Governance and reporting of climate change risk: guidance for trustees of occupational schemes

Updated 21 July 2021

© Crown copyright 2021

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/consultations/taking-action-on-climate-risk-improving-governance-and-reporting-by-occupational-pension-schemes-response-and-consultation-on-regulations/governance-and-reporting-of-climate-change-risk-guidance-for-trustees-of-occupational-schemes

This is draft statutory guidance. Read the final guidance at Governance and reporting of climate change risk: guidance for trustees of occupational schemes.

Draft statutory guidance proposed to be issued pursuant to section 41(A) and 41(B) of the Pensions Act 1995.

This draft Guidance is produced for the purposes of consultation.

It does not have any effect unless the Pension Schemes Bill receives Royal Assent and the Occupational Pension Schemes (Climate Change Governance and Reporting) Regulations 2021 and the Occupational Pension Schemes (Climate Change Governance and Reporting) (Miscellaneous Provisions and Amendments) Regulations 2021, which are each currently the subject of consultation, come into force.

Part 1: Background

About this Guidance

1. From 1 October 2021 the Occupational Pension Schemes (Climate Change Governance and Reporting) Regulations 2021 [footnote 1] (“the Climate Change Governance and Reporting Regulations”) introduce new requirements relating to reporting in line with the Task Force on Climate-related Financial Disclosures (TCFD) recommendations, to improve both the quality of governance and the level of action by trustees in identifying, assessing and managing climate risk.

2. The Occupational Pension Schemes (Climate Change Governance and Reporting) (Miscellaneous Provisions and Amendments) Regulations 2021 [footnote 2] (“the Miscellaneous Provisions Regulations”) amend the Occupational and Personal Pension Schemes (Disclosure of Information) Regulations 2013 [footnote 3] (“the Disclosure Regulations”) to introduce disclosure requirements relating to the reports required by the Climate Change Governance and Reporting Regulations .

3. In complying with the requirements in Part 2 of and the Schedule to the Climate Change Governance and Reporting Regulations trustees are required to have regard to guidance issued from time to time by the Secretary of State. [footnote 4]

Legal status of this Guidance

4. This Guidance is statutory guidance produced under sections 41A(7) and 41B(3) of the Pensions Act 1995 (“the 1995 Act”) and section 113(2A) of the Pension Schemes Act 1993 (“the 1993 Act”), unless otherwise stated.

5. The guidance on trustee knowledge and understanding included at Part 2 paragraphs 28-34 is not statutory guidance. Trustees are not required to have regard to it, but may find it helpful.

Expiry or review date

6. This Guidance will be reviewed as a minimum every 3 years, from the date of first publication, and updated when necessary.

7. When we review the Guidance we will consider, for possible inclusion, lessons from established and emerging best practice of the way in which TCFD reports are produced, and improvements in data quality and completeness.

Audience

8. This Guidance is for trustees who are subject to the requirements in Part 2 of and the Schedule to the Climate Change Governance and Reporting Regulations, as described below. Once the requirements are fully phased in, this will include trustees of both money purchase and non-money purchase schemes with £1bn or more in “relevant assets”. It will also include, trustees of all authorised master trusts and authorised schemes (once established) providing collective money purchase benefits, in both the accumulation and decumulation phases.

9. Trustees of schemes whose relevant assets are £5bn or more at the end of their first scheme year to end on or after 1 March 2020 will be subject to the climate change governance requirements from 1 October 2021, or, if later, the date they obtain audited accounts in relation to that scheme year.

10. Trustees of authorised master trusts and authorised schemes (once established) providing collective money purchase benefits will be subject to the governance requirements from 1 October 2021, or, if later, the date the scheme becomes authorised.

11. Trustees of schemes whose relevant assets are £1bn or more at the end of their first scheme year to end on or after 1 March 2021 will be subject to the governance requirements from 1 October 2022, or, if later, the date they obtain audited accounts in relation to that scheme year.

12. Trustees of schemes whose relevant assets are £1bn or more at the end of a scheme year which falls on or after 1 March 2022, will be subject to the governance requirements from the beginning of the scheme year which is one scheme year and one day after the scheme year end date when the relevant assets were £1bn or more.

13. Trustees must produce and publish a report (“TCFD report”), containing the information required by Part 2 of the Schedule to the Climate Change Governance and Reporting Regulations, within 7 months of the end of any scheme year in which they were subject to the climate change governance requirements. Regulation 3(2) provides for limited exceptions to this requirement.

14. Where a scheme’s relevant assets fall below £500m on any subsequent scheme year end date, the trustees will cease to be subject to the climate change governance requirements with immediate effect (unless the scheme is an authorised scheme). The trustees must still publish their TCFD report for the scheme year which has just ended within 7 months of the scheme year end date, unless one of the exceptions in regulation 3(2) applies.

15. The circumstances in and timing by which trustees fall in and out of scope of the requirements is further detailed in the Climate Change Governance and Reporting Regulations. The purpose of this Guidance is not to restate those legal requirements, but instead to help trustees understand how to meet them when they apply.

16. Trustees of other schemes may also find this Guidance helpful when carrying out climate change risk governance and reporting on a voluntary basis.

PCRIG guidance on TCFD Recommendations

17. The Pensions Climate Risk Industry Group (PCRIG) has produced non-statutory guidance [footnote 5] for trustees on ways to approach improving their scheme’s climate governance and TCFD disclosures. Whilst it is not mandatory for trustees to consider or follow the PCRIG’s guidance, trustees may find its practical nature very helpful. For example, it sets out the types of action trustees may wish to consider following an assessment of climate risks and opportunities (which is beyond the scope of this Guidance) and it suggests wider resources that trustees may find helpful for scenario analysis amongst other topics. Trustees may therefore find it helpful to consider the PCRIG’s guidance in addition to this statutory Guidance.

When this Guidance should be followed

18. The Climate Change Governance and Reporting Regulations require the trustees of schemes in scope to:

- implement climate change governance measures and produce a TCFD report containing associated disclosures; and

- publish their TCFD report on a publicly available website, accessible free of charge

19. The amendments made to the Occupational and Personal Pension Schemes (Disclosure of Information) Regulations 2013 by the Miscellaneous Provisions Regulations require trustees who must produce a TCFD report to, among other things:

- include a link to the TCFD report in the Annual Report

- tell members that the TCFD report has been published and where they can locate it, by including this information in the Annual Benefit Statement and, for defined benefit (DB) schemes, the Annual Funding Statement

20. Trustees of occupational pension schemes must have regard to this Guidance when meeting requirements under the Regulations.

‘Must’ vs ‘Should’ vs ‘May’

In this Guidance, activities will be described as things trustees either ‘should’ do, ‘may’ choose to do or ‘must’ do. What this means for the purposes of the Guidance is set out below:

Should – It is expected that trustees will follow the approach set out in the Guidance and if they choose to deviate from that approach they should describe concisely the reasons for doing so in the relevant section of their TCFD Report.

May – Trustees can choose to follow the approach set out in the Guidance, and are encouraged to do so where possible, but if they choose not to they are not expected to explain their reasons in their TCFD Report.

Must - This is a requirement imposed by legislation. Failure to meet the requirement may lead to enforcement action by The Pensions Regulator.

Compliance with this Guidance

21. For occupational pension schemes, The Pensions Regulator (TPR) monitors compliance with legislation and provides guidance about what trustees need to do. The Department for Work and Pensions (DWP) is responsible for answering questions about the policy intentions behind the legislation. Neither DWP nor TPR can provide a definitive interpretation of the legislation, which is a matter for the courts.

