Best Practice Guide 23-24: Climate & Sustainability Reporting

Published 10 April 2025

© Crown copyright 2025

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/best-practice-examples-on-sustainability-reporting-from-2023-24/best-practice-guide-23-24-climate-sustainability-reporting

1. Introduction

Why Climate and Environmental Reporting is Important:

-

Government accountability for climate and environmental action.

-

Public interest and the need for transparency.

-

Demonstrating alignment with climate and environment targets (e.g., Greening Government Commitments (GGCs), Net Zero).

Focus of this Guide:

-

Provide real-world examples of good practices.

-

Highlight areas where reporting often falls short.

-

Offer actionable advice on improving reports.

Key Reporting Frameworks:

-

The Government Financial Reporting Manual (FReM) is central to government and UK public sector reporting.

-

Sustainability Reporting Guidance (SRG) encapsulates the GGCs, other climate and environmental objectives, and voluntary reporting.

-

The TCFD-aligned disclosure Application Guidance (herein ‘the Application Guidance’) for climate-related risks.

1.1 The right information, in the right place

The FReM1 sets out the considerations annual report preparers need to bear in mind when deciding whether and where to publish information on performance.

The Application Guidance grants flexibility in deciding where to report information, and in what level of detail. Signposting to external reports enables users to ‘drill down’ to complementary information on a particular component, but that is not necessary to effectively communicate the material or mandated information.

Principles for Effective Disclosure

The Task Force set out seven fundamental principles for effective disclosure, stating that disclosures should:

-

present relevant information

-

be specific and complete

-

be clear, balanced, and understandable

-

be consistent over time

-

be comparable among organisations within a sector, industry, or portfolio

-

be reliable, verifiable, and objective

-

be provided on a timely basis2

These principles are adopted in the Application Guidance and align with performance reporting principles set out in the FReM3.

Examples in this publication illustrate specific features of high-quality annual reports and accounts (ARAs). These may not be relevant for all organisations or situations. The inclusion of an example from an organisation does not evaluate the organisations’ overall ARA or Sustainability Report.

2. Opening Page and Providing the Context

A strong first page for sustainability reporting sets the tone, engages readers, builds trust, summarises key messages, and sets the benchmark for compliance with relevant frameworks, aligning the organisation’s mission with its sustainability goals.

This section evaluates examples of good practice for introductions and overviews for Sustainability Reports and TCFD Reports. Practices to avoid are also highlighted throughout this guide. These are general examples of practices to avoid and are not linked to the example being analysed.

Good Practice

-

Visuals and Accessibility: Use charts, graphs, and graphics which drive user engagement. Use clear, accessible language to ensure all stakeholders understand the message.

-

Explain Requirements: Identify and explain the relevant frameworks, statute and regulation - and how your organisation complies with them - to set a clear benchmark.

-

Provide Context: Convey and prioritise the important information on the organisation, its strategy, its group, and the industry it operates in with respect of sustainability to set the scene.

-

Keep It Concise: Include key information, findings and conclusions at the beginning of the report. Reserve specifics for later sections and use the first page to provide a concise overview. Cross-reference within the ARA, and signpost to other sources.

Practice to Avoid

-

Vague Statements: Avoid broad, generic statements. Instead, provide specific examples of sustainability goals, progress, and achievements.

-

Balanced Introductions: Avoid making exaggerated claims or unrealistic projections about sustainability efforts. This can damage credibility. Acknowledge the challenges, balancing these by highlighting solutions or plans for improvement.

-

Detailed and Technical Information: Avoid overwhelming users with too much detail. Unnecessary technical jargon on the first page can confuse the reader. Instead, build up to more complex disclosures later in the section.

Proving Context and Setting out the Big Picture

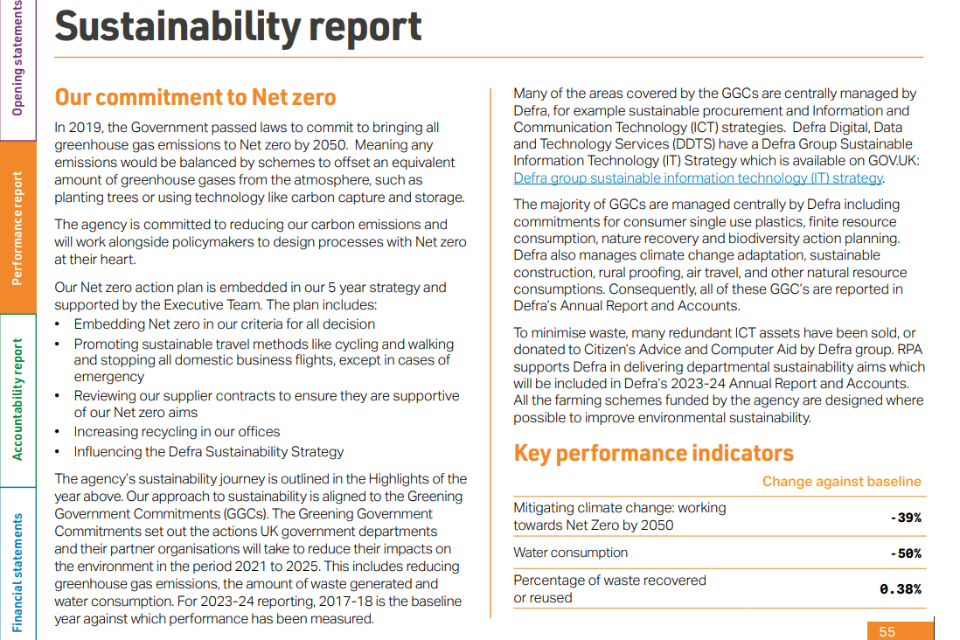

Rural Payments Agency (RPA), 2023-24

Good Practice:

The first page of RPA’s 2023-24 sustainability report sets a positive tone by highlighting key achievements and the agency’s commitment to sustainability. It presents a narrative that outlines the objectives achieved over the past year, particularly focusing on areas such as reducing environmental impacts, improving engagement, and embracing innovative digital services.

Why It’s Good Practice:

The first page of RPA’s Sustainability Report:

-

reaffirms the government’s statutory and the agency’s own commitment to net zero.

-

links to the Net Zero Action Plan, aligned with the 5-year strategy, highlighting measurable outcomes to ensure transparency. The reference to the year’s highlights reinforces this.

-

sets out the responsibilities and accountability between them and the environment – signposting to relevant supplementary material (e.g., Defra’s Group Sustainable Information Technology Strategy).

-

highlights the Key Performance Indicators (KPIs) to emphasise their significance and provide an overview.

Navigation bars allow users to traverse the ARAs efficiently.

Prioritising key information to communicate to users on the first page, sets the scene and conveys management’s own assessment of what is important (e.g. governments’ statutory net zero commitment, sustainability plan overview, highlighting the most important KPIs).

Practice to Avoid: Weak introductions Failing to set the scene or provide context - either on the reporting framework or on the impacts of climate and environment on the organisation.

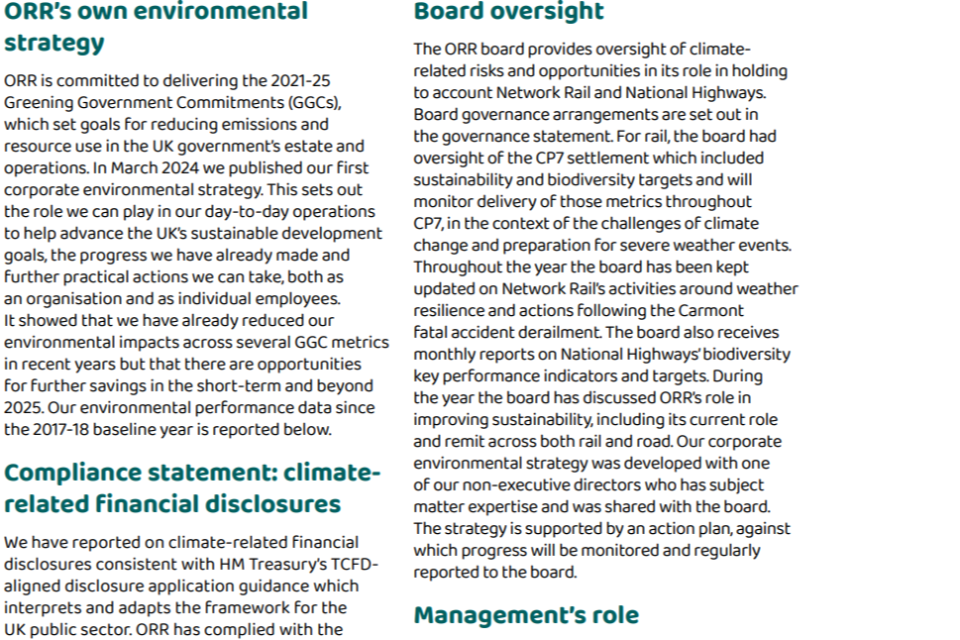

The Office of Rail and Road (ORR), 2023-24

Good Practice:

As a regulator, ORR uses an opening paragraph to set out their oversight role for rail and road - explaining that both industries are subject to different goals and legislation. The GGCs are identified as the relevant reporting framework.

ORR details interactions with key stakeholders used to understand the related risks facing the industry, and potential mitigation strategies - leveraging off existing reporting frameworks (i.e., Defra’s National Adaption Plan).

Why It’s Good Practice:

ORR provides context (i.e., regulatory, reporting framework) which sets a clear benchmark for users to understand and assess the organisation. The first page identifies the most important information for users to understand the big picture in a clear and succinct way.

Stand-out opening statements can be used to present management’s view on the impact of sustainability on the organisation to set the scene.

Regulators are responsible for influencing external stakeholders. Considering the climate-related risks faced by the related industry is key to understanding the regulator’s own risk management and future strategy.

Using limited text, varied font sizes, and images creates a more welcoming first page.

Practice to Avoid: Unvaried and text heavy first pages These can reduce user engagement and make it more challenging to understand the big picture.

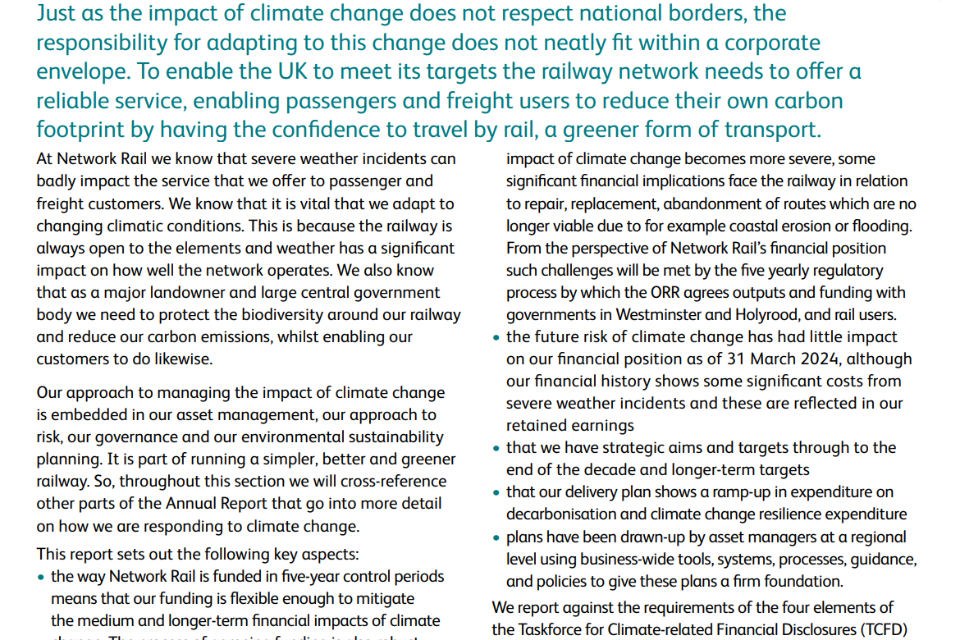

Network Rail, 2023-24

Good Practice:

Network Rail:

-

highlights the key physical climate risks and transitional opportunities – severe weather and greener transport – for their organisation and its strategy.

