Affordable home ownership schemes: Wales (updated September 2020)

Updated 16 September 2020

© Crown copyright 2020

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/joint-service-housing-advice-office-leaflet-index/affordable-home-ownership-schemes-wales-updated-april-2020

- Serial number: JSHAO/06

- Date: March 2020

- Review date: April 2021

Affordable home ownership schemes in Wales

This handout has information on:

-

Help to Buy: Shared Equity Loan

-

Homebuy

-

homes within reach shared equity

-

rent first

Many personnel may have discounted the idea of buying a property because they believe that they can’t afford it. Over recent years it has become increasingly difficult to obtain an affordable mortgage unless you have a significant deposit. The Mortgage Market Review has also impacted on mortgage applications as providers are now required to look more closely at how affordable your initial mortgage repayments will be, taking into account not just your income but also your outgoings such as general cost of living and existing loans. Lenders will also look at the future affordability of your mortgage payments to ascertain whether a rise in interest rates would impact on your ability to meet your repayments.

Whilst the tightening of mortgage regulations may appear to make home ownership even harder to achieve, Affordable Housing Schemes are designed to bridge the gap between the asking price for a property and the available mortgage, increasing the range of people who are able to get on, or move up, the property ladder.

This handout will focus on the Affordable Housing Schemes available in England. Similar schemes are available throughout the UK and information on those specific to Scotland, Wales and Northern Ireland are available on request from JSHAO. Service personnel have been designated as ‘Priority Status’ on these schemes (excluding Northern Ireland). Although this is no guarantee that an application will be accepted, it ensures applications from service personnel will be treated the same as social housing tenants for a period up to 12 months after discharge.

Help to Buy equity loan Wales

You can use Forces Help to Buy with this scheme, JSP 464 Part 1 Chapter 12.

How it works

Help to Buy Wales allows eligible purchasers to buy new-build homes with assistance from the Welsh Government in the form of a shared equity loan.

What does this mean in practice?

Help to Buy Wales shared equity loans are available to both first-time buyers and home movers wishing to purchase new-build homes worth up to £300,000.

With Help to Buy Wales, buyers won’t be able to sub-let their home.

With Help to Buy Wales:

- buyers need to contribute a deposit equal to 5% of the property price

- the Welsh Government (through Help to Buy (Wales) Ltd) will fund a shared equity loan for up to 20% of the purchase price

- buyers will then need to secure a mortgage to cover the remaining balance.

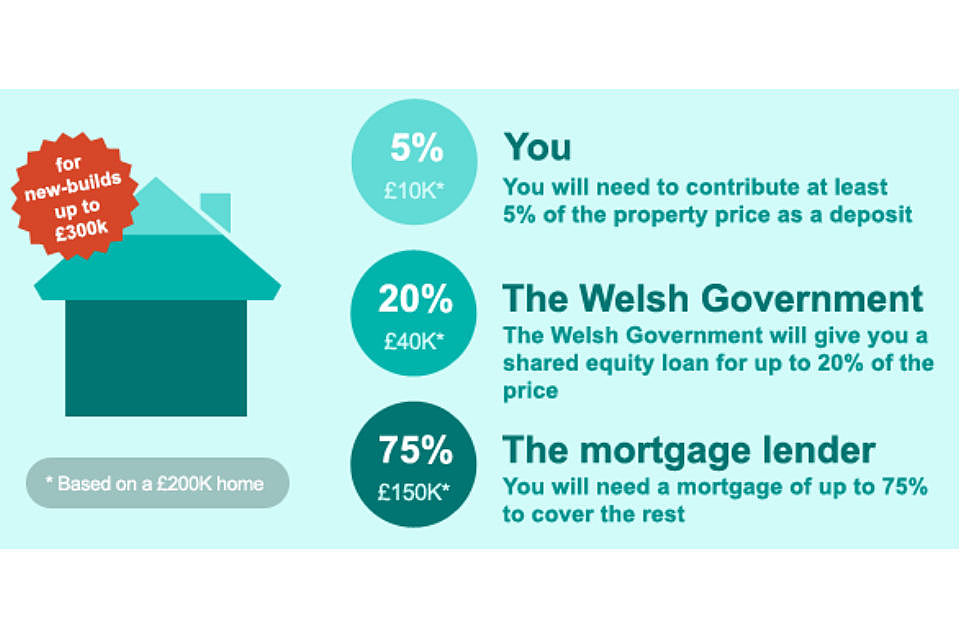

Example undertaking

Infographic showing that for a property worth £200,000, you would need a Cash deposit of £10,000, shared equity loan of £40,000 and your mortgage covers £150,000.

