Anti-money laundering and counter-terrorist financing: Supervision Report: 2023-24 (Accessible)

Published 13 March 2025

© Crown copyright 2025

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/anti-money-laundering-and-countering-the-financing-of-terrorism-supervision-report-2023-24/anti-money-laundering-and-counter-terrorist-financing-supervision-report-2023-24-accessible

Foreword

A strong, transparent, and well-regulated financial system is fundamental to the UK’s economic growth and global competitiveness. By maintaining robust defences against illicit finance, we not only safeguard our national security but also create an environment that attracts investment and supports growth. The government’s commitment to tackling the threat of money laundering, terrorist financing, and corruption is an important part of this mission.

A growing threat requires an ambitious response. That is why this Government has committed not only to continue to deliver the Economic Crime Plan 2023-26, but also to develop an ambitious government-wide anti-corruption strategy.

Against this backdrop, HM Treasury’s annual supervision report for the financial year 2023-24 provides an important insight into the activities of the UK’s 25 anti-money laundering/counter terrorist financing (AML/CTF) supervisors. Supervision plays a crucial role in the UK AML/CTF regime, ensuring that over 90,000 businesses maintain strong and proportionate controls, and supporting them to remain responsive to the latest risks in their sector.

This year the Treasury has significantly expanded the information which this report provides. It includes new metrics on the guidance and training supervisors provide for firms and data on how supervisors are targeting activity according to risk. This reflects our commitment to strengthening oversight, supporting businesses in their compliance efforts, and recognising the value of effective supervision.

The information in this report will be important in helping to inform long-term decisions on structural reform to the UK supervisory system, as well as improvements to the Money Laundering Regulations. By prioritising the effectiveness of our AML/CTF regime, we are not just tackling economic crime; we are building a stronger, more prosperous UK.

Emma Reynolds MP, Economic Secretary to the Treasury

1. Introduction

The UK has a comprehensive anti-money laundering and counter-terrorist financing (AML/CTF) supervision regime, responsible for ensuring that a range of firms engaging in high-risk activities take effective action to identify and prevent money laundering and terrorist financing.

AML/CTF supervisors play a critical role in protecting the UK against the threat of economic crime. This includes important actions such as registering regulated firms, updating them on the latest risks in their sector, overseeing firms’ application of the Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017 (‘the MLRs’), supporting and monitoring firms’ compliance and effectiveness, and taking enforcement action where necessary.

HM Treasury works closely with the supervisors - the Financial Conduct Authority (FCA), His Majesty’s Revenue and Customs (HMRC), the Gambling Commission (GC) and the 22 legal and accountancy Professional Body Supervisors (PBSs) - as well as with the Office for Professional Body Anti-Money Laundering Supervision (OPBAS).

This is HM Treasury’s 12th report on AML/CTF supervision. This report provides information on the activities of AML/CTF supervisors in the 2023-24 financial year and fulfils HM Treasury’s obligation, under Section 51 of the Money Laundering Regulations (MLRs), to publish an annual report on supervision activity using information requested from supervisors.

Each chapter of the report considers a different area of supervisory activity:

-

Chapter 2 covers the responsibility of supervisors to register businesses for supervision under the MLRs, and to assess money laundering and terrorist financing risks within their populations.

-

Chapter 3 details each supervisor’s risk-based approach to monitoring compliance with the MLRs by their population using various methods such as desk-based reviews, onsite visits, and other supervisory interventions.

-

Chapter 4 outlines supervisors’ use of enforcement action to promote compliance with the AML/CTF standards among their supervised population.

-

Chapter 5 explores supervisors’ educational role in supporting firms to take a risk-based approach by sharing relevant guidance and risk assessments, and covers collaboration with other supervisors, law enforcement, and the private sector.

Economic Crime Plan 2023-26 and the UK’s AML/CTF regulatory and supervisory regime

The government takes a robust and holistic approach to tackling all forms of economic crime, with sustained action to improve the response spanning law enforcement, industry and a range of key public bodies such as HMRC, the FCA and Companies House. An effective AML/CTF regulatory and supervisory regime is a critical component of this whole-system approach.

The government has committed to continued delivery of the Economic Crime Plan 2023-26 (ECP2), a strategy agreed between the public and private sectors which sets out a programme of specific actions and milestones that span the whole of the UK’s economic crime landscape.

ECP2 set out a range of specific actions to improve the effectiveness of the AML/CTF regulatory and supervisory regime, building on commitments from the 2022 review of the MLRs These include:

-

AML/CTF supervisors taking action to make further improvements to their effectiveness.

-

HM Treasury and OPBAS strengthening their existing oversight of the AML/CTF supervisors.

-

HM Treasury consulting on a potential package of changes to improve the effectiveness of the MLRs and reform the UK’s AML/CTF supervisory regime.

Reforming the UK’s future supervision regime

HM Treasury committed in ECP2 to continue strengthening the UK’s AML/CTF supervision regime, and in 2023 consulted on four potential options for reform. This government remains committed to reforming the UK’s AML/CTF supervision regime and will announce a plan for reform as a priority. While reform is implemented, however, the quality and consistency of the current supervision system remains immensely important. It is also vital that the UK can measure and assess the effectiveness of the supervision regime, both before and after any reform.

Improving the effectiveness of the Money Laundering Regulations

AML/CTF supervision can only be effective if it is underpinned by clear and robust regulations which are targeted at high-risk activity. HM Treasury is committed to working with supervisors, regulated firms and law enforcement to continue improving and updating the MLRs as needed, including to reflect changes in threats to the UK.

In 2024 HM Treasury ran a public consultation on potential changes to improve the effectiveness of the MLRs. The consultation covered a range of issues identified in the 2022 Review of the MLRs and other priority issues raised by stakeholders. HM Treasury is considering the consultation feedback carefully and developing detailed proposals on each issue.

Preparing for the Financial Action Task Force’s next assessment of the UK

The Financial Action Task Force (FATF), an intergovernmental organisation which sets global standards for AML/CTF, has now begun its fifth round of assessments of global efforts to tackle money laundering, and terrorist and proliferation financing. As part of this, the UK will undergo an in-depth evaluation by its peers, resulting in a new Mutual Evaluation Review. The assessment, which will be published in 2028, but for which data is already being gathered and preparation has begun, will consider the effectiveness of the UK’s AML/CTF/CPF (Counter Proliferation Financing) regime and the UK’s technical compliance with the FATF’s 40 Recommendations.

This round of FATF assessments will be based on a new methodology, which has been revised to place a greater emphasis on effectiveness, risk and context. Mutual evaluations in this round will assess the effectiveness of the supervision of financial institutions and virtual asset service providers, and supervision of non-financial businesses and professions, separately. This will provide a clearer overview of the level of effectiveness of supervision in these distinct areas, and stronger and more targeted recommendations for improvement.

As a leading member of FATF, the government welcomes a renewed international focus on the effectiveness of supervision and expects supervisors to demonstrate effective implementation of the required standards. Indeed, many of the supervisors demonstrate this implementation in their own publications and reports of supervisory activity and enforcement, such as those which the government requires the PBSs to publish under Regulation 46A of the MLRs (see Annex C), which provide more context and explanation to many of the statistics in this report.

OPBAS also continues to drive improvements in supervisory effectiveness through its updated Sourcebook for Professional Body Anti-Money Laundering Supervisors, which was published in January 2023 and aims to deliver a stronger and more consistent standard of supervision of the accountancy and legal sectors.

Updating the UK’s National Risk Assessments

Understanding the nature and extent of money laundering, terrorist financing and proliferation financing (PF) risk is crucial to inform effective and appropriately risk-based supervision. HM Treasury and the Home Office are jointly responsible for publishing periodic assessments of money laundering and terrorist financing risk, and the Treasury is responsible for publishing equivalent assessments of proliferation financing risk.

The government is aware that these assessments provide important insight to all actors who help tackle economic crime. The MLRs require supervisors to refer to the National Risk Assessments of Money Laundering and Terrorist Financing when they carry out their own AML/CTF risk assessments. Regulated persons under the MLRs must also undertake their own risk assessments of PF, and manage and mitigate PF risks. The third ML/TF National Risk Assessment (NRA) was jointly published by HM Treasury and the Home Office in December 2020 and has continued to support supervisors in building a robust intelligence picture of relevant sectors. The Treasury also published the UK’s first PF NRA in 2021.

Work on the next NRA on ML/TF is underway, underpinned by a rigorous process undertaken in collaboration with law enforcement, UK government departments and other key stakeholders to identify and assess risks. It will be published in 2025. The Treasury has also begun the process of updating the PF NRA which will be published in due course.

The role of supervision in sanctions compliance

Following Russia’s full-scale invasion of Ukraine in February 2022, the government acted quickly to impose an unprecedented package of coordinated sanctions alongside our international partners.

UK persons, including supervised firms, are required under the Sanctions and Anti-Money Laundering Act (SAMLA) to screen their activity against the UK sanctions list, to prevent funds, economic resources or services being provided to designated persons or for the provision of any other prohibited activity. Additionally, under the MLRs, supervisors should consider the systems and controls that a relevant firm has in place to mitigate the risks of breaching relevant sanctions relating to counter-terrorism and counter-proliferation sanctions, as part of their AML/CTF compliance checks.

Methodology for this report and additional metrics for 2023-24

This report is informed by an annual data return which HM Treasury collects from all AML/CTF supervisors in accordance with Regulation 51 of the MLRs. The return consists of a quantitative datasheet with key metrics across the main areas of supervisory activity, and a qualitative return which allows supervisors to provide more detail around their activities across the relevant period (including case studies). Types of data that supervisors are required to collect and submit to HM Treasury are set out in Schedule 4 of the MLRs, but data requests are subject to change from year to year.