-

identifies and prioritises the key areas impacted by climate change to convey to users - physical asset management and environmental planning.

-

uses a short stand-out opening paragraph to set the scene and management’s own assessment of the impact of climate on rail.

Why It’s Good Practice:

Network Rail’s first page uses a variety of formats to make certain information stand out, uses cross references to underlying information, and prioritises key information to highlight to users.

Using the first page to summarise information covered later – either in an overview or TCFD Compliance Statement - introduces the later disclosures, preparing the reader for upcoming more detailed or technical content. A summary with cross references can be used as an anchor to navigate to other disclosures.

The First Page of TCFD Report with a Climate context

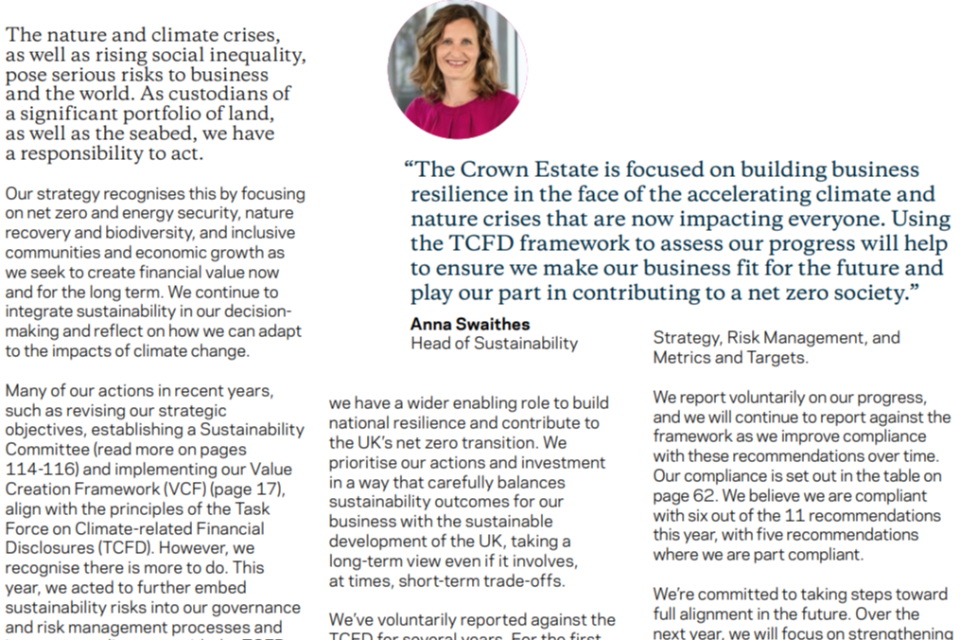

The Crown Estate, 2023-24

The Crown Estate is set up as independent commercial business by an act of parliament

Good Practice:

The first page of the Crown Estate’s TCFD Report explains the nature and climate risk for the organisation; provides details on compliance, and non-compliance, explains future disclosure plans; and communicates the four key implementation actions.

Communicating summary or compliance information against the full list of recommended disclosures demonstrates progress.

Stand-out opening statement from those charged with governance for climate or sustainability topics are an effective way to communicate the responsible owners’ views to users.

Why It’s Good Practice:

The Crown Estate’s TCFD Report starts with the most significant information, providing users with context. The first page is concise, prioritising key information (i.e., management’s own view, key actions). The TCFD Compliance Summary supports users to understand the big picture and to navigate.

Using Compliance Summaries and Statements

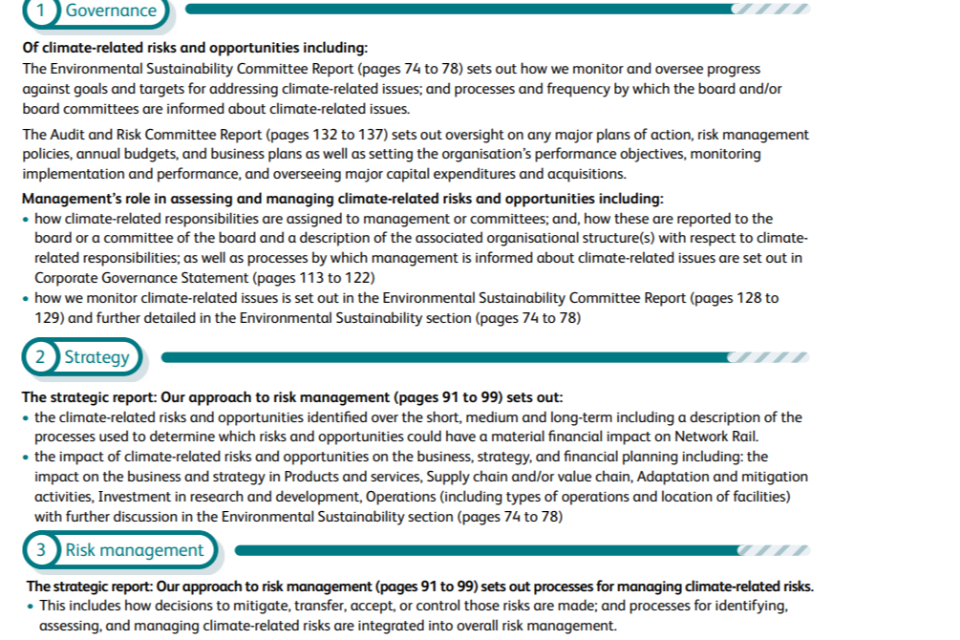

Network Rail, 2023-24

Good Practice:

Network Rail sets out the TCFD pillars, and how each of the recommended disclosures apply to the organisation towards the start of their TCFD Report – using page references to link to supporting detail.

Why It’s Good Practice:

Network Rail’s TCFD Compliance Summary includes high-level information on the recommendations and recommended disclosure, accurately reflecting compliance and future plans.

High-level summaries of how the recommended TCFD disclosures across the four pillars have been met, with cross-references to supporting detail across the ARA support user understandability and identify areas for deeper analysis.

Including these summaries towards the start of section provides an anchor and improves users’ ability to navigate the report.

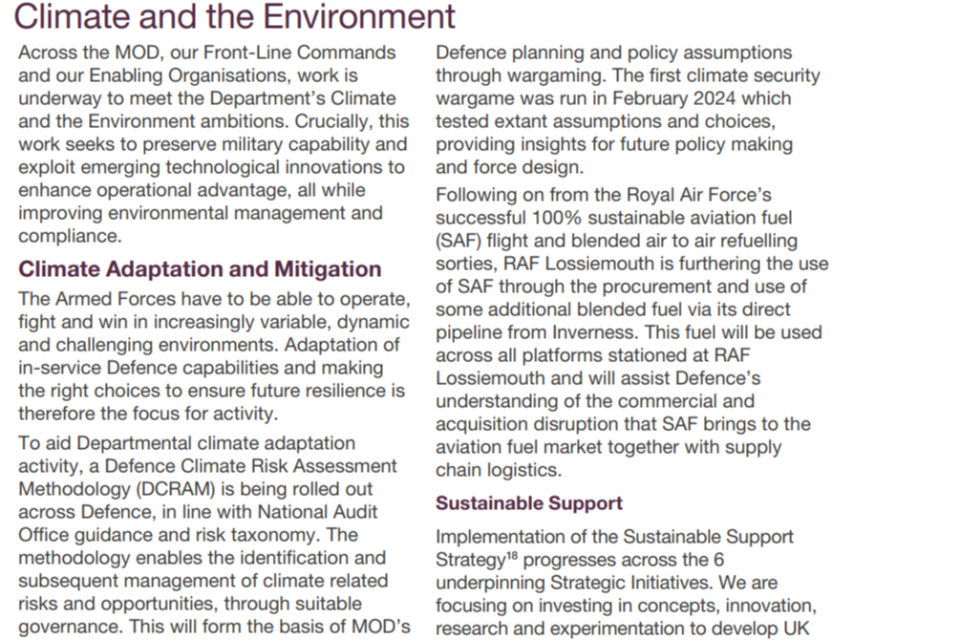

Ministry of Defence (MOD), 2023-24

Good Practice:

The first page of MOD’s sustainability report provides an effective introduction, setting out how climate and the environment are seen in the context of the department, its responsibilities and its operations. The report leads with impactful policies and programmes.

Effective overview of the foundation on which the department is conducting its analysis, and how this links to TCFD.

Longer-term evaluation of continued service delivery and the key drivers impacted by climate risks, and what the department is doing in response. MOD details the key actions and relevant case studies in an effective manner.

Case studies provide more context for user - in this case, the RAF trailing sustainable aviation fuel.

Why It’s Good Practice:

The first page of MOD’s Climate and Environment Report includes information for users to understand the level of compliance, future plans for implementation, and key actions undertaken. MOD conveys the most important information to primary users – to convey management’s view of climate-related issues for the department. They also set out the scope and lens of the disclosures.

Thorough and practical climate risk management can be achieved by embedding climate environmental risks within broader governance and decision-making frameworks, as well as aligning them with the organisation’s long-term objectives.

Practice to Avoid:

-

Boiler Plate TCFD Compliance Statements Weaker statements copied the Application Guidance example – failing to explain any judgement made - or set out plans for related reporting in future periods.

-

Failure to explain new disclosures Some reports failed to explain the adoption of TCFD by central government.

