Factsheet: Carbon border adjustment mechanism

Published 24 April 2025

© Crown copyright 2025

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/factsheet-carbon-border-adjustment-mechanism-cbam/factsheet-carbon-border-adjustment-mechanism

-

In spring 2024, the previous government consulted on the detailed policy design and implementation of the UK CBAM in a consultation entitled ‘Introduction of a UK carbon border adjustment mechanism from January 2027’.

-

The government published its response on 30 October 2024 confirming that a UK CBAM will be introduced on 1 January 2027.

-

The government published the primary legislation for technical consultation on 24 April 2025. Alongside this, a supporting policy update was published.

1. Carbon leakage

-

The UK is taking rapid action on industrial decarbonisation to meet net zero. This includes the use of carbon pricing through the UK Emissions Trading Scheme (UK ETS).

-

As not all jurisdictions are moving at the same pace, and many countries do not yet have domestic carbon pricing mechanisms, carbon leakage risk is then created.

-

Carbon leakage is the movement of production and associated emissions from one country to another due to different levels of decarbonisation effort through carbon pricing and climate regulation.

-

Carbon leakage can undermine efforts to reduce global emissions and curtail private investment in decarbonisation – compromising efforts to limit global warming to 1.5°C.

2. The UK Carbon Border Adjustment Mechanism (CBAM)

-

The government will introduce the UK Carbon Border Adjustment Mechanism (CBAM) on 1 January 2027.

-

This will ensure highly traded, carbon intensive products from overseas face a comparable carbon price to that which would have been payable had they been produced in the UK, so that UK decarbonisation efforts lead to a true reduction in global emissions rather than simply displacing carbon emissions overseas.

3. Sectors and products initially in scope of the UK CBAM

-

The UK CBAM will place a carbon price on some of the most emissions intensive industrial goods imported to the UK from the aluminium, cement, fertiliser, hydrogen and iron & steel sectors that are at risk of carbon leakage.

-

Within these sectors, the CBAM will only apply to specific imported ‘CBAM goods’. These goods are determined by the product level scope of the CBAM and are identified by commodity code as listed in Annex B of the ‘Government Response to the introduction of a UK CBAM Consultation’.

-

The glass and ceramic sectors will not be in scope of the UK CBAM from 2027 as originally proposed (in December 2023).

-

The sectoral and product level scope of the CBAM will be kept under review beyond 2027 as new evidence comes to light to reflect changes to carbon leakage risk as well as methodological and technological advances.

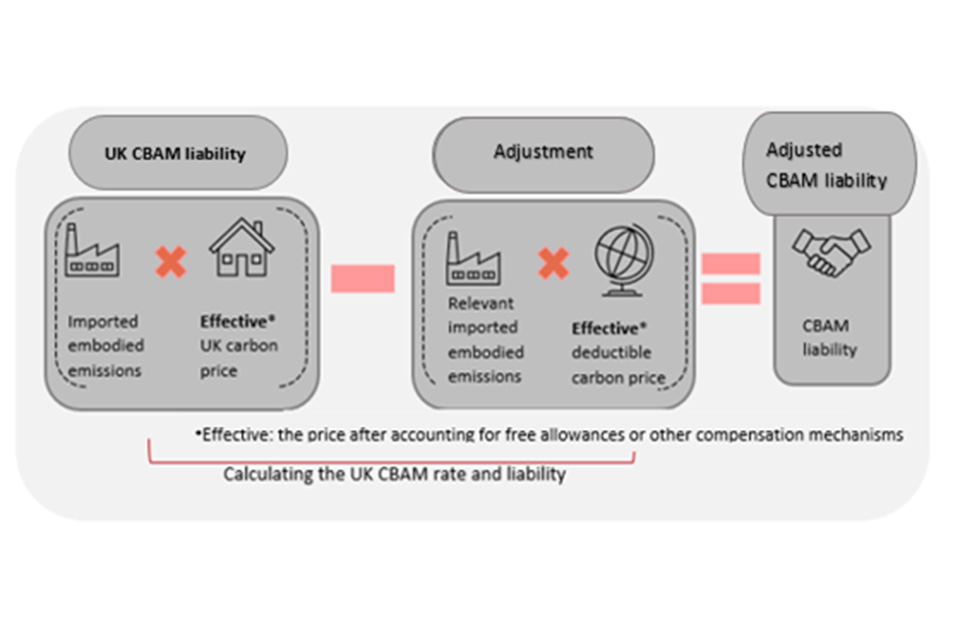

4. Calculating the UK CBAM liability

Calculating the UK CBAM liability

5. Relevant imported emissions

-

The UK CBAM will apply to both the direct and indirect emissions embodied in imported CBAM goods, including those emissions embodied in relevant precursor goods at a point further up the value chain.