For the 2023-24 reporting period, HM Treasury requested several new metrics as part of the quantitative return. This reflected our commitment under ECP2 to develop a framework to better evaluate the effectiveness of AML/CTF supervision, in order to enhance HMT oversight of the supervisors and support the continuous improvement of supervision. The additional metrics were developed with input from all supervisors, as well as OPBAS and the National Crime Agency, and were designed with FATF methodology in mind to include data that will be required as part of the UK’s next Mutual Evaluation Report (MER).

Since data collection for some of the new metrics was not possible retrospectively, for the 2023-24 reporting period supervisors were asked to provide this data on a ‘best endeavours’ basis, with a view to providing the data in full for the 2024-25 period. As a result, this year’s report only includes metrics where most or all supervisors were able to provide a figure. The new metrics in this report are as follows:

Supervision activities

-

Onsite visits and desk-based reviews split by risk categorisation.

-

Businesses assessed via supervisory interventions other than onsite visits or desk-based reviews.

-

Proportion of businesses found to be non-compliant or require a higher risk categorisation after being randomly selected for assessment.

-

Number of Suspicious Activity Reports (SARs) assessed by supervisors for quality, and how many of those were assessed as inadequate.

Ensuring compliance

-

Formal and informal enforcement actions split by risk categorisation.

-

Fines split by risk categorisation.

-

Number of enforcement actions published online.

-

Number of unregistered businesses identified as undertaking AML/CTF-regulated activity, and the enforcement actions taken against them.

Cooperation, coordination and information sharing

-

Number of guidance/training materials shared related to money laundering and terrorist financing risk.

-

Number of guidance/training materials shared relating to compliance with the MLRs.

-

Average email open rates, monthly hits, and attendance/views.

-

Numbers related to referrals, disclosures and information requests made under various AML/CTF-related information- and intelligence-sharing gateways.

The new metrics build on the data already requested of supervisors to capture the pillars of effective supervision, such as improved firm understanding of risk and AML/CTF obligations. The new metrics also have a renewed focus on the effectiveness of supervisors’ own risk-based approach to supervision by asking for interventions and enforcement actions split by risk categorisation.

This year, the new metrics begin to transition from merely counting the number of interventions a supervisor makes, to assessing the effectiveness of those interventions. This is achieved by examining outcomes of assessments and any subsequent changes in compliance ratings. However, as the data provided this year was on a ‘best endeavours’ basis to allow for supervisors to restructure their data gathering processes, HM Treasury anticipates having a more comprehensive picture next year.

Taken together with existing data, the new metrics will enable HM Treasury to build up a more holistic picture of each supervisor’s effectiveness over time. HM Treasury recognises, however, that not all metrics will be equally relevant for every supervisor and that the qualitative element of supervisors’ existing returns remain important to elaborate and contextualise the data provided (for more contextual information, see supervisors’ Regulation 46A reports in Annex C). Naturally, some metrics will be more helpful to assess individual supervisor trends over time and it is not possible to directly compare individual supervisors, given that every supervisor operates in a different context and with different constraints. HM Treasury also recognises the work involved for supervisors in collecting this data and remains committed to making the reporting process as streamlined as possible for supervisors going forwards.

HM Treasury has sought to capture the data reported by supervisors as accurately as possible, issuing clarification requests to supervisors where information was unclear or different to previous returns. It is important to note that some of these metrics are newly implemented and still in the process of being fully integrated. As such, caution should be exercised when interpreting them, as further refinement and clarification of definitions may be necessary.

2. Gatekeeping and risk assessment

This chapter covers supervisors’ work during 2023-24 to register businesses for supervision, and to understand the distribution of money laundering and terrorist financing risk across their population.

Effective gatekeeping

‘Gatekeeping’ is a core function of supervisors, ensuring that businesses in scope of the Money Laundering Regulations (MLRs) have registered for supervision and demonstrated they meet the minimum necessary standards. It involves checking as appropriate that the firms in question have the necessary systems in place to identify and prevent illicit financial flows, and that positions of significant influence over regulated businesses are not held by those who cannot demonstrate integrity and competence. All firms intending to carry out regulated activity should be subject to effective gatekeeping assessments, designed to be proportionate and not overly burdensome for legitimate business.

Supervisors deliver their gatekeeping function in different ways. Some integrate anti-money laundering/counter-terrorist financing (AML/CTF) registration and ‘fit and proper’ checks into broader processes for the purposes of their other functions. For instance, the FCA also supervises financial firms under the Financial Services and Markets Act (FSMA) and operates a broader Senior Managers and Certification Regime. Others, such as HMRC, carry out a dedicated AML/CTF registration process and AML/CTF-specific fit and proper checks on key individuals. The MLRs provide that, at a minimum, supervisors must ensure that key individuals in supervised firms have not been convicted of certain criminal offences including those related to money laundering, terrorist financing, fraud, tax evasion or organised crime.

Risk assessment

The MLRs require AML/CFT supervisors to take a risk-based approach to the supervision of their population. Supervisors must understand the ML/TF risks of their supervised populations to target resources effectively on monitoring the activities that are most likely to be exploited by criminals. This approach ensures that supervision is focused where it will have the greatest impact in ensuring businesses are detecting, deterring, and disrupting criminal activity, whilst minimising unnecessary burdens.

An effective risk-based approach requires a clear understanding of the supervised population; successfully differentiating between types of firms, the services they provide, their clients, and other sector-specific factors. In addition to supervisors’ own activities and knowledge of their sectors, there are various resources published by the government, law enforcement agencies, and leading international AML/CTF bodies to assist supervisors in building an understanding of ML/TF risks within their regulatory population. These include the UK’s National Risk Assessments, the National Crime Agency’s (NCA) risk assessments and briefings, and publications by the Financial Action Task Force (FATF).

For all tables in this chapter, the data for the 2021-22 and 2022-23 periods is included as a means of comparison with the data covered in the previous HM Treasury supervision report. It should be noted that due to the specific attributes and differences between the regulated sectors – including size of supervised population, differences in risk distribution within the population, and differing contexts in which the supervisors operate – it is not always appropriate to compare supervisors based on quantitative data alone.

Summary of activity across all supervisors

Supervisors received a total of 13,058 applications from businesses for AML/CTF supervision in 2023-24, with 954 of those rejected. However, this does not take into account that many businesses withdraw applications in anticipation of rejection. For comparison, there were 12,856 applications in 2022-23, with 742 rejected.

According to supervisors’ returns, approximately 9% of the supervised population were categorised as high-risk in 2023-24, compared to approximately 10% in 2022-23. This is broadly in line with prior years of 2021-22 (11%) and 2020-21 (9%).

Table 2.A Gatekeeping activity of all supervisors

| 2021-22 | 2022-23 | 2023-24 | |

|---|---|---|---|

| Total applications for supervision | 16,515 | 12,856 | 13,058 |

| Total applications rejected | 350 | 742 | 954 |

Source: HMT annual return data

Table 2.B 1. Risk assessment activity of all supervisors

| 2021-22 | 2022-23 | 2023-24 | |

|---|---|---|---|

| Total supervised population size | 101,098 | 95,914 | 94,937 |

| Proportion of supervised businesses assessed as high risk (%) | 11% | 10% | 9% |

| Proportion of supervised businesses assessed as medium risk (%) | 43% | 38% | 31% |

| Proportion of supervised businesses assessed as low risk (%) | 46% | 52% | 60% |

Source: HMT annual return data

The FCA’s gatekeeping and risk assessment activity

The Financial Conduct Authority (FCA) is the supervision authority for financial services firms and virtual asset service providers in the UK. The sectors which the FCA regulates include:

-

Retail banking

-

Wholesale financial market

-

Investment management

-

General insurance and protection

-

Retail lending

-

Retail investments

-

Pensions and retirement income

As well as supervision under the MLRs, the FCA also supervises firms under the FSMA, the Payment Services Regulations and the Electronic Money Regulations.

In 2023-24, approximately 17,200 firms were registered with the FCA for AML/CTF supervision. This number is an approximation because the precise number of firms supervised changes frequently due to the specific activities they undertake. The FCA’s total supervisory remit, including firms outside the scope of the MLRs, extends to around 42,000 firms.

Gatekeeping activity

As of January 2020, the FCA became the AML/CTF supervisor for cryptoasset businesses, such as exchanges and custodian wallets, which are active in the UK. The FCA’s gateway assessment for cryptoasset firms seeking to register for AML/CTF supervision involves reviewing each firm’s controls framework against the requirements in the MLRs. This is with a view to assessing the inherent risks that the applicant firm’s business model presents against the strength of its controls. The FCA’s assessment covers the design of the Business-wide Risk Assessment, Customer Due Diligence (CDD), Enhanced Due Diligence (EDD), Transaction Monitoring and Suspicious Activity policies and procedures. In 2023-24 this process identified significant weaknesses in cryptoasset firms’ controls, resulting in 86% of initial crypto registrations received being rejected, withdrawn or refused.

For FSMA firms, the FCA can assess fitness and propriety through several measures, including, for example, the Senior Managers & Certification Regime. Thus, as part of the examination of these firms, existing intelligence concerning fitness and propriety would be considered.

In the 2023-24 reporting period, the FCA received 275 applications for AML/CTF supervision with 154 approved (56%- 6 cryptoasset firms, 148 other firms), and 120 rejected, withdrawn or refused (44%- 36 cryptoasset, 84 other).

The FCA can issue ‘minded to refuse’ letters prior to declining an application for a licence to practice, which often leads to a firm withdrawing its application for supervision before a formal rejection.

Table 2.C The FCA’s gatekeeping activity

| 2021-22 | 2022-23 | 2023-24 | |

|---|---|---|---|

| Applications for supervision | 270 | 292 | 275 |

| Applications rejected | 161 | 142 | 120 |

Source: HMT annual return from the FCA

Risk assessment

The FCA’s approach to assessing ML/TF risk in its population starts with reviewing the risks in each sub-sector on a periodic basis as part of a ‘portfolio analysis’ exercise. This is led by FCA supervision teams with financial crime specialist supervisors feeding in their own views of ML/TF risks. The FCA combines this portfolio analysis with details from its financial crime supervisory and intelligence work, REP-CRIM data (financial crime data returns) received from around 5,700 firms, and external risk assessments from law enforcement to identify which sectors pose the greatest ML/TF risk and where greatest resource is directed.