22. Trustees and service providers should consider the Climate Change Governance and Reporting Regulations to determine whether the new requirements apply to them, taking further advice where necessary.

23. Where the trustees do not comply with a requirement under the Climate Change Governance and Reporting Regulations – including where this is as the result of a failure to have regard, or to have proper regard, to this Guidance – TPR may take enforcement action which includes the possibility of a financial penalty.

24. Enforcement of requirements under the Climate Change Governance and Reporting Regulations is provided for in Part 3 of those Regulations. Regulation 5 of the Disclosure Regulations [footnote 6] sets out the penalties for failure to comply with the disclosure requirements referred to in this Guidance.

Part 2: Climate change governance requirements – overview

“As far as they are able”

1. Trustees are required to carry out the following activities “as far as they are able”: [footnote 7]

- undertake scenario analysis [footnote 8]

- obtain the scope 1, 2 and 3 greenhouse gas emissions and other data relevant to their chosen metrics [footnote 10]

- use the data obtained to calculate their selected metrics [footnote 10]

- use the metrics they have calculated to identify and assess the climate-related risks and opportunities which are relevant to the scheme [footnote 11]

- measure, on an annual basis, the performance of the scheme against any target they have set [footnote 12]

2. Requirements to undertake the relevant activities “as far as they are able” recognises that there may be gaps in the data trustees are able to obtain about their scheme assets for the purposes of carrying out scenario analysis or calculating metrics. Additionally, in the case of DB schemes, there may be limitations in the scenario analysis they can carry out in relation to their liabilities or funding strategy, for example the sponsoring employer’s covenant.

3. Certain data may be expensive to collect or accompanying analysis complex to carry out. Trustees or those acting on their behalf are not expected to spend disproportionate amounts of time attempting to fill data gaps in relation to firms which are unlikely – due to their business activities or size – to contribute to climate-related risks posed to the scheme.

4. If trustees are able to obtain data or analysis in a format which is usable but only at a cost – whether directly or indirectly via liaison with advisers – which they believe to be disproportionate, they may make the decision to treat this data as unobtainable. A robust justification for doing so should be set out in their TCFD report.

5. Trustees should be prioritising engagement on persistent data gaps which are likely to make the most material difference to accurately assessing the level of climate-related risk (or opportunity), to ensure that data quality continues to improve. Additional information requests to fill data gaps should be made with due regard to the size of the investee company in question and the likely materiality of their contribution to climate-related risks faced by the scheme.

6. The requirement to undertake scenario analysis “as far as they are able” may require trustees, or those acting on their behalf, to seek comprehensive data across their portfolio. For trustees of DB schemes, considering the resilience of the funding strategy as part of their scenario analysis would include considering the sponsoring employer’s covenant “as far as they are able”. However, if they cannot obtain a complete picture, they should still undertake scenario analysis. In cases of incomplete data, they may need to:

- where they have a majority of data for particular asset classes – use modelling or estimation to fill the missing data gaps

- where there are certain asset classes or aspects of liability for which impacts, data or modelling tools are very limited or uncertain - take a qualitative instead of quantitative approach (see Part 3, paragraphs 58 to 60) for certain aspects of their analysis, or proceed with scenario analysis for part of their portfolio or for certain liabilities only

7. Trustees should explain concisely in their TCFD report the extent to which they were able to obtain the data and other information needed to carry out the scenario analysis and explain any gaps.

8. For metrics, trustees must obtain data required to calculate their chosen metrics “as far as they are able”. They must then use this obtained data to calculate their chosen metrics. Similarly, trustees must measure, as far as they are able, performance against any targets they have set in relation to those metrics. Limitations in data should not deter trustees from taking steps towards quantifying and assessing their scheme’s exposure to climate-related risks and opportunities more effectively through the use of metrics, and managing that exposure through the use of targets. Even estimated or proxy data can help identify carbon-intensive hotspots in portfolios, which can help to inform their investment and funding strategies. Trustees can also request that service providers apply sectoral averages based on companies that do publish data to fill in gaps in relation to companies who do not, or use other assumption-based modelling.

9. For metrics and targets, the Scope 3 emissions [footnote 13] of a scheme’s investments are likely to be challenging. Trustees should seek to ensure the emissions of scheme assets, especially Scope 3 emissions, are calculated in line with the GHG Protocol Methodology, [footnote 14] and apportioned using a consistent approach, [footnote 15] to allow, so far as possible, for aggregation and comparability across asset classes and funds and between schemes.

10. For metrics trustees must explain in their TCFD report why, if relevant, the data does not fully cover the portfolio or extend to all scopes of emissions.

11. This explanation should be concise but it should set out clearly what data is missing and the impact this has in terms of the scope of the analysis or calculations the trustees have been able to do. It should also make clear where estimations or models have been used to fill gaps, whether these follow recognised standards or models, whether any data gaps still remain and what steps the trustees are taking to address these gaps. If trustees are using third party providers for scenario analysis, calculation of metrics, or measuring the scheme’s performance against targets, they should make sure that they are provided with sufficient information to be able to report on this.

Ongoing and Discrete Requirements

12. Some of the requirements imposed on trustees under the Climate Change Governance and Reporting Regulations are ongoing. This means that the activities trustees undertake to meet them should be maintained and where necessary updated throughout the scheme year. This applies to the activities associated with governance, strategy (excluding scenario analysis) and risk management.

13. Some of the requirements are discrete. This means that the duty is to do something at a particular frequency. This applies to the activities associated with scenario analysis, metrics and targets.

Frequency of discrete activities

14. Scenario analysis must be carried out in the first scheme year during which the Regulations apply – even if the first year of application is a part year – and then at least every three years thereafter. In the intervening years when trustees are not required to carry out scenario analysis, they must still consider whether it is nevertheless appropriate to do so. Further information is set out in the section on scenario analysis below.

15. The data for metrics (Greenhouse Gas-emissions based and non-Greenhouse Gas emissions based) [footnote 16] should be obtained, and the metrics calculated, at least annually. Performance against targets should be measured and the targets reviewed at least annually. Further information is set out in the section on metrics and targets below.

Level of the assessment

16. Governance and Risk Management activities should be carried out for the whole scheme.

17. Trustees should undertake the Strategy activities, including scenario analysis, at the following levels – and report accordingly:

- for a single section DB scheme, or for a DC scheme with no member choices [just 1 default, and no self-select funds]: at the level of the whole scheme

- for a scheme with more than 1 DB “section”: at the level of each section. However, sections with similar characteristics in relation to assets, liabilities and funding may be grouped

- for DC schemes: for each popular default arrangement offered by the scheme. A popular default arrangement is considered to be one meeting the definition of default arrangement in regulation 1 of the Occupational Pension Schemes (Investment) Regulations 2005 [footnote 17] in which 250 or more members are directly invested, irrespective of whether they are actively contributing

18. For schemes providing both DB and DC benefits, the two benefits should be considered separately for the purposes of the above – so for a scheme with two DB sections with dissimilar characteristics and 1 popular DC default, the activities under Strategy should be carried out three times. However, DC assets which are solely attributable to Additional Voluntary Contributions may be disregarded for the purposes of the above.

19. Where default arrangements use life-styling or a number of target date funds for different age profiles, trustees may carry out the assessment in the round, but should identify risks and opportunities which affect particular cohorts more strongly.