Setting out the Reporting Approach

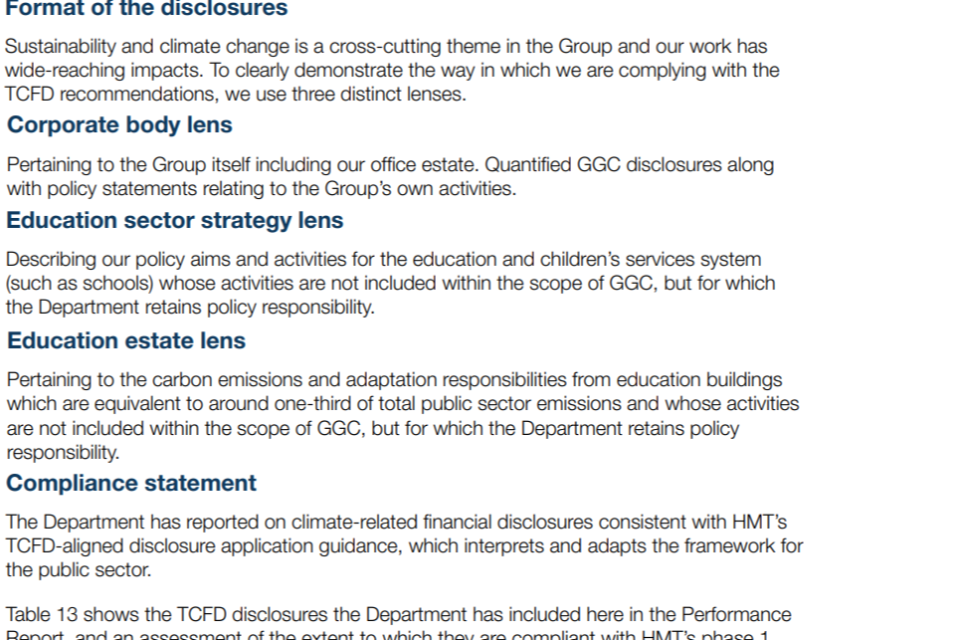

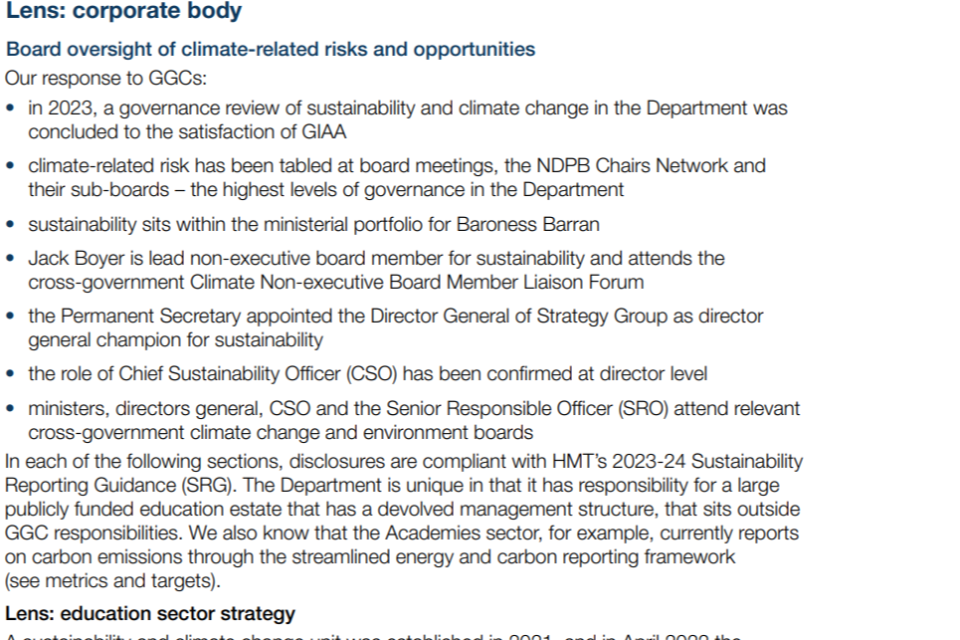

The Department for Education (DfE), 2023-24

Good Practice:

DfE analyses climate and sustainability across three distinct lenses (corporate body, education sector strategy, educational estate). In line with performance reporting principles, the department recognises the areas where it has broader responsibilities outside of its operational boundaries – noting what is covered by existing GGC reporting framework.

Why It’s Good Practice:

DfE considers the wider implications of climate and sustainability across the organisation and its strategy. The different lenses where they held different authority and responsibilities. The rest of the report split analysis and disclosures across each of these different lenses.

Throughout the TCFD Report, DfE explains their coordinated response on sustainability and carbon reduction -across their organisation, the wider departmental group and the sector.

The UK public sector comprises a variety of organisations. Each department or public body can tailor their risk management and reporting strategies to their unique context - considering factors like operational boundaries and wider responsibilities (e.g., policy setting role, funding) supports users to understand the full context of sustainability-related disclosures.

Practice to Avoid: Failure to consider wider authority or responsibility

Some reports failed to consider the wider implications of climate on their organisation – applying narrow operational boundaries and only considering limited scopes.

TCFD Implementation Progress

Transport for London (TfL), 2023-24

Good Practice:

TfL’s commitment to transparency is evident in their detailed disclosures, which provide stakeholders with the information needed to assess the organisation’s climate-related financial risks and opportunities. This openness helps build trust and credibility with readers.

Why It’s Good Practice:

TfL’s TCFD Report includes case studies and real-world examples of how they are implementing TCFD recommendations. These practical illustrations help readers understand the tangible actions TfL is taking and the outcomes of these initiatives.

Connecting TCFD’s four pillars to the organisation and its actions supports users to understand performance.

Quantitative impact information provides context.

3. Governance and Accountability

Good governance is fundamental to managing sustainability-related issues. The TCFD framework sets new disclosure requirements concerning the governance of climate issues.

This section evaluates examples of good practice for TCFD Governance recommended disclosures a) Board’s Oversight and b) Management’s Role. This also highlights practice to avoid.

Organisations that manage climate, alongside other environmental or sustainability-related issues, often choose to address these topics collectively and effectively utilise existing reporting requirements (e.g., in the Corporate Governance Report) to efficiently meet particular TCFD disclosure requirements.

Good Practice

-

Use Organograms: Visually setting out accountability and climate (and other) risk management structures, makes it easier for users to understand who is responsible for oversight and decision-making on climate governance.

-

Provide Context: Include a clear strategy, outlining your goals and objectives, and how you’ll meet them. Explain significant factors that have influenced performance.

-

Be Organisation Specific: Conveying important information on governance arrangements with external stakeholders, and across the groups or industry. Be clear on responsibility and ownership.

-

Stakeholder Engagement: Highlight partnerships and collaborations advancing environmental objectives.

Practice to Avoid

-

Lack of Clarity: Be specific on the individuals, committees or groups responsible for climate governance. Be clear on reporting channels (i.e., frequency, focus).

-

Avoid Duplication: Existing information in the Corporate Governance Report, Performance Report and Accountability Report should be cross referenced, where possible.

3.1 Governance recommendation

TCFD recommendation for Governance: Disclose the organisation’s governance around climate-related issues.

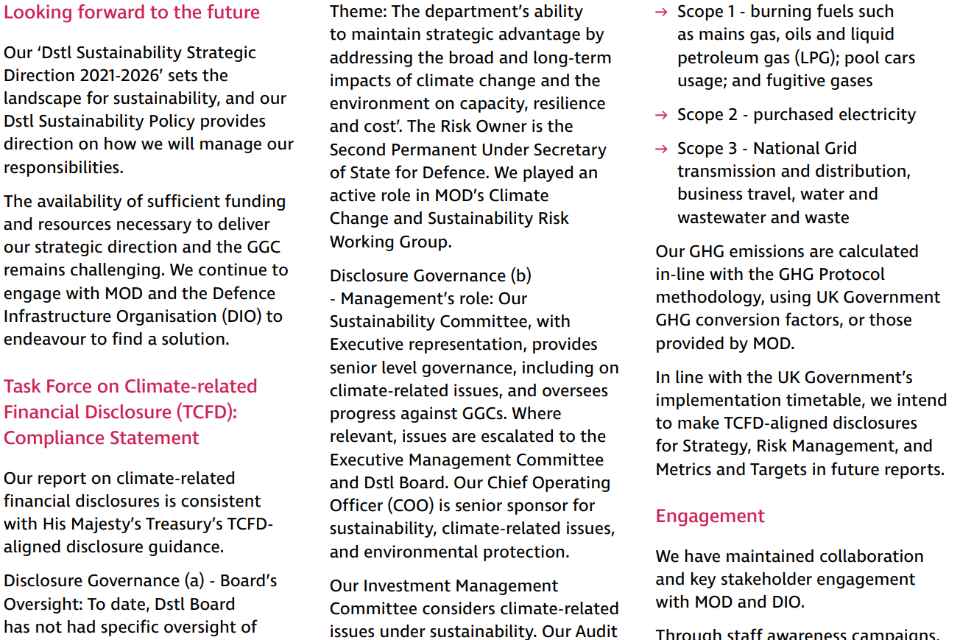

Defence Science and Technology Laboratory (Dstl), 2023-24

Good Practice:

Dstl explains how climate is incorporated into governance processes - however, they are clear and transparent that the Board has not had specific oversight of climate-related issues in the period – relevant to Governance recommended disclosure a).

Why It’s Good Practice:

Dstl’s disclosure is open and honest on activities undertaken and progress to date – setting out plans for further reporting periods.

Dstl explains how they contribute to the departmental group’s response on climate-related issues and are specific on the groups involved.

Considering relationships across the departmental group or sector supports a more complete response to the wider impacts of climate change on the organisation – both direct and indirect.

Practice to Avoid: Lack of openness on implementation progress reports that directly use TCFD’s recommendations and recommended disclosures to set minimum implementation steps – rather than assessing the action undertaken, and what is still needed.

TCFD recommendation for Governance: Disclose the organisation’s governance around climate-related issues.

The Office of Rail and Road (ORR), 2023-24

Good Practice:

ORR’s TCFD section sets out governance structures and lines of responsibility – Specifically on how climate considerations are integrated into board-level decisions and organisational risk management processes. They report assigned climate-related responsibilities for positions and committees, as well as the process and frequency of reporting to the Board.

The ORR effectively sets the scene and identifies relevant climate and environmental frameworks, such as the GGCs.

The TCFD Compliance Statement identifies the relevant guidance applied, the level of compliance, and plans for future disclosure.

ORR also highlight the development of their environmental strategy, supported by a non-executive director with relevant experience, showcasing Board commitment.

Why It’s Good Practice:

ORR has chosen to explain governance of climate-related issues for rail and highways separately supporting users to understand the differences. They detail how the board oversees climate-related risks, ensuring they are managed alongside other significant risks, such as operational and financial concerns. Senior management is actively involved in managing climate-related risks, ensuring that their approach is aligned with the organisation’s strategic objectives.

Standout sections titles make the report easier to read and navigate.

Clear identification of roles and responsibilities for the climate risks identified.

Practice to Avoid: Failing to assess climate’s significance within existing risk management processes.

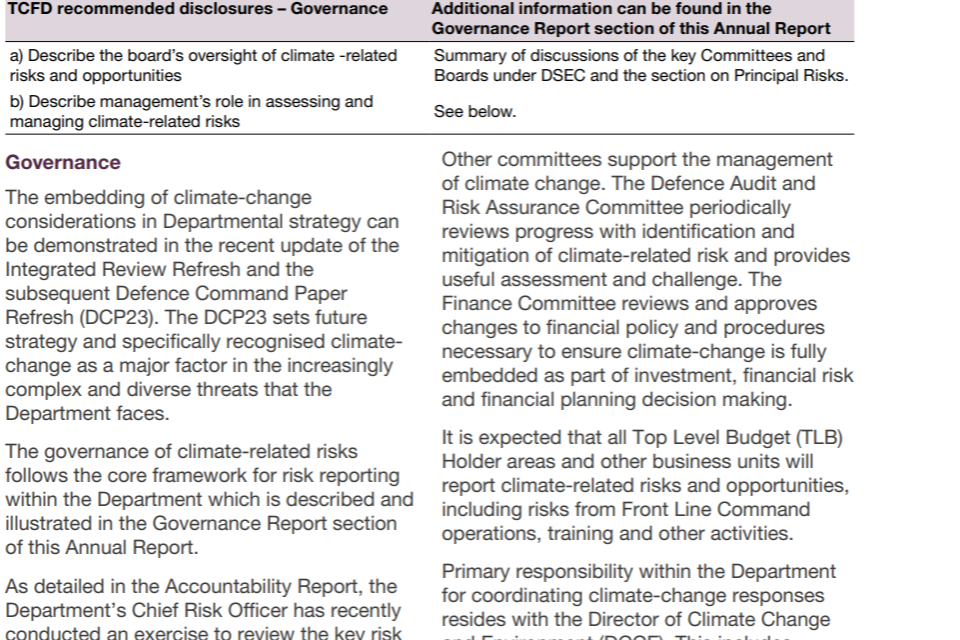

Ministry of Defence (MOD), 2023-24

Good Practice:

MOD’s Governance a) and b) recommended disclosures set out the clear lines of accountability and responsibility for climate and the environment within their leadership structure – outlining who is responsible for implementing climate strategies.