Based on risk assessments of its sectors, the FCA’s view is that, in the reporting year 2023-24, retail banking, e-money, wholesale banking, wealth management and cryptoasset firms remained particularly vulnerable to financial crime and posed the greatest risk of being exploited for money laundering.

In the 2023-24 reporting period, the FCA categorised c3,000 firms within its population as high risk, c8,950 as medium risk, and c5,100 as low risk.

Table 2.D The FCA’s risk assessment activity

| 2021-22 | 2022-23 | 2023-24 | |

|---|---|---|---|

| Population size | Approx. 21,500 | Approx. 18,000 | Approx. 17,200 |

| Proportion of supervised businesses assessed as high risk | 23% | 25% | 17% |

| Proportion of supervised businesses assessed as medium risk | 72% | 69% | 53% |

| Proportion of supervised businesses assessed as low risk | 5% | 6% | 30% |

Source: HMT annual return from the FCA

The Gambling Commission’s gatekeeping and risk assessment activity

The Gambling Commission (GC) is the AML/CTF supervisory authority for all online (remote) and land-based (non-remote) casinos operating in Great Britain or providing casino facilities to British customers. The Gambling Commission is also the regulator for other gambling businesses operating in Great Britain or providing gambling services to British customers, including betting, lotteries, bingo, and arcades.

During the 2023-24 reporting period, the total size of the GC’s supervised population was 247, and the majority of supervised casinos were remote casino operators.

Many remote and non-remote casinos have part, or all, of their ownership structure based outside of the UK. These jurisdictions vary, but the GC frequently sees companies, holding companies, trusts, and beneficial owners based in the British Virgin Islands, Cyprus, Malta, Sweden, Israel, and the United States.

Gatekeeping activity

Any gambling company operating in Great Britain, or with customers based in Great Britain, must hold the appropriate licence issued by the GC. Within these licenced businesses, individuals who hold certain key management functions must hold personal management licences issued by the GC. Holders of personal management licences and personal functional licences are subject to a five-year maintenance cycle where, every five years, their identity, integrity, and criminality is reassessed. Licensees are also required to report certain events to the GC, including if they are subject to any criminal investigation or disciplinary sanction.

The GC has the power to issue these licences under the Gambling Act 2005 and, through specialist guidance and support from their AML team, considers AML/CTF compliance when assessing new licence applications.

The GC also regulates individuals who work within the casino sector. In the 2023-24 reporting period, this amounted to 11,622 personal functional licences and 2,053 personal management licences.

In the reporting period, the GC received 14 applications for casino licences, with 11 granted. Of the 11 granted, four were for entities where the GC already licensed one or more companies in the group, one was from an existing licensee, and six applications were for new licencees. Two applications were withdrawn after the GC issued ‘minded to refuse’ letters, while one was rejected for non-payment. The data for previous years was not collected on the basis that the GC does not register businesses but licenses them instead; for the purposes of this year’s data, HM Treasury considers licence applications to be equivalent to registration applications.

Table 2.E The GC’s gatekeeping activity

| 2021-22 | 2022-23 | 2023-24 | |

|---|---|---|---|

| Applications for supervision | Data not collected | Data not collected | 14 |

| Applications rejected | Data not collected | Data not collected | 1 |

Source: HMT annual return from the GC

Risk assessment

The GC’s ML/TF risk assessment of the gambling industry (which covers all gambling sectors) was published in November 2023. The risk assessment identified remote gambling, particularly remote casinos and betting, along with non-remote casino and off-course betting, as being exposed to a high risk of money laundering. In addition, the risk assessment identified that gambling is currently at medium risk of being exposed to terrorist financing.

The GC assessed that the remote casino sector continued to demonstrate a high risk of non-compliance with the MLRs. Customers not being physically present for identification and verification purposes continued to pose a high risk in relation to stolen or fraudulent identification, enabling criminals to spend their proceeds of crime through gambling.

The non-remote casino sector continued to be rated as having a higher ML risk relative to other gambling sectors. Widespread compliance failings, particularly in relation to personal management, licence holders’ competency levels and inadequate CDD and EDD checks have enabled high levels of transactions to occur.

In the 2023-24 reporting period, there were 97 high, 37 medium, and 113 low risk firms identified.

Table 2.F The GC’s risk assessment activity

| 2021-22 | 2022-23 | 2023-24 | |

|---|---|---|---|

| Population size | 265 | 263 | 247 |

| Proportion of supervised businesses assessed as high risk | 33% | 42% | 39% |

| Proportion of supervised businesses assessed as medium risk | 5% | 7% | 15% |

| Proportion of supervised businesses assessed as low risk | 62% | 51% | 46% |

Source: HMT annual return from the GC

HMRC’s gatekeeping and risk assessment activity

HMRC is the supervisory body for estate agency businesses, letting agency businesses, art market participants, high value dealers, money service businesses, bill payment service providers, telecommunications, digital and IT payment services, trust and company service providers who are not supervised by the FCA or PBSs, and accountancy service providers who are not supervised by one of the accountancy PBSs.

The total size of the population supervised by HMRC was 36,096 in 2023-24, consisting of 27,803 firms and 8,293 sole practitioners. At the time the annual returns were completed, these totals broke down by sector as follows:

Table 2.G Breakdown of HMRC’s supervised businesses

| Sector | Number of supervised businesses (2022/23) | Number of supervised businesses (2023/24) | Year on year change |

|---|---|---|---|

| Accountancy Service Providers | 16504 | 16422 | -82 |

| Art Market Participants | 1135 | 1264 | +129 |

| Bill Payment Service Providers | 273 | 246 | -27 |

| Estate Agency Businesses | 15234 | 16450 | +1216 |

| High Value Dealers | 310 | 251 | -59 |

| Letting Agency Businesses | 1921 | 2149 | +228 |

| Money Service Businesses | 1049 | 983 | -66 |

| Telecommunications, Digital and IT Payment Service Providers | 82 | 71 | -11 |

| Trust and Company Service Providers | 1540 | 1553 | +13 |

| Total HMRC | 35411 | 36096 | +685 |

Source: HMT annual return from HMRC

Gatekeeping activity

In 2023/24 HMRC received 9,893 applications for AML supervision, with 8,404 accepted and 601 rejected; the remainder were still to be determined at the end of the reporting period. The percentage of refusals was highest in the money service business, trust and company service provider, and high value dealer sectors.

HMRC is required to conduct fit and proper tests on certain individuals within money service businesses and trust and company service providers. In addition, HMRC is required to carry out criminality tests for key individuals in accountancy service providers, art market participants, high value dealers, estate agency businesses and letting agency businesses to ensure that individuals with a relevant criminal conviction are not able to hold relevant positions. In the 2023-24 reporting period, HMRC received 89,976 applications for Beneficial Owners, Officers or Managers (BOOM) approval, with 62,288 approved, 42 rejected and 213 invalidated by disciplinary measures.

Table 2.H HMRC’s gatekeeping activity

| 2021-22 | 2022-23 | 2023-24 | |

|---|---|---|---|

| Applications for supervision | 13,196 | 9,967 | 9,893 |

| Applications rejected | 21 | 438 | 601 |

Source: HMT annual return from HMRC

Risk assessment

HMRC draws on external reports to conduct detailed risk assessments for each sector, such as the National Risk Assessment, FATF publications, and information from HM Treasury, the Home Office, the NCA, and HMRC’s Risk and Intelligence Service. It also draws on findings from its own investigations into the sectors and the knowledge of experienced staff.

Overall, HMRC reported that most firms and sole practitioners within their supervised population were classified as low risk for 2023-24, but that 9% and 38% were considered high and medium risk, respectively.

However, these high and medium risk firms are not evenly distributed across all of HMRC’s sectors. HMRC identified money service businesses, art market participants, and trust and company service providers as the sectors presenting the highest inherent risks for money laundering. Money service businesses were also identified as presenting the highest inherent risk of being exploited for terrorist financing.

HMRC does not consider that each business within these sectors represents the same level of risk, however. Instead, it considers factors such as the nature of the product offered, geographical risk and client size, while also considering the impact on risk of business size, scope or reach, and any potential relationships or links to other businesses.

Table 2.I HMRC’s risk assessment activity

| 2021-22 | 2022-23 | 2023-24 | |

|---|---|---|---|

| Population size | 36,960 | 35,411 | 36,096 |

| Proportion of supervised businesses assessed as high risk | 7% | 4% | 7% |

| Proportion of supervised businesses assessed as medium risk | 26% | 27% | 30% |

| Proportion of supervised businesses assessed as low risk | 67% | 69% | 73% |

Source: HMT annual return from HMRC

Gatekeeping and risk assessment activity by the Professional Body Supervisors

The 22 Professional Body Supervisors (PBSs) are responsible for AML/CTF supervision for the accountancy and legal sectors. These cover a range of services including accountancy, auditing, bookkeeping, legal, and notarial. The sizes of PBSs’ supervised populations vary from fewer than 10 to just under 10,000. Some PBSs supervise both firms and sole practitioners, whereas others solely supervise one of these types of business.

During the 2023-24 reporting period, there were 33,830 accountancy businesses and 7,564 legal businesses supervised by PBSs. Of the supervised businesses in the accountancy sector, 57% were firms and 43% were sole practitioners. Of the supervised businesses in the legal sector, 74% were firms and 26% were sole practitioners.