20. Where appropriate, the approach set out above for Strategy activities should also be followed by trustees for calculating and reporting Metrics. However, if, in calculating absolute emissions metrics and emissions intensity metrics, trustees believe it is not meaningful to aggregate data across certain asset classes within a given section or arrangement of the scheme, they may choose not to do so.

21. Trustees are free to measure performance against Targets and report on this in whatever way they see fit.

22. For self-select funds and default arrangements with fewer than 250 members in DC schemes, trustees may also undertake and report on the Strategy activities, including scenario analysis, calculate and report on Metrics, and set, measure performance against and report on Targets.

Risks and opportunities

23. To meet the requirements imposed by the Climate Change Governance and Reporting Regulations 2021, trustees should have a good understanding of the climate-related risks and opportunities that are relevant to their scheme.

24. They may find it helpful to split their analysis of risks into ‘physical risks’ and ‘transition risks’ as a way to understand the potential impact on the scheme’s investments:

- physical risks are those that pertain to the physical impacts that occur as the global average temperature rises. For example, the rise in sea levels could have impacts such as flooding and mass migration. Extreme weather events, such as flooding and fires, could become more frequent and severe, and these incidents could threaten physical assets and disrupt supply chains

- transition risks arise as we seek to realign our economic system towards low-carbon, climate-resilient solutions. Changes in industry regulation, consumer preferences and technology will take place and impact on current and future investments

- litigation risks may also result where businesses and investors fail to account for the physical or transition risks of climate change

25. The financial risks resulting from the effects of climate change have a number of distinctive elements:

- far-reaching in breadth and magnitude: The financial risks from physical and transition risk factors are relevant to multiple lines of business, sectors and geographies. Their full impact may therefore be larger than for other types of risks, and the risks are potentially non-linear, correlated and irreversible

- the time horizons over which financial risks may be realised are uncertain. Past data is unlikely to be a good predictor of future risks

- there is a high degree of certainty that financial risks from some combination of physical and transition risk factors will occur

- the magnitude of future impact will, at least in part, be determined by the actions taken today. This includes actions by governments, firms, pension schemes and a range of other actors

26. Trustees have a legal duty to consider matters which are financially material to their investment decision-making. Trustees must not only consider the kinds of financial risks which might affect investments (and in the case of DB schemes, their liabilities and sponsoring employers’ covenant), they should consider where climate change, and action to address climate change, might contribute positively to anticipated returns or reduce risk.

27. Climate change related opportunities may include access to new markets and new technologies related to the transition to a low-carbon economy. Examples of climate-related risks and opportunities and their potential financial impacts are comprehensively set out in the TCFD’s Final Recommendations. [footnote 18]

Trustee knowledge and understanding of climate-related risks and opportunities

Trustee knowledge and understanding

This section is non-statutory guidance, intended as best practice.

Trustees are not required to have regard to this section of the guidance but are encouraged to do so. Trustees are not expected to provide an explanation in their TCFD Report if they choose not to follow this guidance.

28. Beyond existing duties to have knowledge and understanding of pensions law and the principles relating to investments, [footnote 19] new requirements for knowledge and understanding in relation to climate change apply to individual and corporate trustees who are subject to requirements in the Climate Change Governance and Reporting Regulations. The new requirements are prescribed by regulation 2 of the Miscellaneous Provisions Regulations 2021.

29. Individual trustees must have knowledge and understanding of the principles relating to the identification, assessment and management of risks arising to occupational pension schemes from the effects of climate change. They must also have knowledge and understanding of the principles relating to the identification, assessment and management of opportunities relating to climate change for occupational pension schemes.

30. Individual trustees must have the appropriate degree of knowledge and understanding of these matters to enable them to properly exercise their functions. In the case of corporate trustees, the company is required to secure that any person exercising its functions as trustee has the appropriate degree of knowledge and understanding of these matters.

31. This means, for example, understanding how scenario analysis works, why climate change poses a material financial risk and its relevance to overall risk management.

32. This understanding need not require a mastery of technical detail, however. It is anticipated that in most cases, trustees –or those exercising trustee functions in the case of corporate trustees - will not be carrying out the underlying activities to identify or assess climate-related risks and opportunities themselves, or implementing investment strategies which take account of climate change in a hands-on way. Rather, they will identify experts to do this. Yet as trustees are ultimately responsible for identifying, assessing and managing climate-related risks the scheme is exposed to, they should have sufficient knowledge and understanding to interpret the results of any analysis and the know how to take action in light of these results, or indeed to challenge assumptions, external advice and information. In the case of corporate trustees, they should ensure that those exercising their functions have this knowledge and understanding.

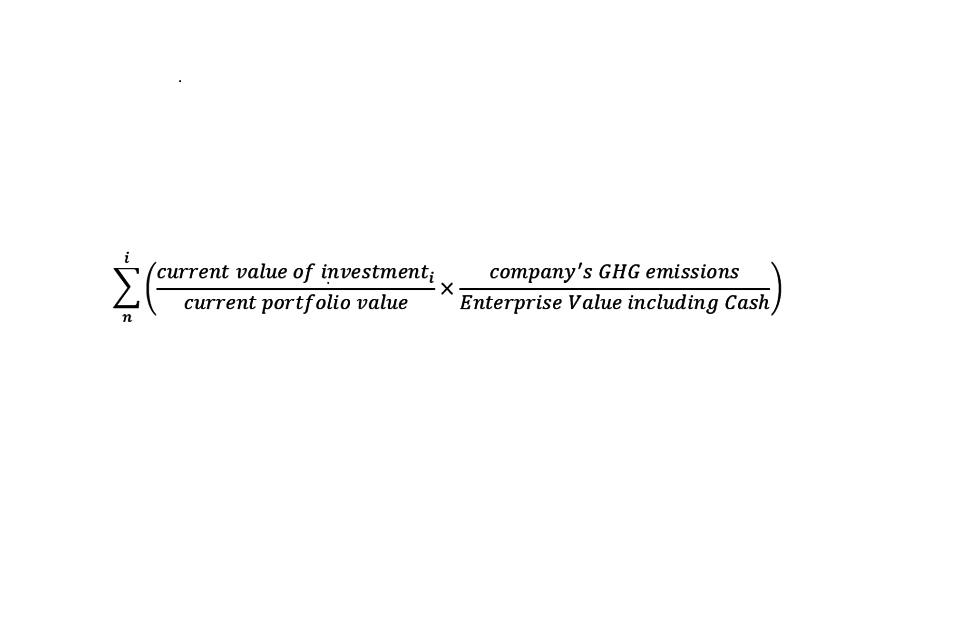

33. Trustees are encouraged to ensure that they – or those exercising their functions, in the case of corporate trustees – are keeping their knowledge and understanding of climate-related risks and opportunities up-to-date, so that they can meet the knowledge and understanding requirements.

34. Stewardship, including engagement and voting activities, can promote the long term success of pension schemes. Through engagement with intermediaries including consultants and asset managers, as well as investee companies, trustees are in a good position to keep their knowledge of climate change risk and opportunities up-to-date and learn about governance approaches, strategies, risk management tools and metrics and targets.

Part 3: Climate change governance and production of a TCFD Report

1. This section of the Guidance sets out the matters to which trustees of the schemes in scope must have regard when producing a TCFD report in accordance with the Climate Change Governance and Reporting Regulations.

2. To do this effectively, trustees need to meet the requirements specified in the Regulations in relation to Governance, Strategy and Risk Management, carry out scenario analysis, select and calculate appropriate Metrics and set Targets and measure the scheme’s performance against them.

