve anonymity in considering a clearance publication process and would not wish any such process to act as a deterrent to clearance applications or be unduly administratively burdensome

Question 15: What do you consider the advantages and disadvantages of publishing summarised and anonymised clearances to be? Has publication by other clearance jurisdictions aided tax certainty as a result?

Certainty over time

Factors affecting continued reliance on a clearance

Where only part of the clearance is impacted by a change in law, or where customers are unsure if changes to facts and circumstances or change of ownership would change the clearance opinion given, HMRC will endeavour to work with the customer to confirm any impact on the scope or ability to rely on the clearance going forwards. It is the government’s intention to avoid clearances being fully invalidated by small changes.

HMRC would monitor for changes in facts and circumstances and key assumptions relevant to clearances given. Options may include an annual compliance return or discussion with their compliance contacts within HMRC.

Question 16: What would you wish to see in terms of engagement for clearances where impacted post issuance by legislation, ownership, case law or key facts and assumption changes?

Clearance renewals

For some major projects, the lifespan of the investment may extend beyond the five-year maximum clearance length proposed. The use of a maximum length reflects the high likelihood of change impacting clearance reliability for lengthier periods.

It is proposed that taxpayers with the same projects extending beyond five years may apply for a renewal of the clearance originally given, subject to confirming the facts and key assumptions have not changed to the extent that they impact the clearance conclusions. Safeguards will be built in to prevent renewals expanding the scope beyond the original project.

Question 17: What should a renewals process look like, and is 5 years an acceptable trigger point?

5. Cost Contribution Arrangements

In the Corporate Tax Roadmap, the government committed to reviewing the transfer pricing treatment of Cost Contribution Arrangements (CCAs). CCAs are contractual agreements between group companies to share the costs and benefits of developing assets such as intellectual property.

The government’s review was motivated by this being a complex area of transfer pricing where different interpretations of the international guidelines exist. This increases the risk of disputes and double taxation.

The government held discussions with members of the key advisory firms acting in this area to inform its review. Following those discussions, the government intends to offer clearance on the treatment of CCAs through Advance Pricing Agreements (APAs) using existing legislation. Unilateral APAs would provide certainty that CCAs will be respected as the framework for pricing CCA transactions.

The government intends to publish an updated Statement of Practice which will detail the necessary conditions for granting such a clearance. The commerciality of the CCA and the expected profitability of the UK participant over its term will likely be factors in determining whether HMRC enters into an APA.

In addition to providing advance certainty on tax treatment in future periods, APAs can apply to periods where returns have already been filed. The government understands that it is important to provide taxpayers with certainty on the treatment of CCAs where there may currently be ambiguity.

This approach aims to protect inward investment, provide increased tax certainty, and address an area of technical difficulty that can lead to unresolved double taxation.

Annex A List of consultation questions

Chapter 2: Eligibility

1) What is the impact of giving eligibility to corporate entities that are or will be subject to CT and are directly undertaking major investment projects? Does this exclude any other structures investing in major projects which would significantly benefit from being in scope?

2) How can advance tax certainty provide material wider benefit beyond the entity receiving the clearance?

3) What is the best way of quantifying the fixed and intangible investment for the purposes of assessing whether a project meets the threshold? Do you agree that authorised project spend is a suitable metric?

4) Is there a set amount of expenditure that would prompt you to seek a clearance or certainty, or would this be more attributable to the amount of tax and uncertainty in treatment?

5) Are there supplementary criteria, which are objective and measurable, which could capture projects below the quantitative threshold which are nevertheless of a national or strategic importance, are highly impactful on a relative basis within their sector, or that have large growth potential despite starting small?

Chapter 3: Scope

6) In which areas of UK tax legislation would advance tax certainty have the most impact on investment decisions? Where possible please give examples of where lack of certainty has had a negative effect on an investment decision.

7) Are there areas for which certainty would be of value that are not currently addressed by the non-statutory clearance process? What do you see as potential benefits and barriers to their inclusion?

8) Who do you consider should be bound by an advance certainty clearance and to what extent. What form should that take?

9) What are the circumstances under which you consider it important to be able to continue to rely on a clearance?

Chapter 4: Process

10) Do you consider that an early engagement facility would be helpful and why?

11) How would this process work with typical commercial decision-making timescales?

12) What facility would be helpful for unsuccessful clearance applications? Do you consider for example that the process should include reconsideration by HMRC on request?

13) Do you consider a scoping meeting to obtain clarity on scope of clearance, timing and inputs to be useful? What would a scoping conversation need to include?

14) Are there process elements you would consider helpful during the clearance consideration phase?

15) What do you consider the advantages and disadvantages of publishing summarised and anonymised clearances to be? Has publication by other clearance jurisdictions aided tax certainty as a result?

16) What would you wish to see in terms of engagement for clearances where impacted post issuance by legislation, ownership, case law or key facts and assumption changes?

17) What should a renewals process look like, and is 5 years an acceptable trigger point?

Annex B Privacy notice

Processing of personal data

This section sets out how we will use your personal data and explains your relevant rights under the UK General Data Protection Regulation (UK GDPR). Both HM Treasury and HM Revenue and Customs (HMRC) will be data controllers for any personal data you provide in response to this consultation.

Data subjects

The personal data we will collect relates to individuals responding to this consultation. These responses will come from a wide group of stakeholders with knowledge of a particular issue.

The personal data we collect

The personal data will be collected directly from data subjects through voluntary email submissions in response to this consultation and are likely to include respondents’ names, email addresses, their job titles and opinions.

How we will use the personal data

This personal data will be processed for the purpose of obtaining opinions about government policies, proposals, or an issue of public interest to inform the further development or implementation of the consultation subject.

Contact details you provide during this consultation will, in some circumstances, be used to contact you to discuss your response further.

Processing of this personal data is necessary to help us understand who has responded to this consultation.

HM Treasury will not include any personal data when publishing its response to this consultation.

Lawful basis for processing the personal data

Article 6(1)(e) of the UK GDPR; the processing is necessary for the performance of a task we are carrying out in the public interest. This task is consulting on the development of departmental policies or proposals to help us to develop effective government policies.

Who will have access to the personal data

The personal data will only be made available to those with a legitimate business need to see it as part of consultation process.

This consultation is being issued by HMT in partnership with HM Revenue and Customs (HMRC), so any personal data received in responses will be shared between HMT and HMRC As the personal data is stored on our IT infrastructure, it will be accessible to our IT service providers. They will only process this personal data for our purposes and in fulfilment with the contractual obligations they have with us.

How long we hold the personal data for

We will retain the personal data until work on the consultation is complete and no longer needed. Your data protection rights

Relevant rights, in relation to this activity are to:

- request information about how we process your personal data and request a copy of it

- object to the processing of your personal data

- request that any inaccuracies in your personal data are rectified without delay

- request that your personal data are erased if there is no longer a justification for them to be processed

- complain to the Information Commissioner’s Office if you are unhappy with the way in which we have processed your personal data

How to submit a data subject access request (DSAR)

To request access to your personal data that HM Treasury holds, please email: dsar@hmtreasury.gov.uk

Complaints

If you have concerns about Treasury’s use of your personal data, please contact our Data Protection Officer (DPO) in the first instance at: privacy@hmtreasury.gov.uk

If we are unable to address your concerns to your satisfaction, you can make a complaint to the Information Commissioner at casework@ico.org.uk or via this website: https://ico.org.uk/make-a-complaint.