Why It’s Good Practice:

By clearly outline roles and responsibilities, as well as linking committees to information in the Corporate Governance Report - MOD provides a detailed consistent picture for Governance.

Clearly defined roles and responsibilities over climate and environmental strategies and risks ensure accountability and leadership buy-in.

Practice to Avoid: Vague statements about leadership commitments without specifying who is responsible or outlining the role of the board in sustainability governance.

3.2 Governance a) Board’s Oversight

TCFD recommended disclosure for Governance a): Describe the board’s oversight of climate-related issues.

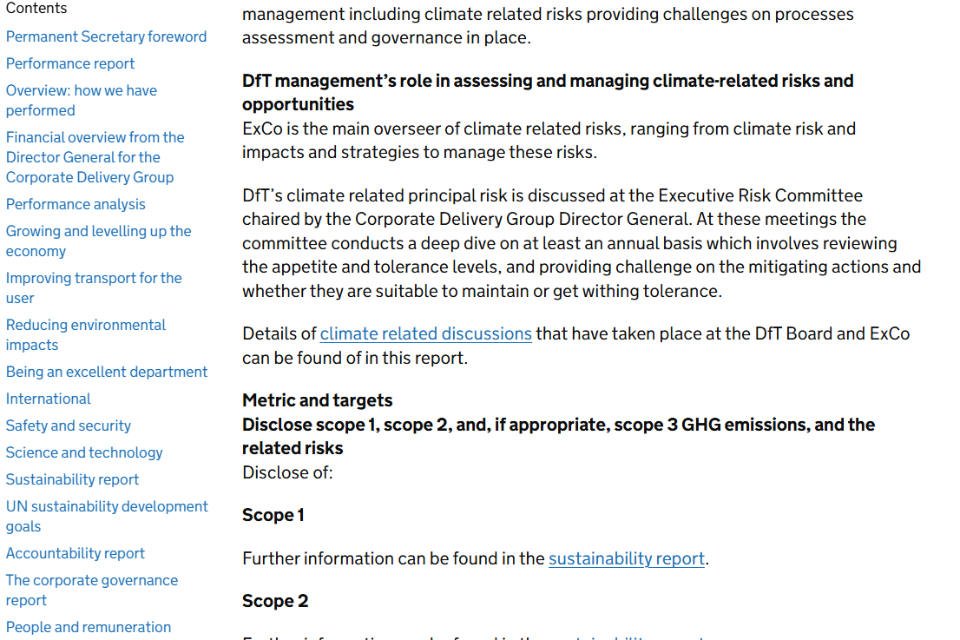

The Department for Transport (DfT), 2023-24

Good Practice:

The TCFD section of DfT’s ARA cross-references to a list of 2023-24 Board and Executive Committee discussions in the Corporate Governance Report.

Why It’s Good Practice: DfTs disclosures provided details on the process and frequency of reporting. They explained how climate-related risks:

-

are incorporated into the organisation’s governance framework - cross-referencing to the Governance Report, where appropriate.

-

influenced corporate strategy, risk management, and decision-making processes.

In addition to listing the climate-related topics discussed – this demonstrates that climate is integrated in the department’s risk management processes and how it managed and viewed alongside other risks.

Reporting climate risks alongside other risks in the ARA can drive linkage and support proportionate and integrated disclosure.

Practice to Avoid: Disproportionate information on climate being reported. Where governance of climate risks is managed alongside other risks - reporting similar information within the corporate governance report, and cross-referencing as appropriate is sufficient.

3.3 Governance b) Management’s Role

TCFD recommended disclosure for Governance b) Describe management’s role in assessing and managing climate-related issues

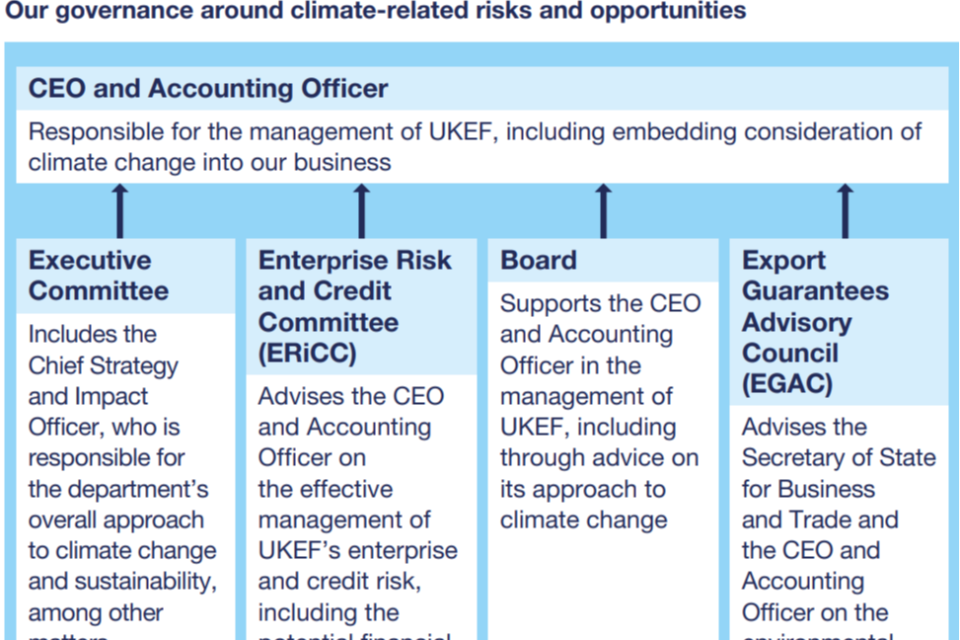

UK Export Finance (UKEF), 2023-24

Good Practice:

UKEF’s report sets out their governance, accountability and responsibility for climate-related risks to specific roles and various subcommittees.

Why It’s Good Practice:

The organogram clearly set out how responsibilities are assigned to positions and committees, as well as the process and frequency of reporting to the Board. They cross-reference to connected information in the Corporate Governance Report.

Organograms can be used to visually represent leadership/management structures, and enhance transparency by clearly outlining roles, responsibilities, and the chain of command - helping users to quickly grasp who holds authority and accountability for different climate-related issues.

4. Risk Reporting and Risk Management

While TCFD’s Risk Management recommended disclosures are not mandatory in central government ARAs until 2024-25, there are existing disclosure requirements for principal risks in the Performance Report. This guide analyses disclosures where climate was deemed a principal risk to identify good practice.

This section of the guide also draws from climate change adaptation reporting under the GGCs.

Good practices provide transparency and show that climate risks are managed proactively, while bad practices indicate a lack of integration and insufficient consideration of climate risks in decision-making.

Good Practice

-

Use Existing Frameworks: Leverage from existing climate risk frameworks to support disclosures (e.g., National Adaption Programme).

-

Use Signposting: Link to external publications and data sources for complementary information.

-

Integrated Disclosures: Where climate is managed in a similar way to other organisational risks, provide general information in the general risk section and cross reference. Include key details for climate risk management in the TCFD Report.

-

Terminology: Where possible, use consistent terminology and concepts to the Orange Book to support user understandability.

Practice to Avoid

-

Disproportionate Focus: Beyond the minimum disclosure requirements, information on climate should be proportionate to the organisation’s own assessment, considering other risks faced.

-

Isolated Risk Management: Avoid presenting climate risks separately without showing how they are integrated into the overall risk management frameworks. Cross reference, where appropriate (e.g., Corporate Governance Report)

-

Vague Risk Identification: Failing to specify key climate risks, or providing overly general statements without concrete examples or evidence

4.1 Climate and Environmental Risks and their Management

FReM requirement: Summarise principal risks faced, how these have affected the delivery of priority outcomes/strategic objectives, how they have changed and how they have been mitigated.

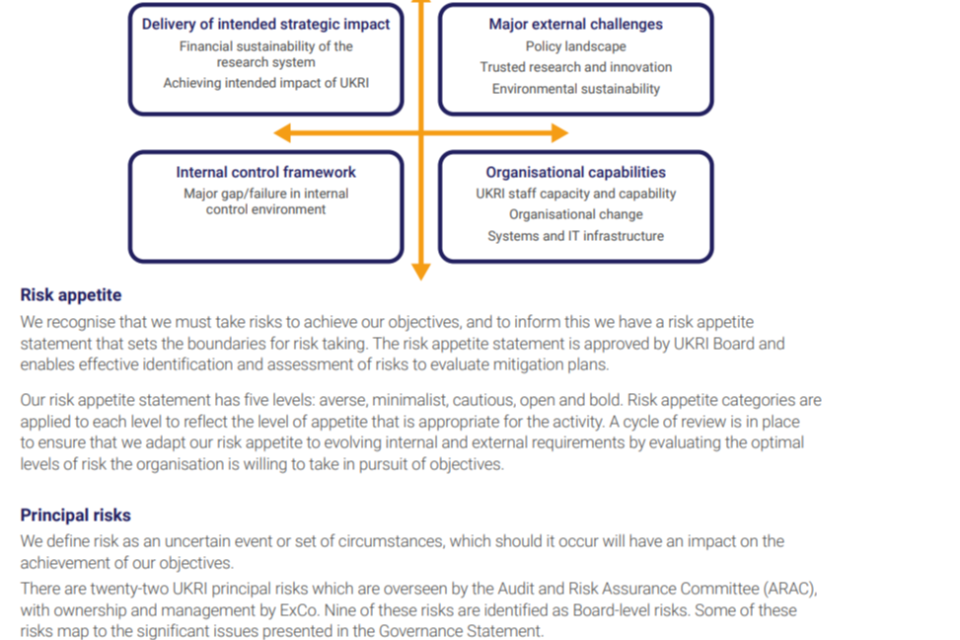

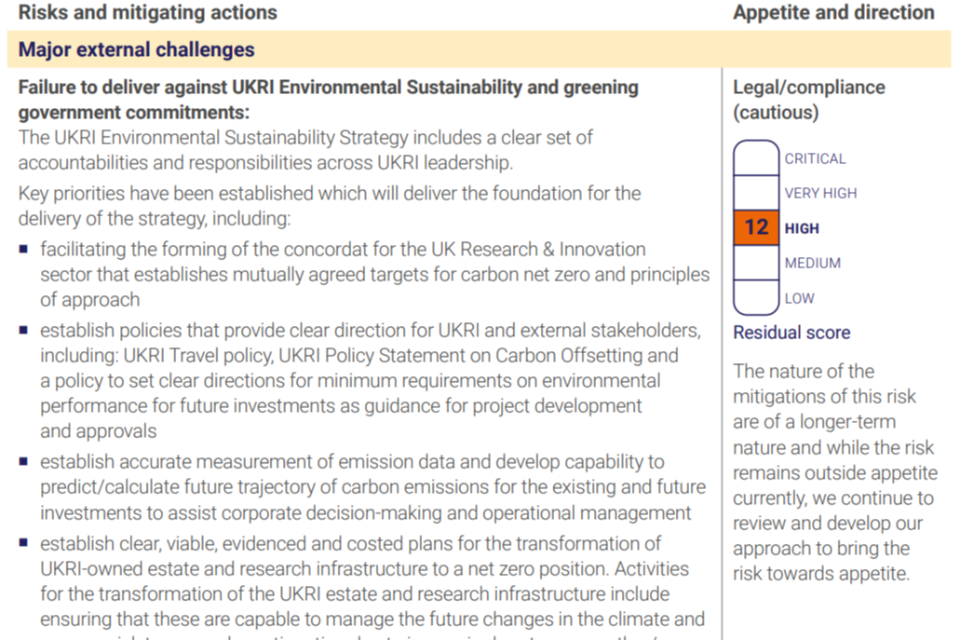

UK Research and Innovation (UKRI), 2023-24

Good Practice:

UKRI identifies climate as a principal risk in its TCFD Compliance Statement, with supporting risk information included in the Performance Analysis alongside other principal risks.