Purpose of disclosures

3. The Climate Change Governance and Reporting Regulations require trustees to disclose a range of information about their scheme. The specifics of these disclosures are set out in Part 2 of the Schedule to the Regulations, with more information in this guidance.

4. In general, trustees should regard disclosure as the output of the processes they have put in place and actions they have taken to understand and address the risks and opportunities that climate change poses to the scheme.

5. Disclosing the information is an important way to help achieve transparency toward members, TPR and the pension sector generally. This should improve accountability, regulation and best practice. However, the principal purpose of disclosure is to ensure that trustees are thorough and rigorous in taking the actions required by the Climate Change Governance and Reporting Regulations. This is aligned with the Government’s intention to make TCFD-aligned disclosures mandatory across the economy by 2025. [footnote 20]

Content of a TCFD Report

6. A significant benefit of making TCFD reports publicly available is that it will provide members with the opportunity to engage with their scheme’s climate-related risks and opportunities, and its potential impact on their pension savings.

7. Whilst we acknowledge the challenges of producing a TCFD report which is digestible by all beneficiaries, trustees should present their TCFD reports in a way that would allow a reasonably engaged and informed member to be able to interpret and understand trustees’ disclosures, and raise concerns or queries where appropriate.

8. As a minimum, the TCFD report should include a plain English summary which is for members to read and allows them to become easily acquainted with the key findings from the report. This will allow trustees to retain the necessary more in-depth analysis in the larger report, which more engaged members may still wish to read in full.

9. Trustees should also consider the TCFD’s own Principles of Effective Disclosure, as set out in the Annex, when producing their TCFD Reports.

10. In summary, the core elements that should be included in the TCFD report are:

Governance

The organisation’s governance around climate-related risks and opportunities.

Strategy

The actual and potential impacts of climate-related risks and opportunities on the organisation’s businesses, strategy and financial planning.

Risk Management

The processes used by the organisation to identify, assess and manage climate-related risks.

Metrics and Targets

The metrics and targets used to assess and manage relevant climate-related risks and opportunities.

Governance

11. ‘Governance’ refers to the way a scheme operates and the internal processes and controls in place to ensure appropriate oversight of the scheme. Those undertaking governance activities are responsible for managing climate-related risks and opportunities. This includes trustees and others making scheme-wide decisions. This includes – but is not limited to – decisions relating to investment strategy, funding (including the sponsoring employer’s covenant) or liabilities.

12. Under the Climate Change Governance and Reporting Regulations trustees must establish processes to satisfy themselves that any person undertaking governance activities takes adequate steps to identify, assess and manage climate-related risks and opportunities relevant to the scheme. Asset managers and administrators are not considered to be in scope of those undertaking “governance activities”. Trustees must also establish processes to satisfy themselves that those advising or assisting the trustees with respect to governance activities, take adequate steps to identify and assess relevant climate-related risks and opportunities. Legal advisers are excluded for the purposes of this requirement.

Trustees’ and others’ oversight of climate-related risk

13. Trustees have ultimate responsibility for ensuring effective governance of climate-related risks and opportunities. The roles and responsibilities of the trustees and others making scheme-wide decisions pertaining to climate-related risk, should be addressed at board, sub-committee and individual trustee levels. The Climate Change Governance and Reporting Regulations require trustees to put in place and report on the governance processes that ensure they have oversight of the climate-related risks and opportunities relevant to the scheme. These governance processes should enable trustees to be confident that their statutory obligations and fiduciary duties are being met.

14. Trustees should decide the appropriate governance structure and processes for their scheme. Trustees may choose to take an approach to the oversight and management of climate change risks that replicates the process for how they consider other risks and opportunities. Alternatively, trustees may decide that the governance process around climate-related risk and opportunities should be separate, reflecting the unique challenge these risks pose and the severity of the impact they could have on their portfolio. Either approach is acceptable – trustees may base the decision on their assessment of the magnitude, nature, unpredictability and duration of climate-related risks to the scheme, and may take account of cost and complexity.

15. Trustees should allocate time and resources for meeting their obligations on climate change governance and reporting. It is expected that for most schemes, trustees will require regular discussion of climate-related risk and opportunities at board level, as a substantive agenda item.

16. All schemes are exposed to some degree of climate-related risks and opportunities. The appropriate amount of time and resource the trustee allocates to governing these risks, will depend on factors such as the size, type and maturity of the scheme, and to what degree the scheme is exposed to climate-related risk. Trustees should use outputs from other TCFD-related activities, including Risk Management, Strategy (including scenario analysis) and Metrics and Targets to help determine how much time and resource is allocated to overseeing climate-related risk.

17. Trustees may need to revise their governance structure and processes in light of these outputs. For example, if trustees discover, through scenario analysis, that some of the scheme’s assets are particularly vulnerable to a type of climate-related risk, they should reconsider whether they are dedicating sufficient resource to processes for assessing and mitigating risk.

Oversight of climate-related risk by those who undertake governance activities and advise or assist with those activities

18. Most occupational pension schemes operate a governance structure that is at least partly reliant on persons other than the trustees or trustee board. The Climate Change Governance and Reporting Regulations apply in respect of those undertaking governance activities in relation to the scheme and those who advise or assist the trustees with respect to governance activities. By undertaking governance activities, we mean making scheme-wide decisions. By advising or assisting with respect to governance activities, we mean advising or assisting the trustee with scheme-wide decisions. Those undertaking governance activities or advising or assisting with respect to these activities include:

- employees of the scheme

- employees of the principal or controlling employer [footnote 21]

- employees of the scheme funder or strategist [footnote 22] (in the case of a master trust)

- external advisers who provide services to the trustee

19. External advisers include those who influence significant climate-related decisions, including investment consultants, scheme actuaries, voting advisers, covenant advisers and fiduciary managers. The common characteristic of these persons is that they are engaged by the trustees or the sponsoring employer, to advise or assist the trustee with scheme-wide decisions or occasionally make scheme-wide decisions.

20. Trustees should clearly define the roles and responsibilities, in relation to climate-related risk, of the groups of people they consider to be involved in governing the scheme. This should not extend beyond the role these persons hold in relation to the specific scheme.

21. Trustees should satisfy themselves that those governing the scheme have adequate climate-related risk expertise and resources. The governance processes put in place should enable trustees to engage with those governing the scheme and check that those individuals / groups have adequately prioritised climate-related risk.

22. When using external advisers to identify and/or assess climate-related risks and opportunities, trustees should consider and document the extent to which these responsibilities are included in any agreements, such as investment consultants’ strategic objectives and service agreements.

23. Trustees must ensure that the scheme’s governance process and structure provides them with adequate oversight of how those governing the scheme are managing the scheme and adequately assessing and managing climate-related risks and opportunities on their behalf. Trustees should provide opportunities for existing employees to undertake climate risk training and – where skills gaps are identified by the trustees – encourage external advisers to do the same.

24. Trustees may find it helpful to do a skills audit in relation to:

- the trustees expertise on climate change

- the expertise of others undertaking governance activities

- the expertise of those advising or assisting in respect of governance activities

25. Having a clearer picture of the skills and gaps that exist across these three groups, will help the trustees develop processes to keep their knowledge and understanding, in relation to Governance, Strategy, Risk Management and Metrics and Targets, up-to-date. Trustees should also ensure that persons to whom they have assigned climate-related responsibilities have clear directions in terms of how and how frequently they inform trustees of their work. It is expected that trustees would need regular updates, the frequency of which will depend on the particular risks the scheme is exposed to and the results of other TCFD-related outputs, like scenario analysis. It is important that trustees understand the information provided to them and can critically challenge this information, where appropriate.