| For a property worth £200,000 | Amount | Percentage |

|---|---|---|

| Cash deposit | £10,000 | 5% |

| Shared equity loan | £40,000 | 20% |

| Your mortgage | £150,000 | 75% |

If in the future the home in the table above sold for £210,000 the buyer would get £168,000 (80%, based on their mortgage and the cash deposit) and pay back £42,000 on the shared equity loan (20%).

The buyer will pay off their mortgage using the proceeds of the sale and will then repay the Help to Buy Wales shared equity loan.

Are there any fees attached to the shared equity loan?

From the time a buyer receives the shared equity loan they will be charged a small administration fee of £1 per month.

Then, in the sixth year, they’ll be charged interest of 1.75% per annum of the original shared equity loan amount. After this, the interest will increase every year. This increase is worked out by using the Retail Prices Index plus 1%.

All buyers will be contacted before the shared equity loan interest starts and they’ll also be sent a statement about their shared equity loan each year.

The fees do not count towards paying back the shared equity loan.

Important notes

Can I sublet my Help to Buy Wales home?

No. Help to Buy Wales is designed to assist you to move on to or up the housing ladder. If you wish to sublet, you will first have to repay the HtBW shared equity loan in full. In exceptional circumstances (for example, a serving member of the armed forces staff whose tour of duty requires them to serve away from the area in which they live for a fixed period) then sub–letting can be considered. In these circumstances you would require approval from HtBW and also your mortgage lender.

Can I own other homes and buy a Help to Buy Wales home?

No. Help to Buy Wales is designed to assist you to move on to or up the housing ladder and must be your only residence (not including renting SFA, please refer to the previous sections for details). This means you will be expected to sell your current home if moving up the ladder. The disposal of your current home will be verified by your solicitor/conveyancer before you can proceed to exchange contracts on the Help to Buy Wales home.

Can I own a Help to Buy Wales home and buy a second home?

No. Help to Buy Wales is designed to assist you to move on to or up the housing ladder. If you can afford to purchase another home, you will have to repay the HtBW shared equity loan in full.

Further details of the Help to Buy Wales shared equity loan can be found within the guidance document available online.

HomeBuy Wales

The Homebuy Wales scheme can help people who are unable to meet their housing needs buy a suitable home.

Homebuy is a Welsh Government scheme that offers support to households by providing an equity loan (normally 30% of the approved purchase price, but this can be increased to 50%) to assist in purchasing a property.

It is intended to help people who would otherwise need social housing. It is not intended for people who can afford to buy a suitable home without assistance or those who are suitably housed but who wish to move to a more expensive location.

The loan can be repaid at any time but must be repaid when the property is sold.

How does Homebuy work?

Homebuy is funded and supervised by the National Assembly for Wales, which has responsibility for housing associations in Wales.

If you qualify for the scheme, you will normally need to contribute 70% of the purchase price of a home through a mortgage and/or personal savings, although in certain circumstances you could contribute as little as 50% of the purchase price. The housing association will lend you the rest.

To fund your percentage of the purchase price you will need to arrange a mortgage from an approved lender. For the purposes of the Homebuy scheme your mortgage must be obtained from a building society, a bank, a friendly society or an insurance company. The housing association will give detailed definitions of these to applicants when they are accepted onto the scheme. Applicants should, under no circumstances, incur any costs in obtaining a mortgage (for example, for a property valuation) until the lender offering to provide the mortgage has confirmed that it is one of these types of lender. Mortgage repayments are usually made on a monthly basis, with the amount sometimes varying if there are changes in interest rates.

There are no monthly payments on the loan from the housing association that covers the remaining percentage of the purchase price. Instead, you repay it when you sell your home. The amount you repay will be the equivalent percentage value of your home at the time you sell it. If you want to, you may repay the loan before you sell, in which case what you repay will be based on the value of your home when you pay back the loan. It is important to remember that the loan must be repaid when you sell the home.