Why It’s Good Practice:

UKRI explain the different priority categorises for risks, and how they were managed by different levels of the organisation. Terminology is consistent with the Orange Book.

Use information from the Performance Analysis to meet Risk Management recommended disclosures with cross references to avoid duplication (i.e., risk appetite and management practices).

SRG requirement: Reporting entities must provide a summary of how they are developing and implementing a Climate Change Adaptation Strategy.

The Department for Transport (DfT), 2023-24

Good Practice:

DfT effectively addresses climate adaptation in its 2023-24 ARA. It includes detailed reporting on climate risks associated with infrastructure projects, including projected climate impacts and adaptation strategies and measures to ensure resilience in the UK’s transport infrastructure.

Why It’s Good Practice:

DfT integrates climate adaptation within broader organisational objectives, providing transparency about future risks, and detailing steps to mitigate impacts. This comprehensive approach represents best practice because it demonstrates both foresight and accountability. DfT makes use of signposts to supplementary information reported separately for users wanting more detail.

Actionable plans detailing steps taken to adapt to climate impacts, such as infrastructure resilience or policy changes.

Strategic integration connecting climate adaptation efforts to broader organisational goals and policies.

Signposting to external data, information and reports can support users seeking additional detail beyond the material information reported in the ARA.

5. Emissions Reporting

The GGC framework incorporates Scope4 1, Scope 2 and Scope 3 (Business Travel) emissions at a national level.

Organisations control and influence a much broader set of emissions. Better reporting entities considered their wider carbon footprint. This often extends beyond organisational and national boundaries and may require organisations to consider broader policy on driving sustainability performance and decarbonisation.

TCFD requires organisations to consider their Scope 1, Scope 2, and, if appropriate, Scope 3 GHG emissions, and the related risks.

Good Practice

-

Consider Scope 3: While reporting Scope 3 emissions categories beyond business travel remains voluntary, supply chain emissions and procurement considerations can drive progress.

-

Clear Methodology: Provide detailed explanations of the methodologies used for emissions calculations, including sources, assumptions, and any estimation methods. This helps stakeholders understand the data’s reliability.

-

Setting and Tracking Emission Reduction Targets: Be specific, measurable, achievable, relevant, and time-bound (SMART).

-

Historical Data and Trends: Offer year-on-year emissions data to show trends over time, as well as performance against targets.

Practice to Avoid

-

Unsubstantiated Net Zero Commitments: Individual entity-level Net Zero commitments should only be included where they are explained, with appropriate plans for delivery.

-

Cherry-Picking: Selectively reporting emissions that paint the organisation in a positive light - without considering materiality and poor performance.

-

Neglecting Emissions in Procurement: Some reports ignore the environmental impact of procurement and supply chains. Reporting on sustainable procurement is essential for a complete understanding of environmental performance.

5.1 Assessing your Carbon Footprint

TCFD and SRG requirements: Disclose Scope 1, Scope 2, and, if appropriate, Scope 3 GHG emissions, and the related risks.

The SRG sets out the minimum emissions reporting requirements for all central government bodies - which align with the GGCs. In addition, the SRG sets out guidance on the GHG Protocol methodology.

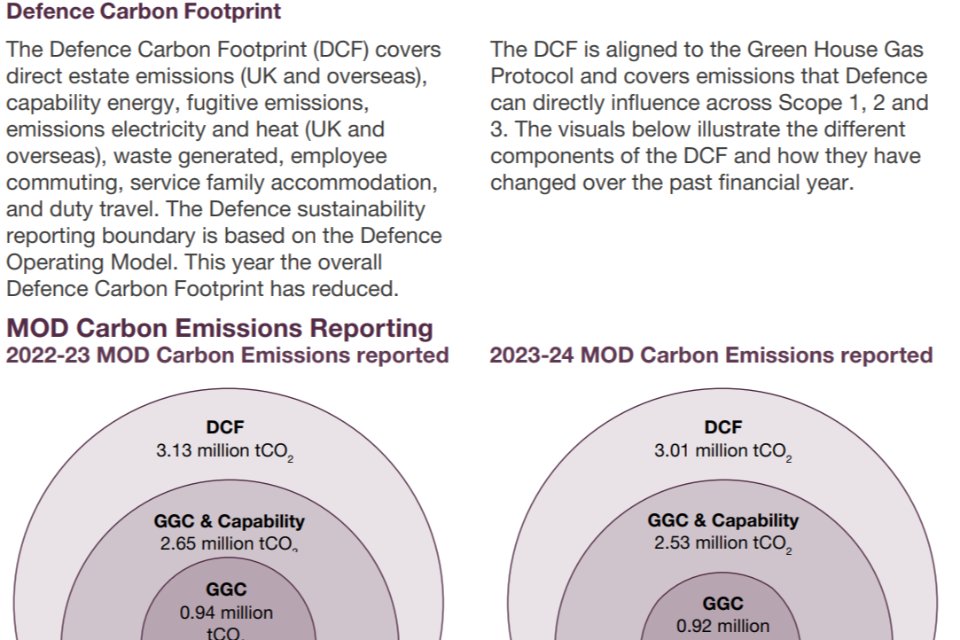

Ministry of Defence (MOD), 2023-24

Good Practice:

MOD gives an insightful overview of its carbon footprint, including various additional Scope 3 categories which it can directly influence. The department identified the GHG Protocol as the underlying methodology for wider emissions.

Why It’s Good Practice:

MOD explained the emissions scopes reported, including Scope 1, Scope 2 and Scope 3 business travel as a minimum under the GGCs and considered the department’s wider impact and other emissions they can influence. MOD quantified these wider emissions (not captured by the GGCs) including further Scope 3 categories, overseas emissions or those across their wider group.

Consistent charts across periods MOD has used pie charts in current and prior years allowing users to easily track and assess progress.

Providing users with further emissions information can provide more context for the organisation’s overall impact. This is particularly helpful where an entity’s emissions profile varies significantly from that covered by the GGCs.

Using a variety of charts and graphs to convey different sets of information can support user understanding.

5.2 Delivering Net Zero and Understanding Scope 3 Emissions

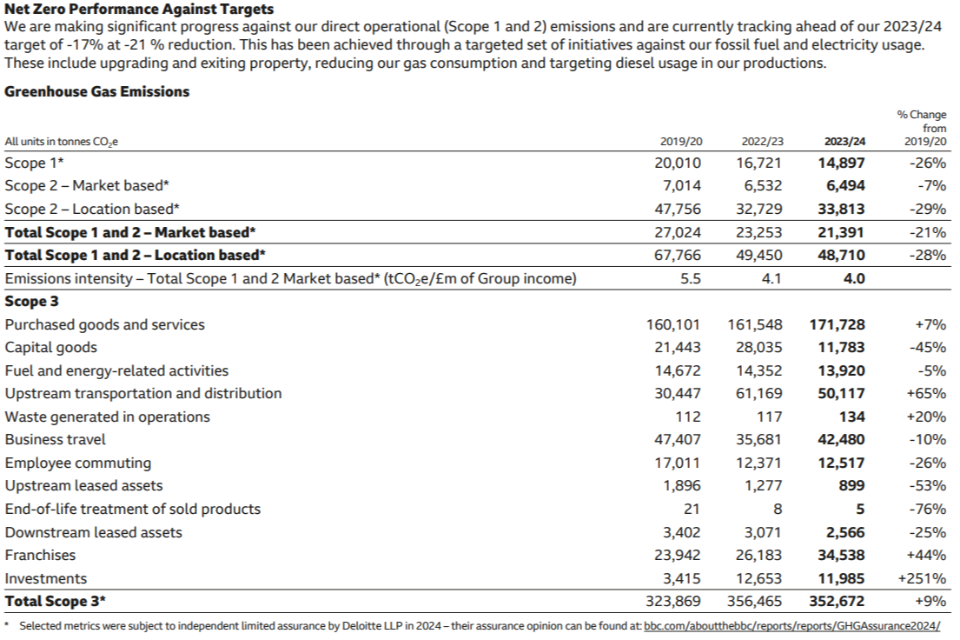

BBC, 2023-24

Good Practice:

The BBC has set a 2030 net zero target, which is approved by the Science Based Targets initiative (SBTi). It includes a summary table with operational (Scope 1 and 2) and value chain (Scope 3) emissions. This allows users to efficiently check overall progress. A further breakdown of emissions by scope and category is provided separately to show the underlying drivers. Total by emissions scopes can be reconciled between the two tables.

Why It’s Good Practice:

The BBC sets out a clear transition plan, alongside their emissions (including further Scope 3 categories). This explains progress to date and highlights the organisation’s commitment to achieving net zero.

Where organisations have set their own near-term net zero (or similar) targets – an explanation of what this means (i.e., baselines), how it is being achieved (i.e., transition plans), and progress so far is important to allow users to assess performance.

Explaining which metrics have undergone external assurance adds credibility to the reported figures and reinforces management’s commitment to achieving net zero goals.

Practice to Avoid: Unsubstantiated net zero commitments should not be included in ARAs.

5.3 Metrics & Targets b) Emissions

TCFD requirement: Disclose Scope 1, Scope 2, and, if appropriate, Scope 3 GHG emissions, and the related risks

Met Office, 2023-24

Good Practice:

The Met Office:

-

clearly set out how emissions metrics and targets, have been set and measured throughout the period including their initial stocktake to calculate their baseline (and in year re-baselining), the methodology used (i.e., GHG Protocol), and the metrics and targets selected to drive key change.

-

considers emissions from other specific KPIs (i.e., supplier engagement scores) with an accompanying fair and balanced assessment of supplier performance with both successes and ongoing challenges.

Why It’s Good Practice:

The Met Office explains their Carbon Neutral commitments appropriately in their ARA. They include

organisation-specific metrics and targets, beyond headline ‘net zero’ statements and emissions targets. They also include linkage between organisations’ climate-related metrics and targets and the risks and opportunities to which they relate to (e.g., KPIs from questionnaires to monitoring progress with suppliers).