26. Trustees cannot delegate responsibility for their obligations under the Climate Change Governance and Reporting Regulations 2021. Trustees have ultimate responsibility for how the scheme manages climate-related risks and opportunities. The Regulations do not impose new legal duties on persons other than trustees.

27. Trustees should ensure that information about the scheme that is relevant to the identification, assessment and management of risks and opportunities relating to climate change is shared between persons tasked with these responsibilities. There should be clear lines of communication between those working on climate-related risk and others within the scheme.

Disclosure of governance information

28. In relation to the governance disclosure requirements, trustees should describe in their TCFD report:

- the approach they have taken to overseeing climate-related risks and opportunities which are relevant to the scheme

- the roles and responsibilities of those undertaking governance activities in relation to the scheme, in identifying, assessing and managing climate-related risks and opportunities relevant to the scheme

- the processes the trustees have taken to ensure those undertaking governance activities are adequately identifying, assessing and managing those risks and opportunities

- the role of those advising or assisting the trustees with governance activities

- the processes the trustees have taken to ensure the person advising or assisting has taken adequate steps to identify and assess climate-related risks and opportunities which are relevant to the scheme

29. To help contextualise these disclosures, trustees should concisely describe:

- how the board and any relevant sub-committees are informed about, assess and manage climate-related risks and opportunities and the frequency at which these discussions take place

- whether they questioned and, where appropriate, challenged the information provided to them by others undertaking governance activities – or advising and assisting with governance

- the rationale for the time and resources they spent on governance of climate- related risks and opportunities

30. Trustees should also describe, in relation to those who undertake governance activities, or advise or assist with governance of the scheme:

- the kind of information provided to them by those persons about their consideration of climate-related risks and opportunities faced by the scheme

- the frequency with which this information is provided

31. Trustees should describe the training opportunities they provided for existing employees. Where trustees identified skills gaps, they should also describe whether they encouraged external advisers to undertake training opportunities.

32. Trustees may wish to provide an organogram or structural diagram in their TCFD report, showing which groups / individual roles have responsibilities for governance of climate-related risks and opportunities. This may include executive officers, in-house teams and / or third parties engaged by the trustees. For the avoidance of doubt, there is no expectation that this would involve disclosing personal data of individuals.

Strategy

33. Trustees should think strategically about the climate-related risks and opportunities that will have an effect on the scheme. In doing so they must consider climate-related risks and opportunities in relation to their investment strategy and their funding strategy, where they have one. Part of this assessment will include scenario analysis. More detail about this is set out in paragraphs 58 to 60 below.

Investment strategy and funding strategy

34. ‘Investment strategy’ refers to factors such as the scheme’s strategic asset allocation, the selection of investment mandates and portfolio construction. It includes whether the scheme’s investments and mandates are active or passive, pooled or segregated, growth or matching, or have long or short time horizons.

35. ‘Funding strategy’ refers to the strategy by which the trustees expect to have sufficient assets to meet the expected future payments due from the scheme. It includes consideration of:

- the scheme’s assets and how the value(s) of the asset held are expected to develop in the future

- the contributions that will be paid by the sponsoring employer to clear any technical provisions deficit (and the likelihood of those contributions being paid)

- the ability of the sponsoring employer to continue to be able to make those deficit repair contributions in the future

- the strength of the covenant offered by the sponsoring employer and how the strength of the covenant is expected to develop over the expected lifetime of the scheme

36. Consideration of the resilience of the funding strategy includes consideration of the sponsoring employer’s covenant. This includes undertaking scenario analysis.

Scope of assessment

37. All asset types are within scope for the assessment of a scheme’s investment strategy, funding strategy (where it has one) and for scenario analysis. Trustees should not start from the assumption that climate change is irrelevant for some assets or sectors. For example, climate-related risks could affect the value of assets such as corporate and sovereign debt. Climate change may also affect the strength of the sponsoring employer’s covenant. The scenario analysis requirement is subject to the provision that trustees are expected to do this “as far as they are able”. This may mean that initially, for some schemes, not all asset classes can be included in the scenario analysis or that some assets will be assessed by a broader qualitative approach.

Time horizons

38. Trustees must decide the short, medium and long term time horizons that are relevant to their scheme. Trustees must state in their TCFD report the time horizons they have chosen, for example “the medium-term time horizon is 5 years”.

39. It is up to trustees how they determine their time horizons. However, in deciding what the relevant time horizons are, trustees must take into account the scheme’s liabilities and its obligations to pay benefits. Trustees should also take account of the following:

- in a DB scheme: the likely time horizon over which current members’ benefits will be paid. This may be the longest time horizon they will need to consider

- in a DC scheme: the likely time horizon over which current members’ monies will be invested to and through retirement. This may be the longest time horizon they will need to consider

40. Trustees may also consider other factors such as the scheme’s cash flow, investment strategy and, where they have one, funding strategy.

41. Trustees are not required to disclose in their TCFD report why they have chosen certain time horizons. However, they may decide to do so.

Types of risks and opportunities

42. Trustees should identify, and assess the impact of, what they consider to be the relevant climate-related risks and opportunities for each time horizon (short, medium and long term). See Part 2, paragraphs 23 to 27 above for guidance on types of climate-related risks and opportunities that may be relevant to the scheme. Examples of climate-related risks and opportunities and their potential financial impacts are also comprehensively set out in the TCFD’s Final Recommendations. [footnote 23]

Considerations relating to the funding strategy

43. The covenant is a significant source of support for most DB schemes. Sponsoring employers’ businesses may be affected by climate change including (but not limited to) physical risks (e.g. to their supply chains) and/or transition risks, which may be particularly impactful for sponsoring employers in, or dependent upon, high carbon sectors.

44. As part of their assessment of the resilience of the funding strategy, trustees of DB schemes must consider the impact of climate related risks and opportunities on the sponsoring employer’s covenant over the relevant short, medium and long-term time horizons. Trustees’ scenario analysis must also, as far as they are able, consider the resilience of the covenant in the relevant chosen scenarios.

45. Trustees seeking information about the impact of climate change on their sponsoring employer may wish to consider:

- dialogue with the sponsoring employer to discuss its assessment of the risks, and opportunities, to which it is exposed. The information above on “Risks and Opportunities” (see Part 2, paragraphs 23 to 27) may help frame this discussion

- any climate-related disclosures, such as TCFD reports, made by the sponsoring employer

46. Where trustees of a DB scheme identify climate-related concerns with the sponsoring employer and the potential strength of the covenant, they may want to take action such as:

- considering whether their investment strategy and funding strategy are sufficiently prudent, in light of non-mitigated climate risks

- considering whether their long-term funding objective is appropriate or needs to change

- incorporating climate-related triggers into the scheme’s contingency planning framework

47. However, trustees are not compelled to take action. Where they cannot form a robust assessment of the impact of climate change on the covenant, for example because of lack of information or uncertainty about the impact of climate change on the sponsoring employer’s business model, they should keep the assessment under review and consider elevating covenant risks within their risk management priorities.

48. Discussions about the impact of climate change on the covenant will often involve confidential information about the sponsoring employer. This is equally true for other information shared as part of the covenant review process and wider discussions. Its confidential nature should not therefore prevent it from being shared with trustees and their advisers.