Gatekeeping activity

PBSs have rejected a higher percentage of registration applications than in previous reporting periods, with the proportion of applications rejected by PBSs increasing to 7.5% from 6.2% in 2022-23 and 5.5% in 2021-22. In all, PBSs received 3,108 applications for supervision in the 2023-24 reporting period, with 2,811 of those accepted and 233 rejected. The difference between the number of applications received but not reported as approved /rejected is due to those applications still being assessed at the end of the reporting period.

Some PBSs, such as the Bar Standards Board, authorise firms to practice rather than provide membership.

In addition to their own professional body ‘fit and proper’ checks and standards, under Regulation 26 of the MLRs, supervisors have a responsibility to approve beneficial owners, officers, or managers of firms (BOOMs). The processes used by PBSs to evaluate applications for new regulated entities and to determine whether to provide them with the authority to practice in the legal and accountancy sectors vary from supervisor to supervisor, but some examples are:

-

Requiring evidence of staff having received sufficient AML/CTF training.

-

Requiring evidence of staff holding certain qualifications.

-

Requiring evidence of staff having relevant work experience in the AML sector.

PBSs must also receive sufficient information to determine whether an individual applying for approval has been convicted of a relevant criminal offence, which would include evidence of a criminality check.

In the 2023-24 reporting period, PBSs received 9,085 applications for BOOM approval, with 8,857 accepted and 210 rejected. The remainder were invalidated by disciplinary measures.

Risk assessment

Of the population supervised by PBSs in 2023-24, 8% were identified as high risk, 22% as medium risk, and 70% as low risk. Due to the diverse nature of their populations and distribution of ML/TF risk within their supervised populations, percentages of supervised businesses in each risk category vary significantly between PBSs. However, high/medium/low risk assessments are undertaken by each PBS using its own criteria and therefore may not be directly comparable.

Table 2.J Gatekeeping activity by the Professional Body Supervisors

| 2021 - 22 | 2022 - 23 | 2023 - 24 | ||||

|---|---|---|---|---|---|---|

| Supervisors | Applications for supervision | Applications rejected | Applications for supervision | Applications rejected | Applications for supervision | Applications rejected |

| ACCA (Association of Chartered Certified Accountants) | 646 | 0 | 391 | 0 | 345 | 0 |

| AIA (Association of International Accountants) | 35 | 2 | 45 | 1 | 57 | 3 |

| CIMA (Chartered Institute of Management Accountants) | 151 | 8 | 115 | 5 | 105 | 6 |

| CIOT (Chartered Institute Of Taxation) | 88 | 4 | 94 | 17 | 84 | 22 |

| ATT (Association of Taxation Technicians) | 45 | 5 | 39 | 8 | 72 | 11 |

| ICAEW (Institute of Chartered Accountants in England and Wales) | 141 | 0 | 122 | 1 | 142 | 0 |

| ICAI (Institute of Chartered Accountants in Ireland) | 0 | 0 | 24 | 0 | 24 | 0 |

| ICAS (Institute of Chartered Accountants of Scotland) | 132 | 0 | 142 | 0 | 148 | 0 |

| ICB (Institute of Certified Bookkeepers) | 259 | 0 | 279 | 5 | 238 | 3 |

| IFA (Institute of Financial Accountants) | 223 | 55 | 121 | 37 | 140 | 32 |

| AAT (Association of Accounting Technicians) | 771 | 88 | 687 | 85 | 1215 | 150 |

| IAB (Institute of Accountants and Bookkeepers) | 149 | 4 | 168 | 1 | 152 | 2 |

| IPA (Insolvency Practitioners Association) | 6 | 2 | 6 | 1 | 50 | 0 |

| SRA (Solicitors Regulation Authority) | 449 | 0 | 231 | 0 | 218 | 0 |

| Law Society of Northern Ireland | 6 | 0 | 4 | 0 | 3 | 0 |

| Law Society of Scotland | 22 | 0 | 18 | 0 | 11 | 0 |

| CLC (Council for Licensed Conveyancers) | 10 | 0 | 9 | 1 | 8 | 3 |

| BSB (Bar Standards Board - General Council of the Bar) | 0 | 0 | 0 | 0 | 0 | 0 |

| General Council of the Bar Northern Ireland | 0 | 0 | 0 | 0 | 0 | 0 |

| CILEx (Chartered Institute of Legal Executives) | 5 | 0 | 1 | 0 | 0 | 0 |

| Faculty of Advocates | 1 | 0 | 1 | 0 | 1 | 0 |

| Faculty Office of the Archbishop of Canterbury | 46 | 0 | 124 | 0 | 119 | 1 |

| Total PBSs | 3,185 | 168 | 2,597 | 162 | 3,108 | 233 |

| Accountancy PBSs | 2,646 | 168 | 2,209 | 161 | 2,748 | 229 |

| Legal PBSs | 539 | 0 | 388 | 1 | 360 | 4 |

Source: HMT annual returns from the PBSs

Table 2.K Risk assessment activity by the Professional Body Supervisors

| 2021-22 | 2022-23 | 2023-24 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Supervisors | Population size | High risk | Medium risk | Low risk | Population size | High risk | Medium risk | Low risk | Population size | High risk | Medium risk | Low risk |

| ACCA | 6,846 | 13% | 18% | 70% | 6,951 | 13% | 17% | 70% | 6,995 | 8% | 17% | 75% |

| AIA | 314 | 11% | 17% | 71% | 320 | 8% | 18% | 74% | 338 | 7% | 20% | 72% |

| CIMA | 1,598 | 1% | 6% | 93% | 1,619 | 2% | 13% | 85% | 1,646 | 3% | 13% | 85% |

| CIOT | 889 | 6% | 91% | 3% | 860 | 8% | 90% | 2% | 858 | 12% | 87% | 1% |

| ATT | 590 | 4% | 93% | 3% | 595 | 4% | 92% | 4% | 618 | 11% | 87% | 2% |

| ICAEW | 10,476 | 3% | 67% | 31% | 10,402 | 2% | 67% | 30% | 9,911 | 3% | 68% | 29% |

| ICAI | 462 | 0% | 3% | 96% | 471 | 1% | 29% | 70% | 468 | 1% | 30% | 69% |

| ICAS | 881 | 5% | 20% | 75% | 824 | 5% | 29% | 67% | 758 | 5% | 22% | 73% |

| ICB | 3,036 | 0% | 0% | 0% | 3,098 | 27% | 9% | 64% | 3,171 | 26% | 9% | 65% |

| IFA | 1,983 | 15% | 43% | 42% | 1,981 | 17% | 30% | 53% | 1,815 | 14% | 26% | 60% |

| AAT | 5,856 | 3% | 41% | 56% | 6,202 | 6% | 43% | 51% | 6,337 | 4% | 40% | 56% |

| IAB | 704 | 40% | 54% | 7% | 719 | 40% | 51% | 9% | 744 | 43% | 46% | 12% |

| IPA | 276 | 7% | 58% | 35% | 267 | 6% | 55% | 40% | 171 | 16% | 53% | 31% |

| SRA | 6,408 | 5% | 30% | 65% | 6,007 | 3% | 1% | 96% | 5,683 | 3% | 5% | 92% |

| Law Society of Northern Ireland | 450 | 11% | 66% | 22% | 435 | 12% | 69% | 19% | 427 | 15% | 66% | 19% |

| Law Society of Scotland | 721 | 8% | 48% | 44% | 686 | 3% | 33% | 64% | 647 | 8% | 26% | 66% |

| CLC | 226 | 5% | 11% | 84% | 231 | 11% | 11% | 77% | 205 | 13% | 11% | 76% |

| BSB | 489 | 0% | 0% | 100% | 486 | 0% | 0% | 100% | 466 | 1% | 10% | 89% |

| General Council of the Bar Northern Ireland | 0 | N/A | N/A | N/A | 0 | N/A | N/A | N/A | 0 | N/A | N/A | N/A |

| CILEx | 28 | 29% | 39% | 32% | 21 | 14% | 43% | 43% | 10 | 0% | 0% | 100% |

| Faculty of Advocates | 7 | 0% | 0% | 100% | 8 | 0% | 0% | 100% | 8 | 0% | 0% | 100% |

| Faculty Office of the Archbishop of Canterbury | 133 | 73% | 27% | 0% | 124 | 14% | 28% | 58% | 118 | 16% | 31% | 53% |

Source: HMT annual returns from the PBSs (acronyms can be found in Table 2.J or Annex A)

3. Monitoring supervised businesses

The Money Laundering Regulations (MLRs) require supervisors to monitor their supervised populations effectively and to vary the frequency and intensity of their supervision based on the different risk profiles within their supervised populations.

Risk-based approach to supervision

Supervisors use a range of tools to assess whether firms are complying with the MLRs, including:

-

Desk-based reviews (DBRs) – these will typically be based on a review by the supervisor of documents provided by the firm to demonstrate the adequacy of its Anti-Money Laundering/Counter-Terrorist Financing (AML/CTF) policies, controls and procedures. Relevant documents might include the firm’s ML/TF risk assessment, examples of customer due diligence for a sample of clients, and staff training records. Supervisors will often supplement this with a questionnaire, or in some cases a virtual or telephone interview with the firm’s Money Laundering Reporting Officer (MLRO), or other members of staff. DBRs will conclude with the communication to the firm of the outcome of the review and any recommendations for improvements. Where more serious issues are identified, the supervisor will undertake follow-up work with the firm or initiate formal enforcement action (see Chapter 4).

-

Onsite visits – these are generally expected to involve an in-person visit to the firm’s premises or place of work, and are often combined with desk-based work. Onsite visits allow supervisors to verify that adequate policies, procedures and controls are in place, as well as to secure the benefits of in-person interviews with the firm’s MLRO or other members of staff.