Where organisations have set their own net zero (or carbon neutral) targets – an explanation of what this means (i.e., baselines), how they plan to achieve it (i.e., transition plans), and progress so far; is important to allow users to assess performance.

6. Metrics and Targets

Accurate and transparent reporting of climate and environmental metrics and targets is essential for accountability and demonstrating central government’s commitment to sustainability.

By setting clear, measurable targets and consistently reporting on key metrics, government bodies enhance transparency and drive performance improvements.

This section outlines key principles for reporting robust, meaningful metrics and targets in central government annual reports. The examples draw from both reporting against the GGCs, and more advanced forward-looking decarbonisation targets.

Good Practice

-

Forward Looking: Where future targets, goals and commitments have been set, appropriate interim targets should also be included with performance tracked. Where appropriate, include trajectory lines continuing until the end commitment or goal completion date.

-

Charts, Graphs and Tables: Consider which visual representation best conveys the data’s intended message. Include historic, baseline and target information.

-

Accompanying Narrative: Explain sustainability performance comparing to prior periods and targets. Link these to actions undertaken.

Practice to Avoid

-

Overly Positive Commentary: Some reports failed to identify where current performance was not on track, or where goals were unlikely to be met in future periods.

-

Inconsistent Reporting Across Years: Inconsistent year-on-year reporting makes it difficult for stakeholders to track progress. Organisations should use consistent frameworks and data collection methods each year to ensure comparability.

6.1 Forward Looking Information

TCFD requirement: Describe the targets used by the organisation to manage climate-related risks and opportunities and performance against targets

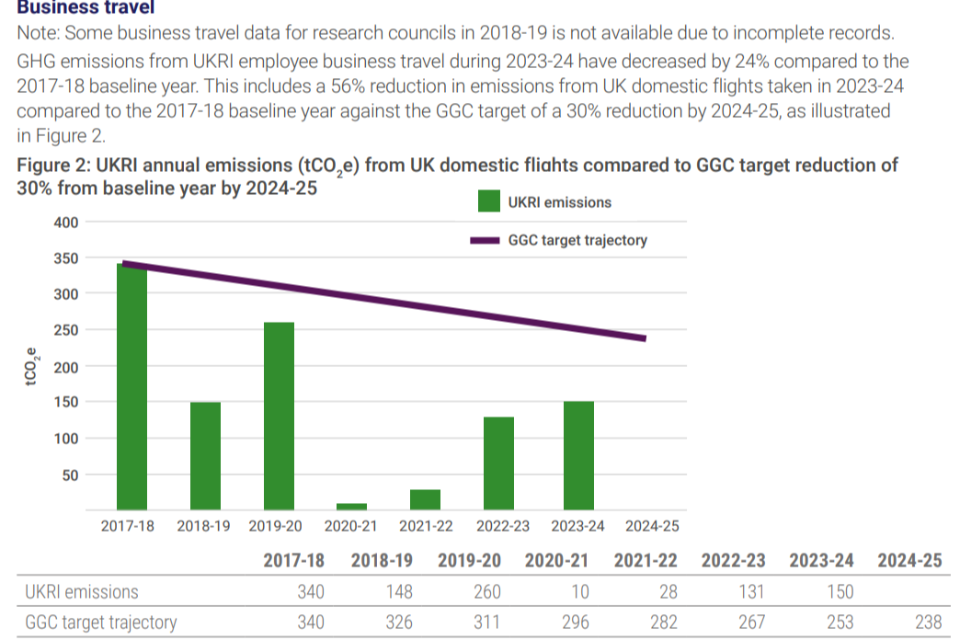

UK Research and Innovation (UKRI), 2023-24

Good Practice:

UKRI includes forward-looking trend lines to the end of the GGC commitment period for users to easily assess performance against the target and the likelihood of meeting the target.

Why It’s Good Practice:

UKRI’s GGC charts and graphs clearly demonstrated performance against target during the current and past periods, with trajectory lines continuing until the end commitment or goal completion date. Where performance was behind target this was clearly identified in the narrative and explained. Better reports fairly assess the likelihood of meeting the goal or commitment – based on current performance and trajectories.

Including a line for target trajectories on graphs demonstrates performance against set targets historically and in the current period, and supports users in making an assessment of the likelihood of meeting a commitment or goal. This should be accompanied by a fair and honest explanation.

Practice to Avoid: Lack of openness Failing to identify where current performance was off track, or where goals were unlikely to be met in future periods.

6.2 Carbon Offsets

Carbon offsets are not encouraged for uptake by central government bodies to meet their GGC targets. This example has been included to demonstrate appropriate disclosure, where an organisation chooses to use carbon offsets.

TCFD requirement: Describe the targets used by the organisation to manage climate-related risks and opportunities and performance against targets.

Met Office, 2023-24

Good Practice:

The Met Office includes details on its decarbonisation strategy running to their goal date of 2030. The report includes details on the carbon offsets purchased in the period, and plans for future periods including the quality, location and programmes for the offsets.

Why It’s Good Practice:

The Met Office clearly conveys the key information on their emissions reduction story, including key milestones, progress on decarbonisation during the period, and focus areas for the future. The specific KPIs/ metrics chosen, and net zero strategy being pursued underpin this story.

Transition plans outline the steps an organisation will take to achieve a future decarbonisation goal. It includes key actions, timelines, resources, and risk management to guide the shift from the current state to the desired outcome.

6.3 Comparable Information and Data

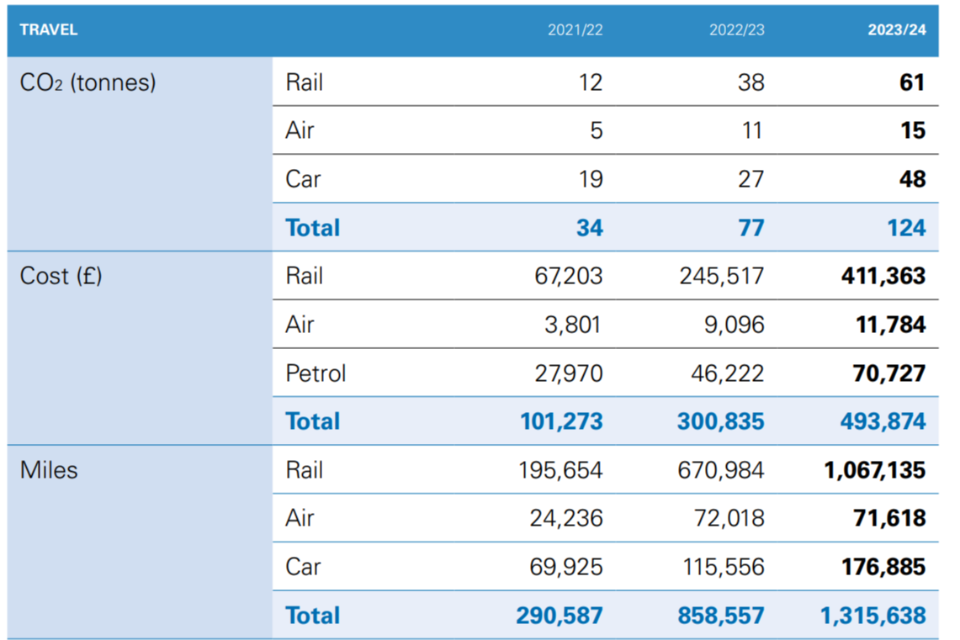

Office for Standards in Education, Children’s Services and Skills (Ofsted), 2023-24

Arts Council England (ACE), 2023-24

Good Practice:

Ofsted included their emissions from travel in a single graph to show the relative climate impact of each form of travel.

ACE uses a single table to demonstrate the emission from different forms of transport, and the related cost and distance travelled.

Why It’s Good Practice:

Both reports used tables and graphs which are simple enough for users to easily compare and contrast data. ACE’s table and Ofsted’s chart were easy to understand with clear totals and the use of bold text and colours to highlight key information.

Using side-by-side charts and tables for the same population of data allows users to compare the relative significance and impacts of various KPIs easily.

Using a single chart to present different emission scopes and sources conveys the significance of each driver, and overarching decarbonisation trends to the user. This can be accompanied by an assessment of the level of control the organisation has over each scope and category.

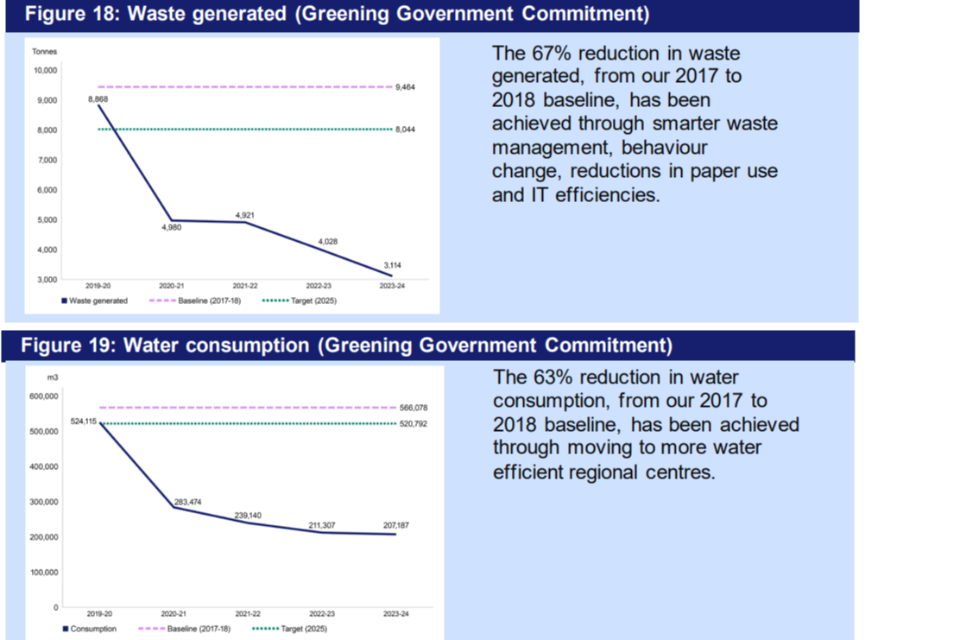

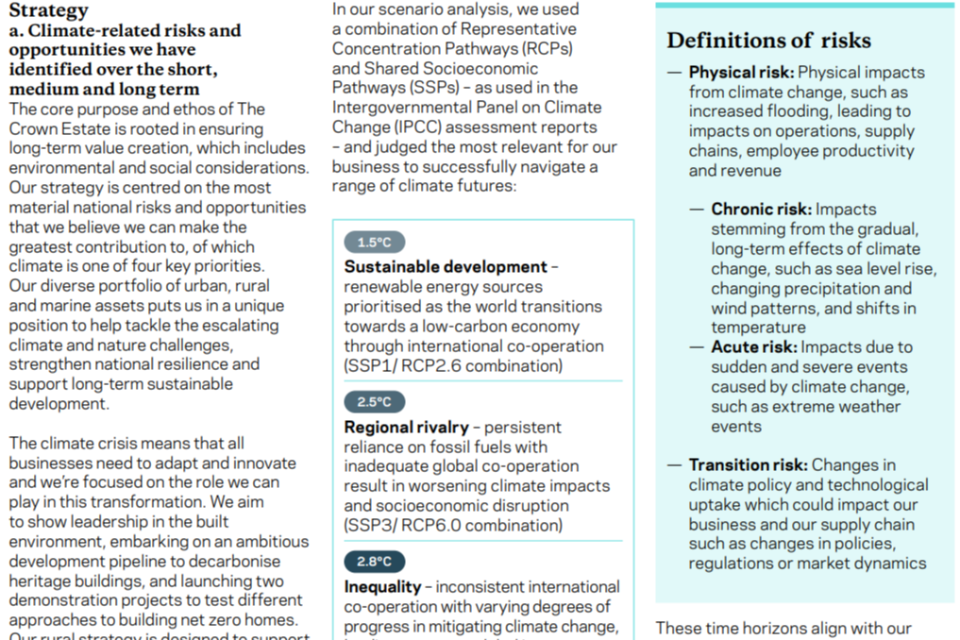

HMRC, 2023-24

SRG requirement: Reporting entities must report water use and absolute values for waste from the organisation‘s estate.