49. When making their own TCFD disclosures, trustees should take account of the confidential nature of information shared about the covenant. However, trustees and sponsoring employers should not assume that this information is always confidential business information that would harm the sponsoring employer if disclosed. For example, trustees may be able to disclose higher level information and/or information about the process they have followed. Trustees may wish to take legal advice regarding confidentiality.

Assessing the impact on the investment strategy and funding strategy

50. Trustees must, on an ongoing basis, assess the impact of the climate-related risks and opportunities they have identified on the scheme’s investment strategy, and the funding strategy, where the scheme has one.

51. Climate change may affect a scheme’s assets, including potential earnings impairment or enhancement in relation to companies in which they invest. DB schemes’ liabilities may also be affected by impacts on inflation, interest rates and demographic factors, particularly longevity, as well as climate change impacting on the sponsoring employer’s covenant.

52. Trustees should consider climate-related risks and opportunities in the context of their strategic asset allocation, and how climate change may affect the different asset classes the pension scheme is invested in over time.

53. Trustees should consider the asset manager mandates they intend to set for each asset class. Trustees may wish to align their mandates with the climate-related risks and opportunities they have identified as relevant to their scheme.

54. Trustees investing in pooled funds should consider how the managers take climate change into account in those funds, including in relation to stewardship and engagement.

55. It is up to trustees how they undertake the assessment. However, trustees may find it helpful to “grade” or organise the identified risks and opportunities across the time horizons. Factors that could be considered include likelihood, timeline, severity of impact etc.

56. In line with the TCFD’s Supplemental Guidance for Asset Owners, trustees may wish to undertake, either directly or through their agents, engagement activity with investee companies to encourage better disclosure and practices related to climate-related risks. This may help improve data availability and trustees’ ability assess such risks. [footnote 24]

Scenario Analysis

- Scenario analysis requirements must be met by trustees “as far as they are able”. More information about this is set out at Part 2, paragraphs 1 to 11.

Considerations for approaching scenario analysis

Quantitative or qualitative scenario analysis

58. Scenario analysis may be qualitative and/or quantitative. Trustees with no or limited experience of scenario analysis may find it easiest to start with qualitative analysis. Qualitative scenario analysis uses narratives to explore the implication of different possible climate impacts. At its most basic, trustees could start from the question “what if…?” and introduce potential climate-related risks, for example “what if policymakers introduced a high carbon price?”

59. Quantitative scenario analysis can produce more developed and rigorous outputs. Trustees of all schemes in scope should progress towards developing the sophistication of their scenario analysis and to using quantitative analysis, especially where they believe that climate change could pose significant risks to their scheme.

60. Trustees may want to overlay their quantitative analysis with a qualitative narrative, for example by providing some wider context and explaining the impact of their findings. In line with the TCFD’s Supplemental Guidance for Asset Owners, trustees may wish to provide a discussion of how climate-related scenarios are used, such as to inform investments in specific assets. [footnote 25] This can help with their own, and others’, understanding.

Using third-party providers

61. Trustees may want to use the services of a third-party provider to do scenario analysis. A third-party provider may be able to help trustees apply an “off the shelf” scenario or to develop a bespoke one.

62. However, whether or not they use a third-party provider, trustees should ensure that they have an understanding of the scenarios that are used. This includes the underlying assumptions which make up the scenarios (for example, scenarios will be based on assumptions about variables such as the use of carbon capture and storage technologies, the timing of emissions reduction and the scope of policy interventions). If trustees do not understand these, it will be difficult for them to interpret and act on the outputs of the scenario appropriately.

63. The TCFD Technical Supplement on the use of Scenario Analysis in disclosure of climate-related risks and opportunities [footnote 26] sets out more details on common assumptions in scenario analysis.

64. Trustees should also consider whether they could gain more insight from undertaking a simpler form of scenario analysis in-house than out-sourcing it to a third-party. Trustees should keep in mind that the purpose of scenario analysis is to better understand the risks and opportunities posed by climate change to the scheme and to inform their strategy and investment decisions accordingly. Trustees should not assume that this will be best achieved by using the most complex, sophisticated and/or expensive tools available.

Information from asset managers

65. Trustees may find it easiest to do a “top-down” analysis of the scheme-level risks to their scheme’s aggregated portfolio. This may be easier than starting from information from asset managers about individual asset classes. It is also likely to be difficult for trustees to aggregate scenario analysis that has been done on different asset classes or by different managers for reasons such as different underlying assumptions.

Chosen scenarios

66. Trustees must conduct scenario analysis in at least two scenarios where there is an increase in the global average temperature and in one of those scenarios the global average temperature increase selected by the trustees must be within the range of 1.5oC above pre-industrial levels, to and including 2oC above pre-industrial levels. The temperature used in the scenario should be the “eventual” temperature increase within the chosen timeframe, on the assumption that the temperature would stabilise at this level and not continue increasing.

67. In selecting the scenario’s they will use, trustees should consider not only the projected potential global average temperature rise but also the nature of the transition to that temperature rise. For example, it is possible to have many different scenarios representing an eventual global average temperature rise of 2°C above pre-industrial levels because of differences in the assumptions made about the type of transition. Trustees may therefore want to consider a range of scenarios like the following:

- a measured, orderly transition takes place with climate policies being introduced early and becoming gradually more stringent. Ambitions under the Paris Agreement and commitments such as the UK’s commitment to achieve net zero by 2050 are met in an orderly manner. This is likely to mean lower transition risks and less severe physical risks. (Such a scenario could be used for the required scenario of a temperature increase within the range of 1.5oC above pre-industrial levels, to and including 2oC above pre-industrial levels)

- a sudden, disorderly transition takes place with climate policies and wider action on climate change not happening until late (e.g. introduced around 2030). Although climate goals are met, transition risks are also more likely to materialise, given the need for sharper emissions reductions, alongside increased physical risks. (Such a scenario could be used for the required scenario of a temperature increase within the range of 1.5oC above pre-industrial levels, to and including 2oC above pre-industrial levels)

- a “hot house world” which assumes only currently implemented policies are preserved, current commitments are not met and emissions continue to rise. This would mean climate goals are missed and physical risks are high with accompanying severe social and economic disruption.

68. The Network for Greening the Financial System sets out representative scenarios in the above ranges which trustees may want to reflect in their own scenario analysis. [footnote 27]

69. A list of reference scenarios can also be found at Annex 2 of the Climate Financial Risk Forum Guide to Scenario Analysis. [footnote 28]

70. Trustees should choose scenarios that reflect their reasoned assessment of plausible pathways and should not focus on scenarios that rely on progress, or otherwise, that they consider unlikely to happen.

71. Physical risks are relevant in all scenarios that assume any global temperature increase. Trustees should therefore test the resilience of their investment strategy and, if they have one, their funding strategy against both transition and physical risks.

72. When selecting scenarios, trustees should seek to avoid selecting scenarios which, although related to different eventual temperature increases, present similar trajectories over the time horizons that are relevant to the scheme. For example, trustees of a scheme with a time horizon of 10 years should avoid using two scenarios that both assume ‘business as usual’ for the next decade before diverging.

Scenario analysis and the funding strategy

73. Assessing the resilience of the funding strategy includes consideration of the sponsoring employer’s covenant. The covenant is an important source of support for many DB schemes. Trustees should use scenario analysis to better understand the potential impact on the covenant of the effects of climate change. Trustees may initially find it easiest to start with qualitative scenario analysis for the covenant. Trustees may want to address questions such as:

- what are the greatest risks posed to the sponsoring employer in our chosen scenarios / if X happens?