-

Other supervisory interventions – This year for the first time we have asked supervisors to record the number of other interventions they undertake apart from DBRs and onsite visits, in order to gain a more holistic overview of their work. These are interventions which are not intended to allow for a formal judgement to be reached about a firm’s compliance (as with DBRs and onsite visits), but are a key component of a supervisor’s risk-based approach. These might include questionnaires aimed at a particular sub-sector of firms, engagement with boards and senior management to discuss specific aspects of compliance, or reviews of data held by the supervisor to look for ‘red flags’ which may indicate poor compliance by one or more firms. These interventions may act as a trigger for a DBR or onsite visit based on issues identified.

Onsite visits and DBRs can be categorised as ‘full-scope’ or ‘targeted’. Full-scope assessments involve a comprehensive review of a firm’s risks, compliance, policies, procedures, training and reporting, and may include a Customer Due Diligence (CDD) file review. Targeted assessments focus on specific aspects of a firm’s AML activity, including one or more of the elements of a full-scope assessment. While a full-scope assessment will be comprehensive enough to allow the supervisor to reach a judgement about whether the firm is compliant, generally compliant or non-compliant overall, a targeted assessment will only allow a judgement to be reached about the firm’s compliance with the specific aspect being assessed. This is the first year of annual reporting that this distinction has been recorded.

This section of the report presents data from AML/CTF supervisors’ annual returns to HM Treasury, detailing the number and type of supervision interventions (onsite visits, DBRs and other interventions). For the first time, the data is broken down by the risk level of the firm being assessed (as determined by the supervisors’ risk assessment processes) and by whether assessments were ‘targeted’ or ‘full-scope’. Additionally, it includes the outcomes of supervisors’ assessments in terms of whether firms were found to be compliant/generally compliant/non-compliant, also split by risk. It also includes data on full-time equivalent (FTE) staff and the amount of money spent by each supervisor on AML/CTF, as well as data on supervisors’ quality assurance of Suspicious Activity Reports (SARs).

For all tables in this chapter, the data for the 2021-22 and 2022-23 periods is included as a means of comparison with the data covered in the previous HM Treasury supervision report. It should be noted that due to the specific attributes and differences between the regulated sectors – including size of supervised population, differences in risk distribution within the population, and differing contexts in which the supervisors operate – it is not always appropriate to compare supervisors based on quantitative data alone.

Summary of activity across all supervisors

There were a total of 9,013 direct supervision actions (desk-based reviews and onsite visits) conducted across all 25 supervisors in 2023-24, representing the highest total since the pre-pandemic figure of 10,550 in 2019-20. This represents 10% of supervised firms being subject to direct supervision action in 2023-24, compared to 6% in 2022-23; the pre-pandemic figure was 11% in 2019-20.

There were a total of 708 FTE (Full Time Equivalent) staff and a total expenditure of £45m dedicated to AML/CTF supervision across all supervisors in 2023-24. However, it is difficult to calculate exact figures as the AML/CTF function of many supervisors is integrated into wider supervision activity; these figures therefore represent a ‘best estimate’.

In the reporting period 2023-24, 996 firms were asked to share SARs with their supervisor, with 466 of those being assessed by a supervisor for quality. Of those, 52 were assessed as inadequate because they did not have glossary codes, and a further 5 were assessed as inadequate for other reasons.

There was significant variation in supervisors’ approaches as to how they used the supervisory tools at their disposal. Some supervisors increased their focus on onsite visits, while others continued to invest more in DBRs. Some supervisors increasingly pursue innovative methods of supervision, such as the FCA’s in-house data analysis tools that tap into multiple data sources (see below).

Table 3.A Supervision activity of all supervisors

| 2021-22 | 2022-23 | 2023-24 | |

|---|---|---|---|

| Total number of DBRs and onsite visits as a % of total supervised population | 5% | 6% | 10% |

| Total FTE staff dedicated to AML/CTF | 458 | 508 | 708 |

| Total expenditure on AML/CTF | £33m | £35.5m | £45m |

| Firms asked to share SARs | 490 | 657 | 996 |

Source: HMT annual return data

The FCA’s monitoring activity

In 2023-24 there were 77 full-time financial crime specialist employees dedicated to AML/CTF supervision at the FCA, including dedicated resources being applied to the assessment and supervision of cryptoasset businesses in particular. The FCA spent an estimated £6m on AML/CTF supervision in the reporting period. However, these figures do not include staff and resources in the FCA’s wider supervision and enforcement teams, which will also contribute to AML/CTF supervision.

The FCA’s supervision approach in 2023-24 was intended to be agile, risk-based, and targeted, making significant enhancements to their AML/CTF supervisory programmes to be data-led and proportionate over the last 2-3 years to get maximum coverage of their supervised population.

The key elements of the data-led approach included:

-

Modular Assessment Proactive Programme (MAPP): This approach replaced the FCA’s previous Systematic AML Programme (SAMLP). It focuses on reviewing specific financial crime risks across multiple firms simultaneously, allowing the FCA to more frequently assess the largest and most important firms and to compare risk mitigation across them.

-

Outliers/Proactive AML Programme (PAMLP): The FCA developed in-house data analysis tools that tapped into REP-CRIM (the annual AML return submitted by firms) and other data sources. The tool analysed large amounts of firm data to identify hotspots, outliers, and emerging themes, driving supervisory attention and focus.

-

Focused Supervisory Interventions (FSI): The FCA targeted engagement with firms on specific issues or risk indicators identified through assessing firm-related data and intelligence. This ongoing work enabled various sectors to understand their potential micro and macro financial crime risks and respond accordingly.

-

Multi-firm work: The FCA undertook multi-firm work to identify risks, conduct reviews, and provide feedback to individual firms and the industry.

Risk and compliance assessments

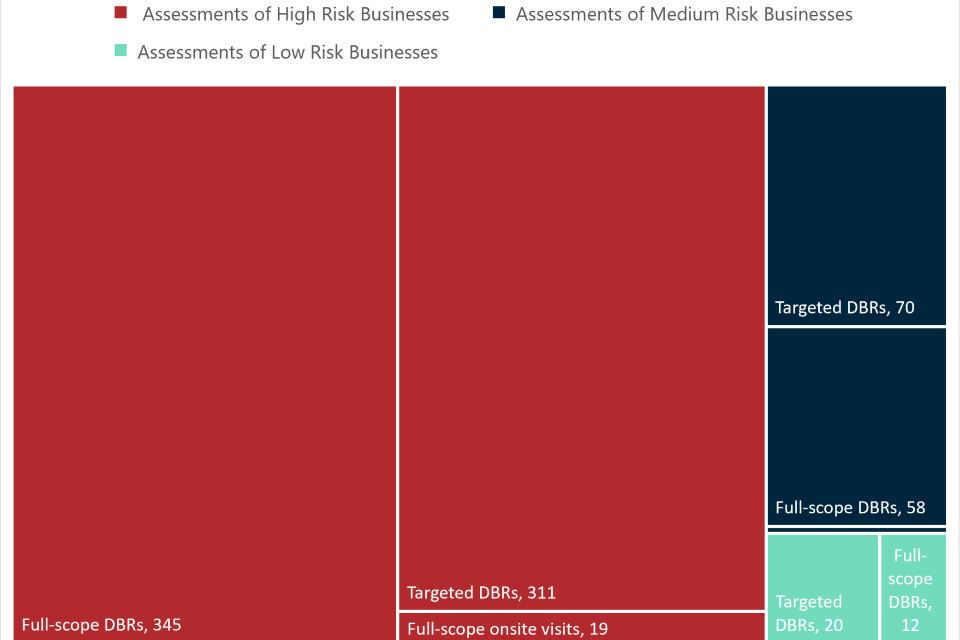

During the 2023-24 reporting period, the financial crime specialists within the FCA conducted a total of 816 DBRs and 21 onsite visits.

Table 3.B The FCA’s Desk Based Reviews and onsite visits, split by risk

Table 3.B The FCA’s Desk Based Reviews and onsite visits, split by risk

Source: HMT annual return from the FCA

Of the DBRs, 656 (345 full-scope, 311 targeted) were completed on high-risk firms, 128 (58 full-scope, 70 targeted) on medium-risk firms, and 32 (12 full-scope, 20 targeted) on low-risk firms. Of the onsite visits, 19 full-scope visits were conducted on high-risk businesses with a further 2 full-scope visits on medium-risk businesses.

The FCA reported that of the firms subject to an assessment by financial crime specialists in 2023-24, 7% were found to be compliant, 19% were generally compliant and 3% were non-compliant. The remaining assessments conducted did not reach a point in the FCA’s review cycle by which the final rating could be determined for the reporting year 2023-24.

Common issues of non-compliance identified by the FCA through DBRs, onsite visits and multi-firm work included:

-

Ineffective ML business-wide risk assessments.

-

Customer risk assessments not always being in place or not sufficiently holistic and robust.

-

Enhanced due diligence not risk-sensitive and granular.

-

Compliance monitoring needing improvement and quality assurance.

Other supervisory interventions

Throughout the reporting period, the FCA issued ‘Dear CEO’ letters addressed to firms highlighting areas of weaknesses and where improvements were expected. The FCA sent 171 firms ‘Dear CEO’ letters in 2023-24.

Table 3.C The FCA’s monitoring activity

| 2021-22 | 2022-23 | 2023-24 | |

|---|---|---|---|

| Total DBRs | 78 | 231 | 816 |

| Total onsite visits | 0 | 7 | 21 |

| FTE staff dedicated to AML/CTF | 40.4 | 52.8 | 77 |

| Estimated expenditure on AML/CTF | £3.5m | £4m | £6m |

| % of businesses assessed as compliant | 36% | 43% | 7% |

| % of businesses assessed as generally compliant | 13% | 16% | 19% |

| % of businesses assessed as non-compliant | 22% | 4% | 3% |

Source: HMT annual return from the FCA

Box 3.A Case study: the FCA’s monitoring activity

-

As of 10 January 2020, the FCA became the AML/CTF supervisor for cryptoasset businesses who are active in the UK. 44 firms are now registered with the FCA and supervised under the MLRs.