Good Practice:

HMRC uses tables, charts, and graphs to clearly present water, waste and other environmental metrics. This data is depicted alongside relevant baselines and targets. They provide high-level narratives to explain trends and where performance is behind target.

Why It’s Good Practice:

HMRC uses graphs to track environmental metrics over the GGC period - with baselines and targets added to support efficient data comprehension. Historical data enables trend analysis of progress over time. Commentary explains the data’s significance and context for the department. This allows users to make an objective assessment of performance and identify improvement areas.

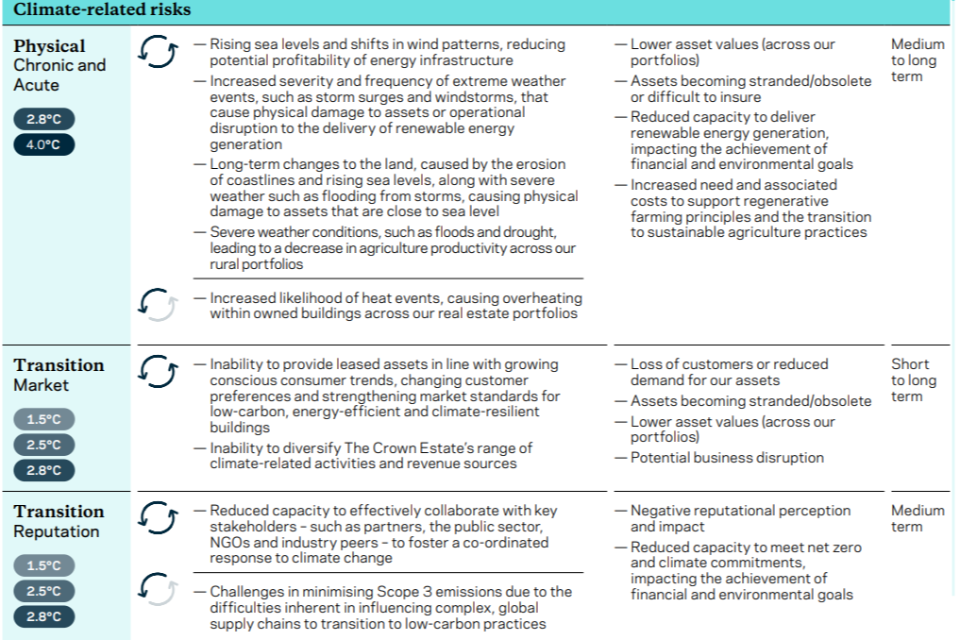

7. Strategy

TCFD’s Strategy recommendations are crucial for embedding climate resilience into long-term planning and decision-making.

TCFD’s Strategy recommended disclosures are not mandatory in central government ARAs until 2025-26. This section analyses Strategy-related disclosures from early adopters of TCFD in central government and the wider public sector.

By following TCFD’s strategic disclosures, government bodies can clearly communicate how climate-related risks and opportunities are integrated into their organisational strategies, ensuring transparency and accountability.

Good Practice

-

Consistency and Specificity: Ensure consistency between the strategy disclosures and other sections of the report, with specific actions, timelines, and accountability for managing climate-related risks and opportunities.

-

Long-Term Focus: Provide a long-term perspective on how the organisation plans to adapt to or mitigate climate-related risks and seize opportunities, outlining milestones and targets.

-

Use of Scenario Analysis: Incorporate scenario analysis to assess the potential financial and operational impacts of climate-related risks under various climate futures (or global warming levels). Explain the assumptions and results of these scenarios in relation to strategy.

-

Materiality: Prioritise climate factors most relevant to the organisation’s operations. Focus on significant risks and opportunities related to climate change and sustainability.

Practice to Avoid

-

Immaterial Opportunities: Consider the relative impact of opportunities when deciding whether to include them in scenarios.

-

Short-Term Focus : Focusing only on short-term risks and not addressing long-term climate impacts, which undermines the credibility of the organisation’s approach to sustainability.

7.1 Time Horizons

TCFD recommended disclosure a): Describe the climate-related risks and opportunities the organisation has identified over the short, medium, and long term.

The Crown Estate, 2023-24

Good Practice:

The Crown Estate met the requirements of the Strategy a) recommended disclosure – providing details on time horizons, the risks, and their impacts. They describe the specific climate-related issues potentially arising in each time horizon that could have a material financial impact on the organisation. In addition, they explain in detail the scenario and processes used to determine which risks and opportunities could have a material financial impact and what is considered as short-, medium-, and long-term time horizons.

Why It’s Good Practice:

The Crown Estate’s explains the risks and scenarios analysed. The tabular format for risk and opportunities supports user to understand and compare information, as well as make their own assessment.

Providing additional detail (e.g., definitions, in-depth explanations) as new elements of the TCFD framework are introduced supports users to understand the disclosures and requirements.

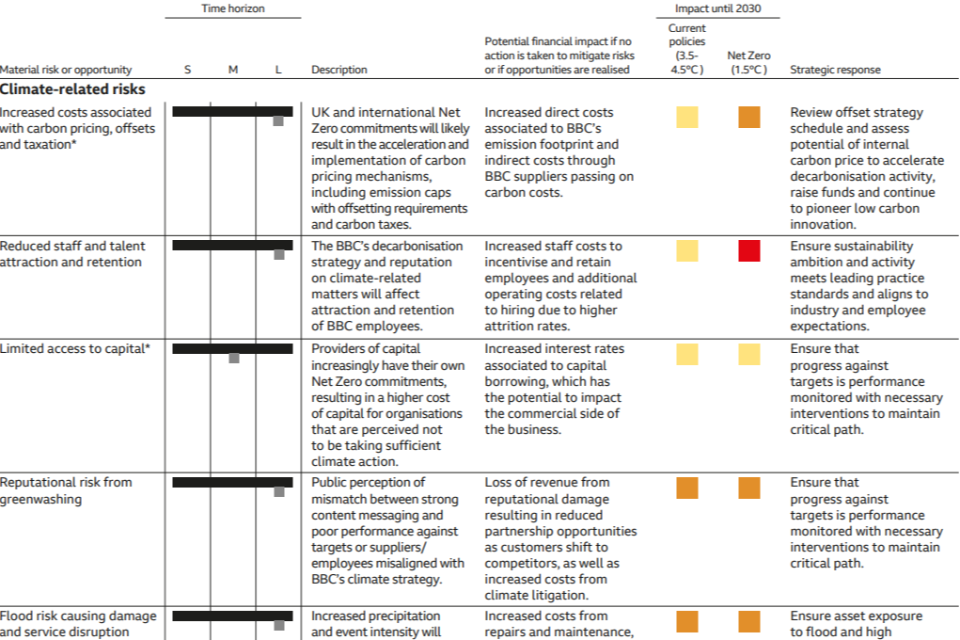

8. Material Climate-related Risks and Opportunities

BBC, 2023-24

Good Practice: The BBC evaluates risks and opportunities over their business and strategic time horizons. They consider the potential financial impacts (pre-2030) of the net zero transition, and their strategic response.

Why It’s Good Practice:

The BBC’s scenario analysis for climate-related risks offers a thorough and forward-looking approach. The analysis explores multiple climate scenarios, helping the BBC assess potential impacts on its operations and resilience. It demonstrates:

-

Strategic foresight: Identifying how various climate outcomes could affect financial, operational, and environmental aspects.

-

Clear metrics and outcomes: Providing measurable results linked to each scenario.

-

Alignment with TCFD guidelines: Integrating climate risk into decision-making processes. This clarity and depth enable better stakeholder understanding and preparedness.

Setting out the climate scenarios analysed, and assessment criteria allows users to understand the analysis being undertaken. A tabular form allows for material risks and opportunities to be compared over the same variables and timeframes.

Only material opportunities should be included in the ARA. Information is material if its omission or misrepresentation could reasonably be expected to influence the decisions primary users take on the basis of the ARAs as a whole. Parliament are the primary users for central government bodies.

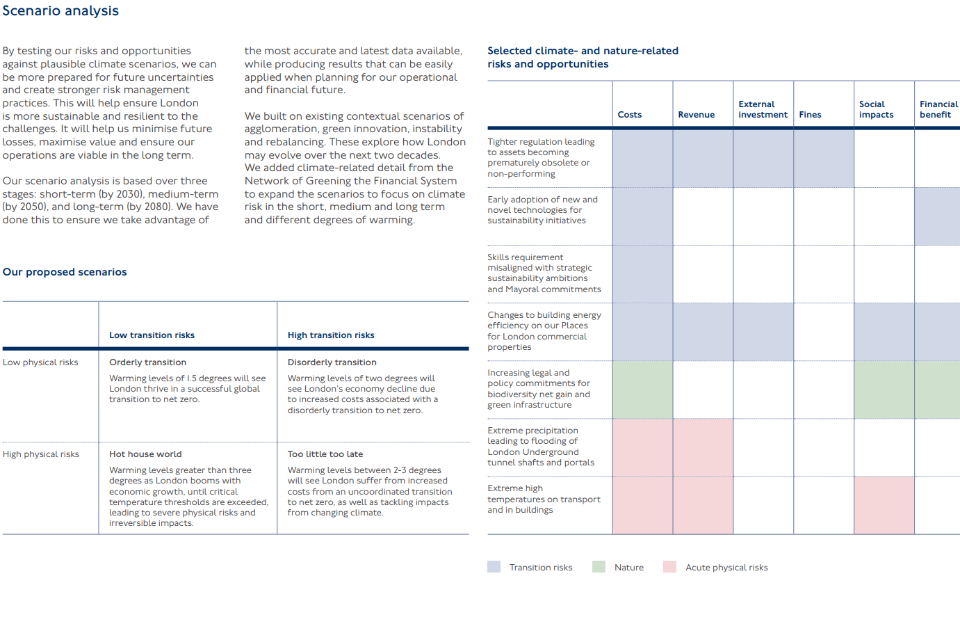

9. Scenario Analysis

9.1 Strategy c)

TCFD recommended disclosures for Strategy c): Describe the resilience of the organisation’s strategy, taking into consideration different climate-related scenarios, including a 2°C and a 4°C scenario.

Transport for London (TfL), 2023-24

Good Practice:

TfL analyse both climate risks (transitional and acute physical) and environmental risks under different scenarios – considering the impact on their accounts.