Who qualifies for Homebuy?

To qualify for the scheme, you must first be approved (in writing) by housing association operating Homebuy. To find out who runs the scheme in your area, contact your local council or the National Assembly for Wales.

In considering your application, the housing association must use the rules currently in place at the time you apply. These are published by the National Assembly for Wales. As a guide, you will need to meet at least the following requirements:

-

you must be able to show the housing association either that you are not adequately housed or that you can no longer afford to occupy your current home

-

you must be able to show the housing association that you cannot buy a home suitable for your needs without help from Homebuy. The housing association may turn you down if you could afford to buy a home without help

-

you must be able to obtain a mortgage to cover your contribution and have savings to cover the other costs of buying a home, such as legal costs. The mortgage must be from a qualifying lender such as a bank, building society or insurance company. Other lenders may be acceptable, but you need to check first with the housing association whether the lender can provide a mortgage for the Homebuy scheme

-

you must not be in rent arrears, or in breach of your tenancy agreement, if you are a tenant of a housing association or local council

-

you must not be receiving Housing Benefit or have received it during the 12 months before you apply for Homebuy

-

if you currently own your home or part-own a property, you can only be considered for Homebuy if the local council accepts that you are in housing need. You would have to sell your interest in that home at the same time as buying a home through Homebuy.

Further details of Homebuy for applicants in Wales can be found within the guidance document available online.

Homes within reach Wales

Homes Within Reach is a low-cost home ownership scheme that provides assistance to eligible first-time buyers trying to get on the housing ladder. The scheme is administered by a group of housing associations spread across South Wales.

If you earn a single / joint salary of approximately £15,000 to £40,000 Homes within Reach could help you get on the housing ladder.

All member housing associations work closely with their respective local authorities and new house builders to provide brand new affordable homes for sale utilising an equity loan. This is available to first time buyers who cannot afford to purchase a property outright but are able to meet the long term financial commitment of home ownership. The properties are offered for sale on a ‘shared equity’ basis which means you purchase a percentage of the full open market value of the property. The housing association will provide an equity loan for the remaining percentage which is retained as a charge on the property. Unlike your mortgage, there are no repayments due to the housing association. The loan may be paid back voluntarily or upon a future sale.

The percentage you are able to purchase may vary from development to development. It may be fixed at a given percentage, for example 70%, or you may have the opportunity to purchase between 50% and 90%, dependent upon your affordability.

In the future you will have the opportunity to increase your equity share by purchasing additional equity from the housing association (in portions of no less than 10%). You may also purchase the whole amount of equity outright from the housing association, but this is normally restricted to the first 3 years of occupation. You may not choose to do either as there are no time restrictions of when the equity loan has to be repaid other than upon a future sale.

On specific developments, you may have the opportunity to reduce your equity share by offering back a percentage of equity (no less than 10%) to the housing association who may purchase it for example, if your circumstances change and you no longer can sustain the existing level of mortgage. Please note, however, you will not be able to reduce your mortgage to less than 50% of the property’s value.

You may offer your property back to the housing association who may purchase all your equity share thereby owning it outright and allow you to remain in the property as a tenant paying rent.

Further details of Homes Within Reach for applicants in Wales can be found within the guidance document available online.

Rent First Wales

Rent First is a Welsh Government scheme that provides rented housing at intermediate rents and gives tenants an opportunity to buy their property outright.

Local Authorities can allocate funding for the scheme through their social housing grant allocation.

How it works

You will have the opportunity to purchase the home you are renting and can build up a lump sum towards a mortgage deposit whilst renting the home.

You will initially rent the home and can receive 25% of the rent paid over the duration of the tenancy and 50% of the increase in the property value (if any) during the period of time you have rented the property to use as a deposit towards purchasing the property.

Your Rent to Own Wales agreement lasts up to 5 years, you can apply to buy your home at any time between the end of the second year and the end of the agreement.

Further information can be obtained from Welsh Local Authority in the area where you wish to settle.

Contact the Joint Service Housing Advice Office on the Civilian number: 01252 787574 and Military number: 94222 7574. You can also email the office on rc-pers-jshao-0mailbox@mod.gov.uk.