-

In the 2023-24 reporting period, 83 assessments were conducted amongst these 44 firms. These include: 12 targeted desk-based reviews, 2 full-scope onsite visits, and 69 full-scope desk-based reviews. This supervisory work identified a range of MLR-related issues which led to remedial work undertaken by those firms.

-

The FCA has stressed to the sector the importance of adherence to the MLRs and that it will take action where it sees actual/potential serious misconduct using the powers it has under the MLRs by either imposing or issuing a direction or opening an investigation into firms, where necessary and appropriate.

-

The FCA continues to address the issue of unregistered cryptoasset businesses by maintaining a list of those believed to be operating without registration. This list helps identify entities unaware of or refusing to comply with registration requirements and is regularly updated based on new information or responses from listed businesses.

-

For the three largest crypto firms and for 12 other large crypto firms, not FCA-registered but advertising legally into the UK, the FCA have adopted an ‘enhanced’ supervisory model which takes a more proactive approach to these firms’ supervision. A priority is assessing these firms’ financial crime controls, and the FCA have a named supervisor for each of these firms.

The Gambling Commission’s monitoring activity

During the 2023-24 reporting period, the Gambling Commission (GC) had 5 full-time employees dedicated to AML/CTF. However, AML/CTF work is integrated into the wider work of the GC, with 159 supporting employees in licensing, enforcement, compliance, intelligence, legal and forensic accountant teams. The GC spent an estimated £227,700 on AML supervision, with the caveat that as AML/CTF supervision is not the sole focus for the majority of the teams, it is difficult to provide an accurate estimate of expenditure; accordingly, the AML/CTF expenditure figure relates to expenses mainly within the AML team.

Risk and compliance assessments

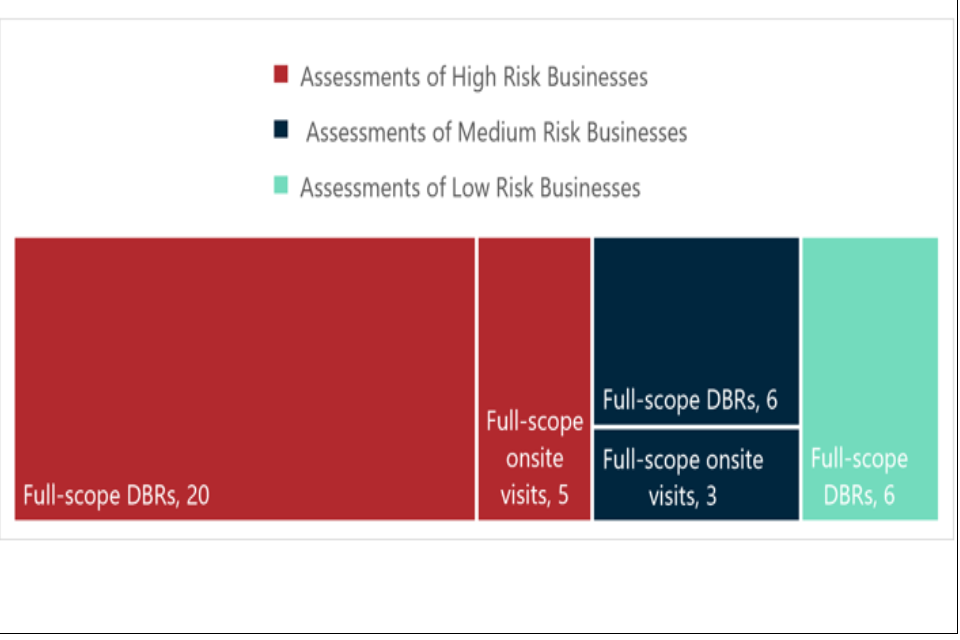

During the 2023-24 reporting period, the GC carried out a total of 32 DBRs and 8 onsite visits; all of these were full-scope as opposed to targeted. Of the DBRs, 20 were completed on high-risk firms, 6 on medium-risk firms, and 6 on low-risk firms. Of the onsite visits, 5 were conducted on high-risk businesses with a further 3 on medium-risk businesses.

Table 3.D The GC’s Desk Based Reviews and onsite visits, split by risk

Table 3.D The GC’s Desk Based Reviews and onsite visits, split by risk

Source: HMT annual return from the GC

During the 2023-24 reporting period, the GC found that of the firms subjected to a DBR or onsite visit, 50% were found to be compliant, 25% were generally compliant, and 25% were non-compliant.

Some causes of non-compliance identified by the GC over the reporting periods were:

-

Inadequate documented policies, procedures and controls.

-

Inadequate CDD procedures, or no ongoing CDD monitoring.

-

Inadequate client risk assessment records.

-

No periodic review of compliance with MLRs.

-

Inadequate training.

-

Inadequate firm-wide risk assessment.

-

Inadequate electronic checks or record retention.

-

Inadequate record keeping.

Other supervisory interventions

The GC has powers of entry to inspect, question, access written or electronic records, and remove and retain any items relevant to a suspected offence under the Gambling Act 2005, or a breach of a licence condition. Any gambling company operating in Great Britain or providing gambling services to British customers must hold the appropriate licence issued by the GC.

The GC also requires annual assurance statements from their highest impact operators. These statements are intended to be a concise self-assessment of the risks to the licensing objectives posed by the business, how well the business is managing those risks, where the business needs to improve, and how it will do so. This information is useful when combined with other information received from and about an operator, such as intelligence or ‘key event’ submissions, as the content can assist in determining the action the operator is taking in managing risks, which can then be tested during any compliance assessment.

Table 3.E The GC’s monitoring activity

| 2021-22 | 2022-23 | 2023-24 | |

|---|---|---|---|

| Total DBRs | 32 | 25 | 32 |

| Total onsite visits | 9 | 9 | 8 |

| FTE staff dedicated to AML/CTF | 4 | 4 | 5 |

| Estimated expenditure on AML/CTF | £212,900 | £193,400 | £227,700 |

| % of businesses assessed as compliant | 20% | 18% | 50% |

| % of businesses assessed as generally compliant | 29% | 23% | 25% |

| % of businesses assessed as non-compliant | 51% | 59% | 25% |

Source: HMT annual return from the GC

Box 3.B Case study: the GC’s monitoring activity

-

At the end of April 2023, members of the GC’s Compliance Team conducted an on-site assessment of a high-end casino in London.

-

This premises assessment looked at on-site controls and compliance, including AML provisions for ID verification, customer due diligence, cash handling (and other payment controls), staff knowledge and experience, and transaction/table monitoring procedures.

-

The premises assessment was followed by a full policies and procedures review, a day interviewing key individuals within the business about their controls, and two days reviewing customer records to test controls (including those relating to AML) in practice for effectiveness and implementation.

-

The assessment found that improvements were required to the operator’s ML/TF risk assessment, their customer due diligence process, the sanctions process and the enhanced customer due diligence process for Politically Exposed Persons (PEPs).

-

While issues were found in these areas, it was judged that there was not a significant risk to the licensing objectives under the Gambling Act (including keeping crime out of gambling), so the matter was not escalated for a Section 116 review. Instead, an Improvement Notice was issued. This required the operator to make improvements at pace in advance of the Commission conducting a follow-up assessment.

-

In October 2023, the follow-up assessment took place and the operator was found to have rectified the issues found in the original assessment and was therefore classed as compliant.

HMRC’s monitoring activity

HMRC had 412.6 full-time equivalent (FTE) employees dedicated to AML supervision in 2023-24. This demonstrates a year-on-year increase in supervisory staff from the 343 and 397 full-time employees dedicated to AML supervision in 2021-22 and 2022-23, respectively. HMRC’s total expenditure on AML/CTF supervision for 2023-24 was an estimated £23.5m.

Risk and compliance assessments

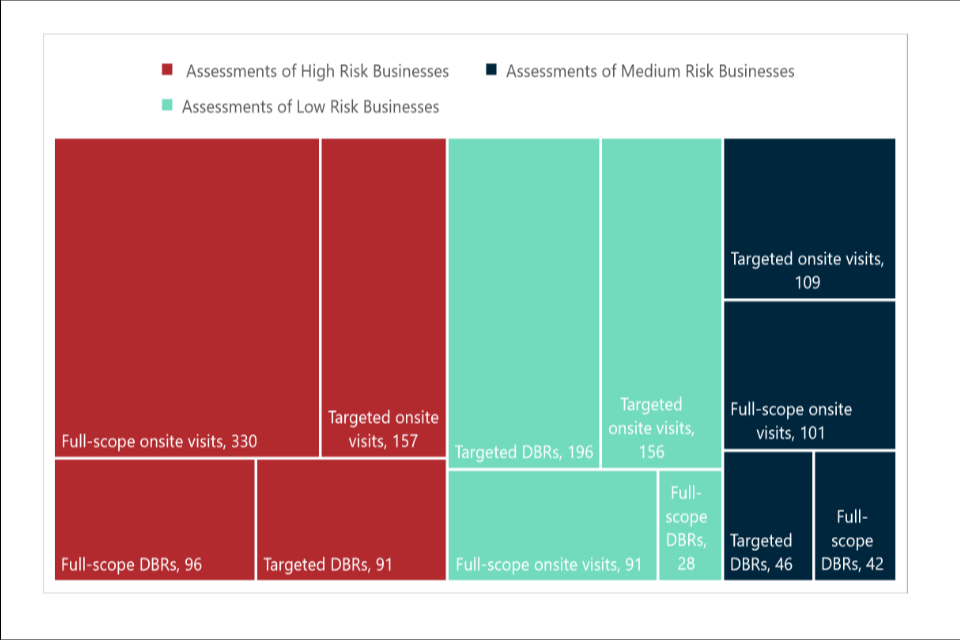

During the 2023-24 reporting period, HMRC conducted a total of 499 DBRs and 944 onsite visits.