- what could the sponsoring employer do to address such a risk? Is the sponsoring employer taking action to avoid and/or address such a risk?

Liabilities

74. Trustees must, as far as they are able, assess the potential impact on the liabilities of the scheme of the effects of the global average increase in temperature, and of any steps which might be taken because of the temperature increase – by governments or otherwise – in their chosen scenarios. This may include considering the impact on:

- financial assumptions based on market yields / assumed market values that may be mis-priced if they do not take account of climate change

- investment return assumptions based on models that extrapolate past trends and so implicitly ignore the possible future impact of climate change

- mortality rates, which may be impacted by environmental factors such as air pollution, changes in temperatures and extreme weather events and economic factors such as financial well-being and access to healthcare

75. This is a developing area of work and trustees and their advisers may not always be able to reach robust conclusions on which they are able to act. However, trustees should still seek to understand the potential impact of the effects of climate change on their liabilities.

Annual review

76. Scenario analysis must be undertaken in the first scheme year during which trustees are subject to the requirements in the Regulations– even if the first year of application is a part year – and every three years thereafter.

77. However, in the scheme years where trustees are not required to undertake scenario analysis, they must review their most recent scenario analysis and determine whether they should nevertheless undertake new scenario analysis in order to have an up-to-date understanding of the matters they are required by the Regulations to consider.

78. Circumstances which are likely to lead trustees to decide that new scenario analysis should be undertaken in a year where it is not mandatory include, but are not limited to:

- a material increase in the availability of data. This is likely to happen as TCFD reporting increases across the investment chain, bringing with it more data for different asset classes and for sponsoring employers’ businesses. This is likely to happen rapidly in the first few years after the Climate Change Governance and Reporting Regulations are in force

- a significant/material change to the investment and/or funding strategy

- the availability of new or improved scenarios (for example 1.5 oC scenarios) or events that might reasonably be thought to impact key assumptions underlying scenarios (for example, more countries making net zero commitments)

- a change in industry practice/trends on scenario analysis. This may include increased popularity of particular types of scenarios or widespread use of particular temperature outcomes to use for a “business as usual” scenario

- some other material change in the scheme’s position

79. If trustees decide not to undertake new scenario analysis, they must explain in their TCFD report the reasons for their decision. If they do not carry out new scenario analysis, they must also include the results of the most recent scenario analysis in their latest TCFD report, as set out below

Disclosure of strategy and scenario analysis information

80. Trustees must describe in their TCFD report:

- the time periods which the trustees have determined should comprise the short term, medium term and long term

- the climate-related risks and opportunities relevant to the scheme over those time periods that the trustees have identified and the impact of these on the scheme’s investment strategy and, where the scheme has a funding strategy, the funding strategy

- the most recent scenarios the trustees have used in their scenario analysis

- the potential impacts on the scheme’s assets and liabilities which the trustees have identified and the resilience of the scheme’s investment strategy and, where the scheme has a funding strategy, the funding strategy, in the most recent scenarios the trustees have analysed

- where trustees have concluded that it is not necessary to undertake new scenario analysis outside the mandatory cycle, the reasons for this determination

81. Trustees should also describe in their TCFD report:

- their reasons for choosing the scenarios they have used

- the critical assumptions for the scenarios used and the key limitations of the modelling (for example, material simplifications or known under/over estimations)

- any information relating to gaps in data which have limited their ability to undertake their assessment (see section on “as far as they are able” at Part 2, paragraphs 1 to 11 above)

82. Trustees may include information in their TCFD report on any other aspects of the assessment of their investment strategy and, if they have one, funding strategy and scenario analysis that they consider would be helpful to disclose.

Risk Management

83. Climate-related risk present unique challenges and requires a strategic approach to risk management. Trustees must adopt and maintain processes for the purpose of enabling them to identify, assess and manage climate-related risks which are relevant to the scheme, and must ensure that their overall risk management integrates management of climate-related risks which are relevant to the scheme.

84. This means having adequate processes for the management of all risks to which the scheme is exposed, including climate-related risks. Trustees must identify, assess and manage the transitional risks to their investments that the pursuit of a lower carbon economy will bring, as well as the physical risks to their assets brought about by the changes in our climate which are already taking place. Risks to liabilities and employer covenants are further risks trustees should be mindful of.

85. Good risk management is a key characteristic of a well-run scheme and an important part of the trustee’s role in protecting members’ benefits. An adequate risk management system will allow trustees to keep scheme assets safe and protect the scheme from adverse risks. Trustees are best placed to decide what risk management process to use, they should be asking:

- which climate change risks are most material to the scheme?

- how do we take account of transition and physical risk in our wider risk management?

- how does climate change affect our risk appetite?

Processes for identifying and assessing climate-related risk

-

Trustees must adopt and maintain processes for the purpose of enabling them to identify and assess climate-related risks which are relevant to the scheme. A scheme’s existing processes may warrant adjustment to ensure they sufficiently address the unique characteristics of climate-related risks.

-

Transitioning to a lower-carbon economy may entail extensive policy, legal, technology, and market changes to address mitigation and adaptation requirements related to climate change. Depending on the nature, speed, and focus of these changes, transition risks may pose varying levels of financial and reputational risk to schemes.

Climate-related risk types

The TCFD recommendations divide climate-related risks into two major categories:

1) Transition Risks: This category includes policy, legal, technology, market and reputation risk factors. Descriptions of these transition risks can be found in the TCFD’s guidance on Risk Management, alongside approaches for managing those risks and possible metrics for measuring risk.

2) Physical Risks: Physical risks from climate change can be event driven (acute) or longer-term shifts (chronic) in climate patterns, and include risks such as a rise in sea levels, with impacts including flooding.

These physical risks may have financial implications for schemes, such as direct damage to assets and indirect impacts from supply chain disruption. Other potential impacts of physical changes in the climate are wider social disruption, including mass displacement, environmental-driven migration and social strife.

88. Trustees may rely on other persons, including advisers and asset managers, to help them identify and assess climate-related risks. However, trustees have overall responsibility for the management of these risks and also the opportunities arising from climate change. Possible approaches to identifying and assessing transition risks and physical risks involve the trustee:

- identifying regulatory developments that are relevant to the scheme to help assess impact of risks

- assessing and forecasting both new and legacy technologies to manage technology risks

- engaging with service providers to compare the scheme’s position to peers or competitors

- identifying relationships between events and news, and business and financial impacts to manage reputational risks

- identifying and assessing physical risks will generally require the trustee to extend their consideration to long-term horizons

- considering the impact of physical risk factors such as physical damage - and disruption to outsourcing arrangements and supply chains – for key parts of the scheme’s portfolio

89. The trustees’ assessment of climate-related risks is fundamental to their prioritisation of those risks, and management of those which pose the most significant potential loss and are most likely to occur.

90. Trustees may use a traditional “likelihood and impact” approach to gauge the severity or materiality of their risks. Given some of the unique characteristics of climate-related risks, trustees may expand their prioritisation criteria to include “vulnerability” and “speed of onset”:

- vulnerability refers to the susceptibility of a scheme to a risk event, in terms of its preparedness, agility, and adaptability

- speed of onset is the time that elapses between the occurrence of an event and the point at which the scheme feels its effect. Knowing the speed of onset can help trustees develop risk response plans

91. The processes for assessing risks should be applied at the asset-class or key sector level as a minimum. Trustees may consider undertaking more granular risk appraisal to identify trends in risk.