Why It’s Good Practice:

TfL scenario analysis provides a structured, forward-looking assessment of potential climate-related risks aligned with TCFD. TfL uses multiple climate scenarios considering different warming trajectories to assess potential impacts on infrastructure and services. They also apply a clear decision-making framework to analyse and link risks to strategic decisions, ensuring that policies align with long-term climate resilience.

Considering the financial impacts of various risks is key to implementing TCFD’s recommendations.

9.2 Time horizons, Impacts and Climate Scenarios

TCFD recommended disclosures for Strategy:

a) Describe the climate-related risks and opportunities the organisation has identified over the short, medium, and long term.

b) Describe the impact of climate-related risks and opportunities on the organisation’s operations, strategy, and financial planning

c) Describe the resilience of the organisation’s strategy, taking into consideration different climate-related scenarios, including a 2°C and a 4°C scenario.

9.3 The Crown Estate, 2023-24

Good Practice: The Crown Estate complied with the Strategy a) to c) recommended disclosures. They included the impact on operations, strategy, and financial planning in the following areas:

-

products and services

-

supply chain

-

adaptation and mitigation activities

-

investment and grants in research and development

-

operations (i.e., types of operations, location of facilities)

Why It’s Good Practice:

The Crown Estate considers climate, and its impact from a holistic point of view on their overall strategy. This effectively provides users with an appropriate narrative for disclosures.

10. Other Climate and Environmental Reporting

The SRG, GGCs and FReM include other requirements and voluntary disclosures on climate, the environment, and sustainability reporting. This section considers these other topics.

Good Practice

-

Integrated Reporting: Linking connected or interlinked reporting requirements across the ARA, support user understanding and navigation.

-

Quantification: Provide figures to support sustainability performance and enhance the ARA’s credibility.

-

Materiality: Prioritise environmental factors most relevant to the organisation’s operations. Focus on significant risks and opportunities related to climate change and sustainability.

-

Sustainable Policy Goals: Report progress against Outcome Delivery Plans and international policies (e.g., UN SDGs). Highlight how operations contribute to sustainability strategies.

Practice to Avoid

- Lack of Cohesion: Consider the organisation and its context, when deciding how to lay out sustainability-related information in ARAs.

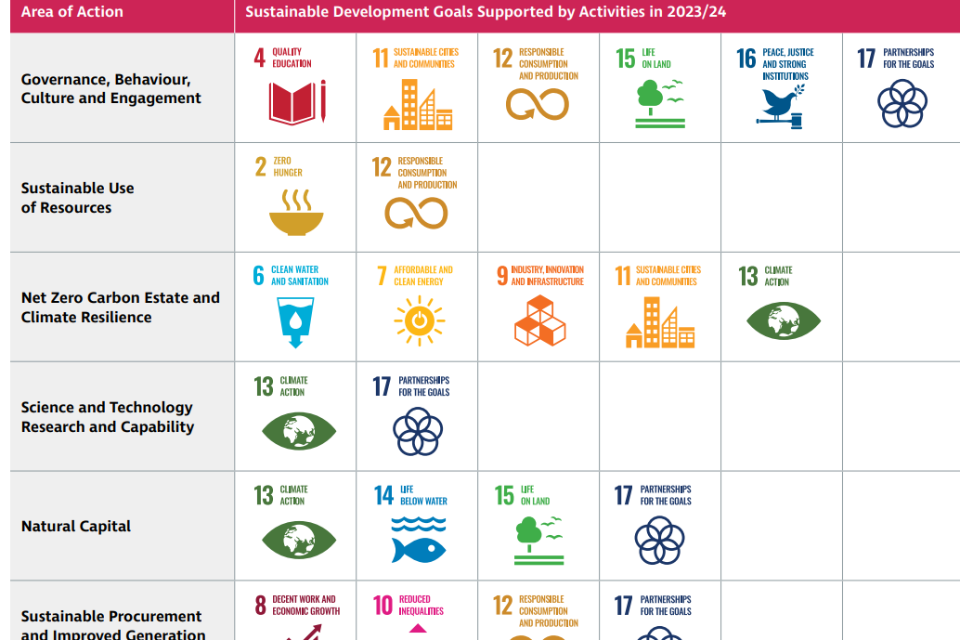

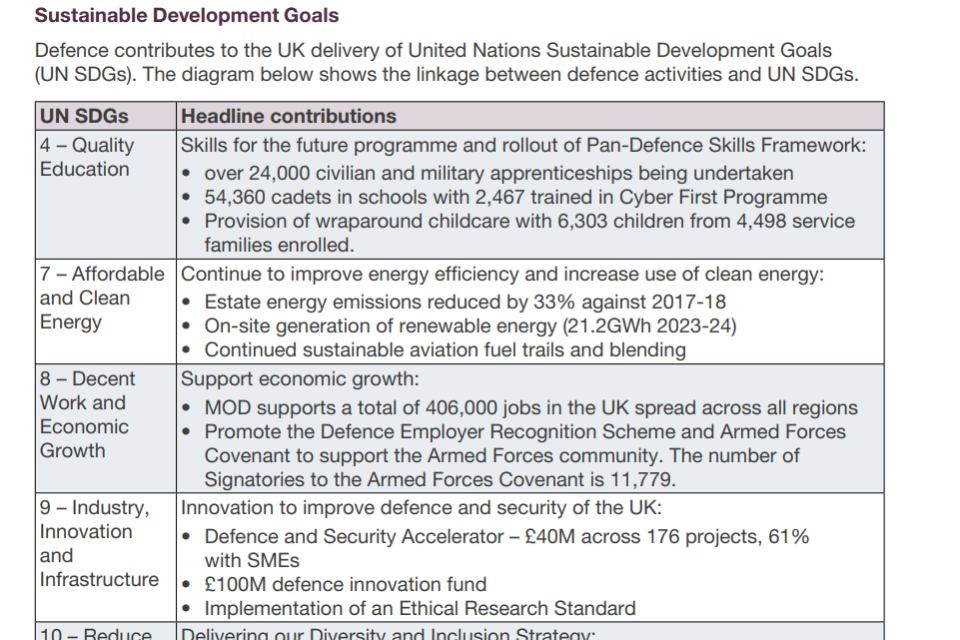

10.1 Reporting against the UN Sustainable Development Goals

FReM requirement: Departments should clearly identify where their performance contributes towards delivery of relevant UN Sustainable Development Goals (SDGs).

Defence Science and Technology Laboratory (Dstl), 2023-24

Ministry of Defence (MOD), 2023-24

The Department for Transport (DfT), 2023-24

Good Practice:

-

Dstl linked their own areas of action to UN SDGs.

-

MOD linked their activities to UN SDGs delivered.

-

DfT set out their sustainability report by categorising specific sustainability topics by the UN SDGs they address.

Why It’s Good Practice:

Each approach by Dstl, MoD and DfT demonstrated how the organisation was working towards each UN SDGs and provided users with a big picture view on sustainable goal delivery.

When structuring ARAs, considering intersecting performance reporting requirements in the context of the organisation, its strategy, and governance processes - can help drive more integrated and connected reports.

10.2 Nature Recovery

SRG requirement: Central government bodies that hold significant natural capital or landholdings must summarise their Nature Recovery Plans for their land, estates, operations and resources. These should be grounded in natural capital assessments where possible and commit to area-based targets for delivery.

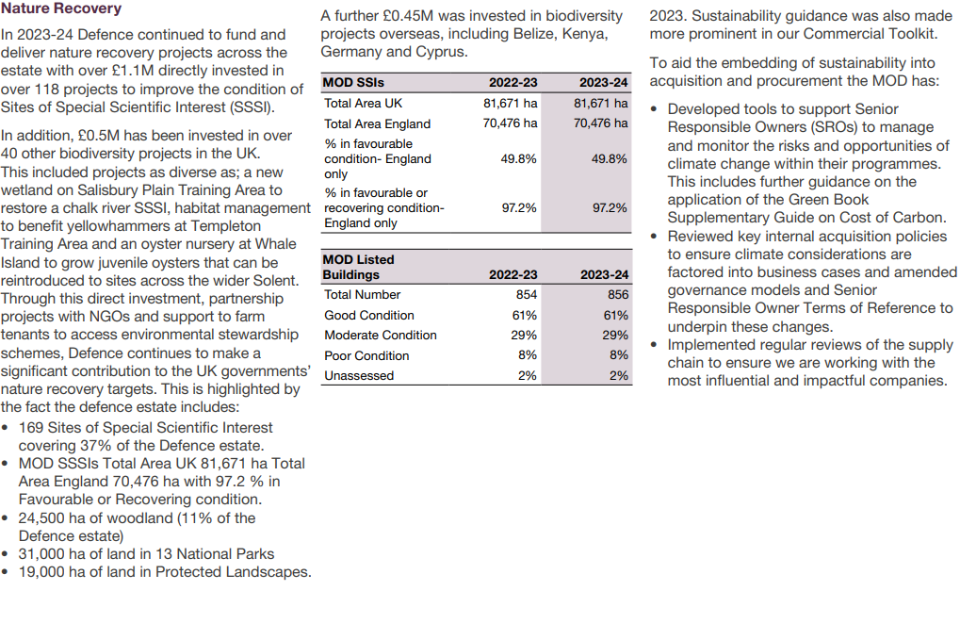

Ministry of Defence (MOD), 2023-24

Good Practice:

MOD identifies overseas sites, choosing to go further than the national boundary set in the GGCs. They identify and calculate suitable KPIs to demonstrate overall performance against Nature Recovery.

Why It’s Good Practice:

Information is quantified, with units chosen to effectively convey information. Monetary values are included to give context for spending. The department uses percentages to demonstrate the relative significance to the whole estate. This provides context to the primary user.

11. Key Takeaways

Sustainability reporting is developing at pace. Implementing the TCFD recommendations in central government and public sector represents a significant step towards more integrated and comparable annual reports.

While progress has been made, full integration of TCFD-aligned disclosure remains challenging and requires a shift in mindset. The phased implementation and ‘comply or explain’ basis for disclosure are designed to support this effort. Reporting entities must continue to develop their own TCFD-aligned disclosures and improve sustainability reporting overall.

Building capability within the finance profession and capacity across government will be crucial for effectively preparing for the impacts of climate change and achieving the government’s statutory net zero commitment.

[1] Good practice and best practice have been used interchangeably in this document. Good and best practice in ARAs can take different forms. The flexibility in reporting frameworks means there is naturally some variation in, and a range of approaches to, effective disclosure.

[1]Figure 2 and 3 in the FReM offer guidance to preparers on what information should be published and where and have been included on this slide.

[2]Only central government bodies that laid their ARAs before the summer parliamentary recess have been evaluated in this guide. This prompt laying and publication ensures that the disclosures are timely.

[3]These readability characteristics were identified in the Government Financial Reporting Review. Similar characteristics of accountability, transparency, accessibility and understandability are used by the NAO in their own Good Practice Guides.

[4] The Greenhouse Gas (GHG) Protocol categorises emissions scopes into Scope 1 covers direct emissions from owned or controlled sources Scope 2 includes indirect emissions from purchased energy, and Scope 3 encompasses all other indirect emissions from the entire value chain, such as business travel, suppliers, product use, and waste.