Table 3.F HMRC’s Desk Based Reviews and onsite visits, split by risk

Table 3.F HMRC’s Desk Based Reviews and onsite visits, split by risk

Source: HMT annual return data from HMRC

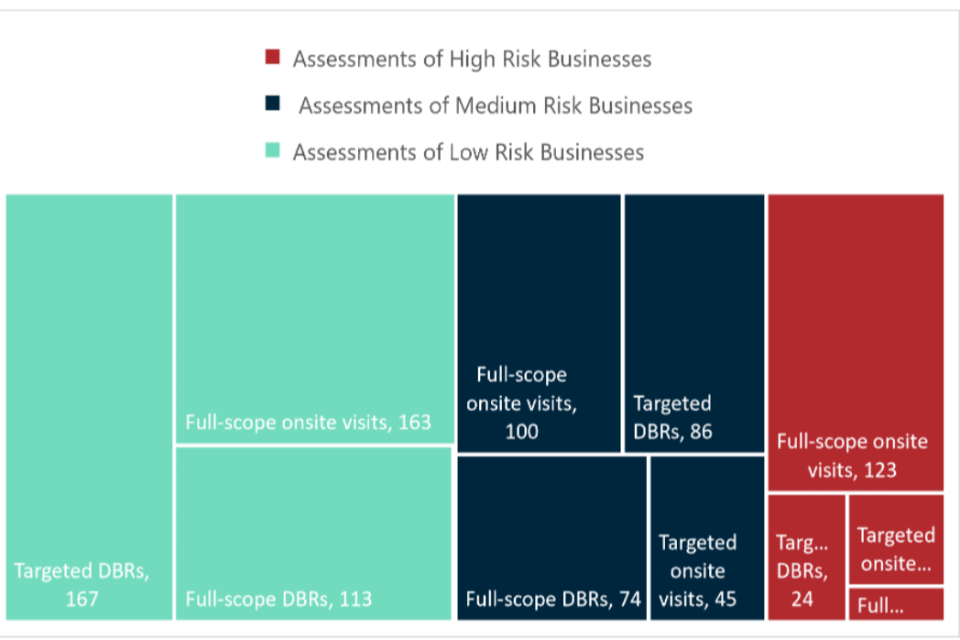

Of the DBRs, 187 (96 full-scope, 91 targeted) were completed on high-risk firms, 88 (42 full-scope, 46 targeted) on medium-risk firms, and 224 (28 full-scope, 196 targeted) on low-risk firms. Of the onsite visits, 487 (330 full-scope, 157 targeted) were conducted on high-risk businesses, 210 (101 full-scope, 109 targeted) were conducted on medium-risk businesses, and 247 (91 full-scope, 156 targeted) were conducted on low-risk businesses.

Of the 1,443 onsite visits and desk-based reviews conducted in 2023-24, 615 visits resulted in assessments of non-compliance (43%). The number of assessment outcomes may not equal the total number of interventions for a number of reasons, including where the case is closed without a supervision outcome such as where other law enforcement groups are leading the case.

HMRC also undertook intervention activity on firms that should have been registered for supervision, but were not, closing 323 of these cases in the reporting period.

The most frequent forms of non-compliance identified in cases closed by HMRC during the 2022-23 reporting period included:

-

Inadequate firm-wide risk assessment

-

Inadequate policies, controls, and procedures

-

Inadequate record-keeping

-

Inadequate customer due diligence measures, including in cases requiring enhanced customer due diligence

Other supervisory interventions

HMRC conducted Mass Market Interventions (MMIs) across 2023-24. MMIs are a light-touch intervention that aim to encourage businesses to comply with requirements by targeting specific areas of non-compliance, for example by prompting them to update their risk assessments, policies and controls. In 2023-24 HMRC undertook 996 MMIs, 35% of which were businesses whose registration had expired and who re-registered with HMRC within 4 weeks of contact.

In addition, HMRC undertook random dip-sampling of medium- and low-risk businesses to ensure that their risking processes were effective; 123 businesses were randomly selected for a DBR or an onsite visit, and of these, 46 were found to require a higher risk categorisation while 67 were found to be non-compliant.

Table 3.G HMRC’s monitoring activity

| 2021-22 | 2022-23 | 2023-24 | |

|---|---|---|---|

| Total DBRs | 1426 | 834 | 499 |

| Total onsite visits | 289 | 907 | 944 |

| FTE staff dedicated to AML/CTF | 343 | 397 | 412.6 |

| Estimated expenditure on AML/CTF | £25m | £27m | £23.5m |

| % of businesses assessed as compliant | 7% | 15% | 12% |

| % of businesses assessed as generally compliant | 15% | 17% | 17% |

| % of businesses assessed as non-compliant | 31% | 28% | 43% |

Source: HMT annual return from HMRC

Box 3.C Case study: HMRC’s monitoring activity

-

A business provided high risk Trust and Company Service Provider (TCSP) services of company formation, registered office, and nominee director/shareholder services but assessed the risk of providing these services to be low.

-

The business provided these services to both UK and offshore customers, including those operating in high risk third countries (geographic areas of operation risk).

-

The majority (90%) of services were provided without face-to-face contact with customers, but the business assessed this to be low risk (delivery channel risk).

-

The business failed to identify and assess the risks it was subject to, leading to a lack of appropriate policies, controls and procedures in place to mitigate those risks, include not applying EDD measures to high-risk customers.

-

In one instance, the business continued to offer services to clients via a business relationship with an intermediary customer despite that intermediary’s refusal to provide requested CDD information.

-

The Nominated Officer (NO) was provided with advice and guidance from HMRC throughout the intervention, beginning in early 2023, on steps to take to correct non-compliance identified, but this was not taken on board.

-

The business’ registration was cancelled, and it was determined to be not F&P (fit and proper) under MLR58, owing to the seriousness of its failings, their risk, and likelihood the NO would not comply with MLR obligations.

Monitoring activity by Professional Body Supervisors

Across the PBSs, there were 213 FTE employees dedicated to AML/CTF in 2023-24, just under the equivalent of 10 FTE per PBS. This continues a year-on-year increase from the reporting periods covered in previous supervision reports. The total expenditure on AML/CTF supervision of all PBSs for the reporting period was an estimated £15.5m. A PBS-by-PBS breakdown of staffing and expenditure levels can be found in Annex B. As noted above, due to the specific attributes and differences between the regulated sectors, it is not always appropriate to compare supervisors based on quantitative data alone.

Risk and compliance assessments

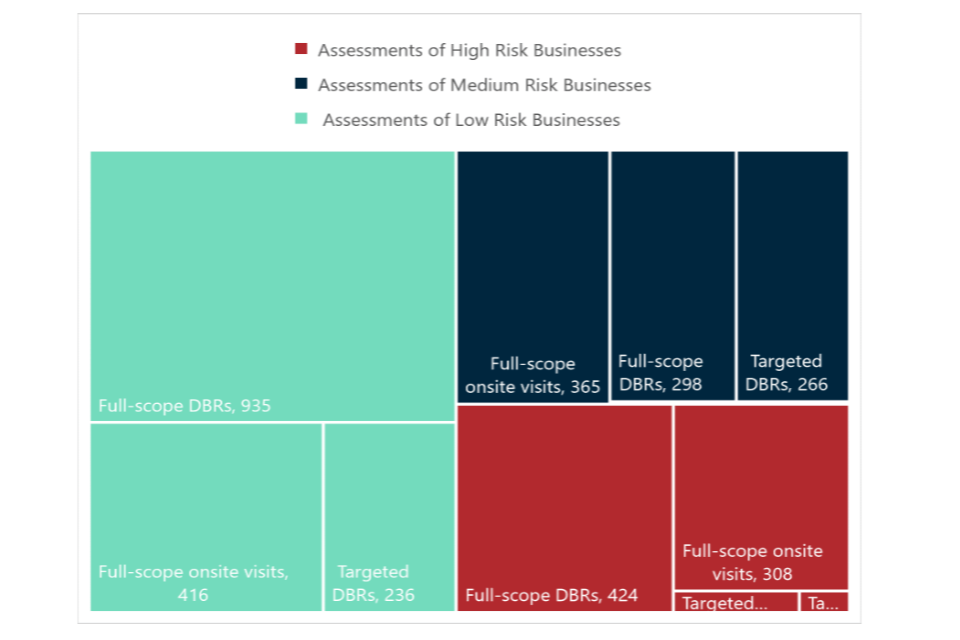

PBSs conducted a total of 2,656 DBRs (481 on high-risk businesses, 724 on medium-risk businesses and 1,451 low-risk businesses) and 1,557 onsite visits (462 on high-risk businesses, 515 on medium-risk businesses and 580 on low-risk businesses) during the 2023-24 reporting period, meaning that roughly 10% of their supervised population was subject to direct supervisory activity.

Table 3.H Accountancy PBS’ DBRs and onsite visits, split by risk

Table 3.H Accountancy PBS’ DBRs and onsite visits, split by risk

Source: HMT annual return from accountancy PBSs

Table 3.I Legal PBS’ DBRs and onsite visits, split by risk

Table 3.I Legal PBS’ DBRs and onsite visits, split by risk

Source: HMT annual return from legal PBSs

Across the reporting period, PBSs reported the most common breaches identified as:

-

Inadequate documented policies and procedures.

-

Inadequate CDD procedures.

-

Inadequate client risk assessment or records.

-

No or inadequate firm-wide risk assessment.

Many PBSs also noted that a lack of knowledge or understanding of the regulations was a common theme among firms with non-compliance or poor procedures. This was sometimes due to the size of the firm or their available resources. Often, this was linked to firms using templates or third-party policies without fully tailoring them to the individual firm.

In the 2023-24 reporting period, accountancy PBSs reported that 14% of the businesses on which they conducted onsite visits and DBRs were non-compliant with the MLRs. Legal PBSs reported that 20% of their assessments resulted in a non-compliant rating.