92. As discussed in TPR’s Integrated Risk Management (IRM) [footnote 30] guidance, risk identification should not be a one-off exercise. Further, TPR recommends that, as a minimum, trustees should consider conducting high level risk monitoring at least once a year. Trustees should increase the frequency of monitoring if risk levels approach pre-determined risk appetites.

Processes for managing climate-related risk

93. Trustees must ensure they have processes in place for the purpose of enabling them to manage effectively climate-related risks which are relevant to the scheme. Trustees should consider whether new risk management tools are needed to support management of climate-related risks or whether existing tools can be adjusted to reflect the unique characteristics of these risks.

94. Trustees should consider the time horizon over which risks are traditionally identified and assessed and whether that time horizon is sufficiently long-term to take account of the timescale over which climate-related risks need to be considered (see paragraphs 38-41), or whether it should be extended.

Integration of climate-related risk

95. Whatever climate-related risks are financially material to the pension scheme, trustees must embed management of these into the scheme’s wider risk-monitoring and management processes. There are four key principles trustees should consider:

- interconnections: integrating climate-related risks into the scheme’s existing risk management framework requires analysis and collaboration across the scheme and, if relevant, with asset managers, investment consultants and DB funding and covenant advisers

- temporal orientation: climate-related physical and transition risks should be analysed across short, medium, and long-term time frames for operational and strategic planning. Analysis of physical risks, in particular, may require extension beyond traditional planning horizons

- proportionality: the integration of climate-related risks into existing risk management processes should be proportionate to the scheme’s other risks, the materiality of its exposure to climate-related risks, and the implications for the scheme’s investment and funding strategies

- consistency: the methodology used to integrate climate-related risks should be used consistently within a scheme’s risk management process to support clarity on analysis of developments and drivers of change over time

96. Trustees should ensure that they, and those they engage, have a general understanding of climate change concepts and the potential impacts of climate change.

97. The trustees should understand how risk management and strategic planning tie together and it may be helpful for trustees to review key governance, strategy setting, and risk management processes.

98. The trustees should incorporate climate-related risks into the existing risk management framework and risk inventory used by the scheme. This includes mapping climate-related risks into existing risk categories and types. This involves determining whether such risks will be treated as stand-alone risks, cross-cutting drivers of existing risks, or a combination of both – and then appropriately incorporating risks into the scheme’s risk management framework. The risk categories should include financial, operational and strategic risks – however, most schemes have additional risk categories as well.

Disclosure of risk management processes

99. The primary purpose of requiring disclosure of risk management processes is to provide context for how the trustees think about and address the most significant risks to their efforts to achieve appropriate outcomes for members.

100. Trustees should describe in their TCFD report the processes they have established for identifying, assessing and managing climate-related risks in relation to the scheme, and how the processes are integrated within the trustees’ overall risk management of the scheme.

101. The report should also include concise information on the following:

- the risk tools the trustees used and the outputs / outcomes of using those particular tools

- how the trustees have identified, assessed and managed both transitional risks to the scheme’s investments and the physical risks to its assets

- how the trustees’ assessment of climate-related risks has impacted the scheme’s prioritisation and management of risks which pose the most significant potential loss and are most likely to occur

102. Disclosing information about how climate-related opportunities are identified, assessed and managed is encouraged as this will add further insights for members and others into the scheme’s overall approach to climate-related risk. Trustees may also include information on how their stewardship approach helped them manage climate-related risks and opportunities. The TCFD provides supplemental guidance on engagement activity and risk. [footnote 31]

Metrics

103. For trustees, metrics can help to inform their understanding and monitoring of the scheme’s climate-related risks and opportunities. Quantitative measures of the scheme’s climate-related risks and opportunities, in the form of both emissions and non-emissions-based metrics, should help trustees to identify, manage and track their scheme’s exposure to the risks and opportunities climate change will bring.

104. Trustees must select and report on a minimum of one absolute emissions metric, one emissions intensity metric and one additional climate change metric, and must review their metric selections from time to time as appropriate to the scheme. The requirements imposed on trustees with regard to metrics are at paragraphs 14 to 16 and paragraph 21(n) of the Schedule to the Climate Change Governance and Reporting Regulations.

Emissions metrics

Which emissions

105. Trustees must obtain, as far as they are able, the Scope 1, 2 and 3 GHG emissions for the scheme’s assets [footnote 32] – that is, the pension scheme’s financed emissions. These are the emissions referred to as category 15 (investment emissions) in the GHG Protocol Technical guidance for calculating scope 3 emissions. [footnote 33]

106. The emissions measured are the seven gases mandated under the Kyoto Protocol, converted to and expressed as carbon dioxide equivalents (CO2e).

107. Trustees are not required to obtain or disclose the Scope 1 and 2 emissions of the scheme’s operations – for example, the emissions caused by heating or lighting in offices. They are also not required to obtain or disclose Scope 3 emissions of the scheme other than category 15 “investment emissions” – for example, they do not need to obtain or disclose emissions data relating to business travel or employee commuting by the trustees or others undertaking governance activities on their behalf, or assisting with or advising on governance activities.

Calculation and attribution of the emissions

108. An internally consistent methodology should be used wherever possible when trustees undertake steps to calculate metrics - for example, when they aggregate fund level emissions data provided by their asset managers or third party data providers.

109. Trustees should seek to ensure the emissions of the scheme’s assets are calculated and attributed in line with the GHG Protocol methodology [footnote 34] – to allow for aggregation and comparability across asset classes and funds and between schemes.

110. In measuring the pension scheme’s’ “share” of the emissions of a given asset, trustees should, wherever it is meaningful to do so, attribute those emissions according to the trustees’ investment (their equity, or the outstanding value of their loan) divided by a measure of the total equity and debt. For listed and unlisted equities and for corporate bonds, the Enterprise Value Including Cash (EVIC) [footnote 35] may be used as a measure of the total equity and debt.

111. For real estate or infrastructure, the value of the asset or the value at origination may be used as the denominator.

112. For sovereign bonds, trustees may choose to attribute a production- or consumption-based measure of total national emissions according to trustees’ share of total Government debt. Trustees are free to use other methodologies and do not need to provide justification for their choice, but they should explain in their TCFD report the approach they have taken in using their chosen methodology.

113. Trustees may use the Global GHG Accounting and Reporting Standard developed by the Partnership for Carbon Accounting Financials (PCAF) [footnote 36] for the attribution of emissions for asset classes for which a methodology is available.

114. There is no expectation that trustees should calculate emissions removed or avoided. Nor are trustees expected to calculate projected lifetime emissions of projects for which they are an initial sponsor or lender, in the year that they were financed. If these emissions are included in the TCFD report they should be set out separately.

Timing of the emissions

115. Trustees should seek to obtain the most recent available greenhouse gas emissions for the holdings which made up their portfolio on a given date.

116. Recognising there is often a lag between financial reporting and the required data becoming available, trustees should use the most recent data available even if the data used relates to different years. For example, trustees reporting on emissions in the 2022 financial year might still need to rely on some 2021 disclosures.

Recommended absolute emissions metric: Total GHG emissions

117. Trustees should use total greenhouse gas emissions as their absolute emissions metric.

118. Trustees should seek to calculate the Total GHG Emissions for each DB section and each popular DC default arrangement in the scheme as set out in part 2, paragraphs 17-20.

Recommended emissions intensity metric: Carbon footprint

119. Whilst total GHG emissions are more effective in communicating contribution to climate change, they are difficult to translate into exposure to risk. A larger scheme may have higher total emissions but be less exposed to climate change risk than a smaller scheme.