-

It is important for the UK CBAM to cover indirect emissions to ensure comparability with goods produced in the UK, where electricity emissions are subject to both the UK ETS and Carbon Price Support (CPS).

6. Determining embodied emissions

-

The liable person can choose to use either independently verified actual emissions data or default values.

-

From 2027, the government will proceed with a single default value set per product. The government will confirm the methodology to be used for their calculation and publish default values in advance of the introduction of the CBAM in 2027.

-

Post-2027, the government is considering the viability of moving to an alternative approach for default values.

7. Setting the UK CBAM rate

-

The UK CBAM rate will be applicable per tonne of embodied emissions attributed to CBAM goods and will be comparable to the carbon price faced in the UK by domestic producers, net of reductions.

-

As a result, the UK CBAM rate will reflect the UK ETS, CPS, and free allowances. As the UK ETS and CPS place a carbon price on indirect emissions, these costs will be reflected within the rate.

8. Adjusting for overseas carbon prices

-

The CBAM liability can be reduced if the embodied emissions in the imported CBAM goods are subject to a deductible carbon price overseas and the importer provides evidence of this.

-

Only deductible carbon prices will be accounted for in this adjustment. Deductible carbon pricing schemes are those which place a price directly or indirectly on emissions in the form of a tax or an emissions trading scheme.

-

Further detail and guidance will be published in advance of commencement of the UK CBAM.

9. Liable person and registration

-

The liable person for the UK CBAM charge will either be the person responsible for the goods when they are released into free circulation if there are customs controls, or the person on whose behalf the goods are moved into the UK if there are no customs controls.

-

The liable person will not need to register or account for the CBAM if the total value of their CBAM goods passing a tax point falls below a minimum registration threshold of £50,000 over a rolling 12 month period. This is to ensure that the costs of complying with the CBAM are more proportionate to the carbon leakage risk the government is seeking to address.

10. Payments

- As the UK CBAM will operate as a tax, liable persons will need to account for all CBAM goods that pass a tax point during an accounting period.

- Following the end of each accounting period, liable persons will have to submit an online tax return and pay their CBAM liability.

- Payments for the first annual accounting period (1 January 2027 to 31 December 2027) will be due at the end of May 2028.

11. Interaction with UK Emissions Trading Scheme (ETS)

-

The UK ETS places a price on greenhouse gases emitted by domestic producers. The UK ETS is a cap-and-trade system in which the market determines the price of allowances. Total emissions and allowances under the scheme are capped, reducing over time to incentivise decarbonisation.

-

The UK’s current main measure to mitigate carbon leakage risk is the system of free allocation under the UK ETS. The UK CBAM will work cohesively with the UK ETS. That includes on free allowances, where the methodology to determine the UK CBAM rate will reflect the availability of free allowances in the domestic market to ensure imported products are subject to a carbon price comparable to that incurred by UK production, mitigating the risk of carbon leakage.

-

To put the UK ETS on a net zero consistent trajectory, the UK ETS Authority will reduce the number of ETS allowances available for purchase from government by 45% between 2023 and 2027. The number of free allowances will also decrease.

-

In December 2023, the UK ETS Authority published the Free Allocation Review to seek views on how free allocation policy could be adjusted to better target free allocations for sectors most at risk of carbon leakage.

-

In December 2024, the UK ETS Authority published an interim consultation as part of the Free Allowance Review. Following the UK government’s announcement to introduce a CBAM, this consultation sets out how the UK ETS Authority could adjust free allocation to reflect the reduced risk of carbon leakage for CBAM sectors, and to increase the effectiveness of the CBAM as a leakage mitigation policy.

-

Any changes to free allocations for CBAM sectors will be announced as part of the wider Free Allocation Review response by the end of 2025, and take effect at the start of the next allocation period in 2027. This will align with the introduction of the UK CBAM, ensuring a holistic policy approach to carbon leakage. It will also ensure that changes to free allocation resulting from the review, and any changes to adjust free allocation for CBAM covered sectors, will all take place at the same time, minimising uncertainty for business.

12. Next steps

-

As work on the implementation of the tax proceeds, the government will continue to keep all areas of the UK CBAM design and implementation under review and would welcome continued engagement from all interested stakeholders.

-

There are two established working groups for domestic and international stakeholders. For domestic stakeholders, HMRC coordinate a UK CBAM Joint Industrial Working Group. For international stakeholders, HM Treasury coordinate a UK CBAM International Group.

-

The draft primary was published on 24 April 2025 for technical consultation. Alongside this, a policy update note was published.

-

The UK CBAM will require secondary and tertiary legislation. The government intends to publish all the legislation in draft ahead of introducing it before Parliament. This will allow interested stakeholders to review the legislation and ensure it meets the policy intent.