Other supervisory interventions

PBSs also assessed a total of 4,674 businesses via interventions other than DBRs or onsite visits, including:

-

Requiring supervised firms to complete an annual AML form, then providing bespoke support to firms where responses indicate a lack of understanding of the MLRs.

-

Thematic reviews on aspects of AML supervision such as BOOMs or Register of Overseas entities, leading to analysis of the regulated population.

-

Requiring firms to respond to questionnaires sent out by the supervisor.

-

Reviews of supervisory data held by PBSs to look for ‘red flags’ which may indicate poor compliance by one or more firms.

Some PBSs also undertook random dip-sampling of medium- and low-risk businesses; 558 businesses were randomly selected for a DBR or an onsite visit, with 4% of those found to require a higher risk categorisation and 13% found to be non-compliant.

Table 3.J Monitoring activity by PBSs

| 2021-22 | 2022-23 | 2023-24 | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Supervisors | Total DBRs | Total onsite | Compliant | Generally compliant | Non-compliant | Total DBRs | Total onsite | Compliant | Generally compliant | Non-compliant | Total DBRs | Total onsite | Compliant | Generally compliant | Non-compliant |

| ACCA | 299 | 0 | 0% | 91% | 9% | 326 | 12 | 5% | 88% | 7% | 285 | 34 | 1% | 92% | 7% |

| AIA | 18 | 0 | 0% | 89% | 11% | 36 | 1 | 3% | 95% | 3% | 35 | 8 | 0% | 85% | 7% |

| CIMA | 3 | 21 | 17% | 29% | 54% | 2 | 22 | 21% | 13% | 67% | 7 | 30 | 19% | 27% | 54% |

| CIOT | 49 | 0 | 49% | 27% | 24% | 29 | 3 | 16% | 66% | 19% | 39 | 1 | 20% | 55% | 25% |

| ATT | 24 | 0 | 63% | 17% | 21% | 32 | 1 | 21% | 70% | 9% | 29 | 0 | 7% | 52% | 41% |

| ICAEW | 568 | 424 | 15% | 70% | 14% | 450 | 676 | 14% | 70% | 16% | 669 | 664 | 12% | 56% | 16% |

| ICAI | 5 | 51 | 89% | 4% | 4% | 1 | 53 | 48% | 28% | 13% | 45 | 9 | 28% | 46% | 26% |

| ICAS | 40 | 30 | 34% | 46% | 20% | 31 | 56 | 45% | 45% | 10% | 55 | 41 | 61% | 24% | 15% |

| ICB | 32 | 113 | 30% | 0% | 70% | 75 | 63 | 10% | 8% | 82% | 599 | 9 | 3% | 0% | 4% |

| IFA | 173 | 0 | 16% | 47% | 38% | 155 | 1 | 17% | 58% | 25% | 121 | 2 | 19% | 52% | 29% |

| AAT | 125 | 109 | 70% | 17% | 14% | 150 | 106 | 63% | 16% | 21% | 282 | 137 | 2% | 74% | 21% |

| IAB | 36 | 255 | 30% | 44% | 26% | 24 | 176 | 41% | 47% | 10% | 0 | 156 | 58% | 40% | 3% |

| IPA | 38 | 12 | 84% | 16% | 0% | 57 | 31 | 67% | 33% | 0% | 17 | 13 | 73% | 13% | 13% |

| SRA | 132 | 164 | 16% | 37% | 9% | 96 | 151 | 27% | 47% | 27% | 358 | 335 | 16% | 41% | 17% |

| Law Society of Northern Ireland | 105 | 51 | 59% | 27% | 13% | 69 | 111 | 49% | 32% | 14% | 53 | 110 | 55% | 31% | 18% |

| Law Society of Scotland | 49 | 14 | 38% | 17% | 44% | 58 | 23 | 30% | 46% | 25% | 67 | 51 | 1% | 97% | 3% |

| CLC | 17 | 25 | 24% | 29% | 48% | 5 | 51 | 7% | 43% | 43% | 11 | 27 | 11% | 45% | 66% |

| BSB | 278 | 0 | 0% | 0% | 0% | 10 | 0 | 10% | 0% | 0% | 31 | 0 | 100% | 0% | 0% |

| General Council of the Bar Northern Ireland | 0 | 0 | 0 | 0 | 0 | 0 | |||||||||

| CILEx | 28 | 0 | 79% | 21% | 0% | 21 | 0 | 81% | 19% | 0% | 0 | 0 | |||

| Faculty of Advocates | 7 | 0 | 100% | 0% | 0% | 0 | 8 | 100% | 0% | 0% | 7 | 0 | 100% | 0% | 0% |

| Faculty Office of the Archbishop of Canterbury | 64 | 18 | 96% | 2% | 1% | 38 | 10 | 4% | 96% | 2% | 129 | 20 | 44% | 48% | 8% |

| Total PBSs | 2090 | 1287 | 1665 | 1555 | 2839 | 1647 | |||||||||

| Accountancy PBSs | 1410 | 1015 | 1368 | 1201 | 2183 | 1104 | |||||||||

| Legal PBSs | 680 | 272 | 297 | 354 | 656 | 543 |

Source: HMT annual return from PBSs (acronyms can be found in Table 2.J or Annex)[footnote 1]

Box 3.D Case study: monitoring activity by an accountancy PBS

-

An accountant for a club identified a decline in bar profits and a significant increase in profits from two gaming machines, raising suspicion of potential money laundering.

-

The accountant sought guidance from an accountancy PBS on whether to report the matter and continue acting for the client.

-

They were advised on their professional obligations under the MLRs to submit a Suspicious Activity Report (SAR).

-

The accountant was directed to resources from the accountancy PBS, as well as general AML guidance and NCA’s SAR portal to support their decision-making and reporting.

-

The firm’s SAR procedures and the quality of SARs submitted will now be reviewed by the accountancy PBS in a Practice Assurance Review.

Box 3.E Case study: monitoring activity by a legal PBS

-

A legal PBS’s Monitoring Officer found inadequate AML/CTF measures in a firm, with notable deficiencies in client due diligence and source of funds checks.

-

The PBS’s Professional Conduct Committee reviewed the inspection report and identified reliance on personal knowledge over proper documentation, directing a follow-up AML/CTF inspection.

-

The subsequent inspection noted significant improvements, including the implementation of an AML/CTF checklist for new and existing clients.

-

The Monitoring Officer’s review of 12 files during the follow-up inspection raised no AML/CTF queries.

-

The legal PBS recognised the firm’s progress and adherence to the AML/CTF regime, providing positive feedback to the firm.

4. Ensuring compliance

Compliance strategies and enforcement

The Money Laundering Regulations (MLRs) require supervisors to ensure that regulated firms which breach the regulations are subject to effective, proportionate, and dissuasive measures. This means that disciplinary measures should be effective at ensuring future compliance by sanctioned businesses, proportionate to the severity of the breach, and dissuasive of non-compliance by others.

Supervisors have a wide range of sanctioning powers available to them to achieve this, including:

-

Fines

-

Public censures

-

Suspension or cancellation of registration

-

Referral to law enforcement agencies and/or prosecutors

Several supervisors also derive broader sanctioning powers from pieces of legislation other than the MLRs (such as the Proceeds of Crime Act, the Financial Services and Markets Act, the Legal Services Act, and the Gambling Act, or through the By-Laws and Regulations of the Professional Body). Action taken under this separate legislation is only included in this section where these powers were used in response to money laundering breaches.

Direct comparisons between supervisors on levels of fines and numbers of cancellations/suspensions may not be appropriate due to the differing population sizes, risk categorisations of each supervisor’s population, and the differing contexts in which supervisors operate.

Summary of enforcement action across all supervisors

For the 2023/24 period, HM Treasury requested that supervisors provide enforcement data broken down by the assessed risk level of the business in terms of money laundering and terrorist financing. As discussed, this should allow for a fuller picture of how supervisors are targeting enforcement action.

The total sum of fines across all 25 supervisors in 2023-24 was £41.5m compared to £196.5m in 2022-23. It should be noted that significant year-on-year changes in this aggregate figure are common and driven largely by the outcomes of FCA enforcement action against large financial institutions, and should not be taken as representative of trends across all supervisors.

Across all supervisors, £14.5m of fines were issued to high-risk businesses, £26.5m of fines were issued to medium-risk businesses (this was driven by 3 large fines from the FCA), and £598,300 of fines to low-risk businesses. The average fine amount across all supervisors was approximately £34,000.

Given the heightened risk of money laundering associated with Trust and Company Service Providers (TCSPs), the supervisors overseeing these entities (predominantly HMRC and the PBSs) have separately reported enforcement actions taken against them for 2023-24. In total, fines amounting to £1.5m were imposed on TCSPs, and the memberships of 51 supervised businesses operating as TCSPs were revoked.

Excluding TCSPs, the memberships/registrations/authorisations of 27 high-risk businesses were cancelled, alongside seven medium-risk and 20 low-risk businesses.

As mentioned, all supervisors have a range of actions available from formal actions such as fines and suspension or cancellations of registrations, to informal actions like guidance or reminder letters.

Table 4.A All supervisors’ formal and informal actions, split by risk

Table 4.A All supervisors’ formal and informal actions, split by risk

Source: HMT annual return data

Across all 25 supervisors, 180 formal actions and 707 informal actions were taken against high risk businesses, 179 formal actions and 401 informal actions were taken against medium risk businesses, and 121 formal actions and 490 informal actions were taken against low risk businesses.

Under the MLRs, supervisors can publish information about enforcement actions publicly. In the 2023-24 reporting period, the 25 supervisors published a total of 1,015 of their enforcement actions online.

Table 4.B Enforcement actions by all supervisors

| 2021-22 | 2022-23 | 2023-24 | |

|---|---|---|---|