Innovation finance evidence pack (HTML)

Updated 11 August 2023

© Crown copyright 2023

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/letter-to-the-prime-minister-on-investment-in-innovative-science-and-technology-companies/innovation-finance-evidence-pack-html

INCREASING THE AVAILABILITY OF SCALE-UP INVESTMENT FOR DOMESTIC INNOVATIVE SCIENCE AND TECHNOLOGY COMPANIES

Evidence pack

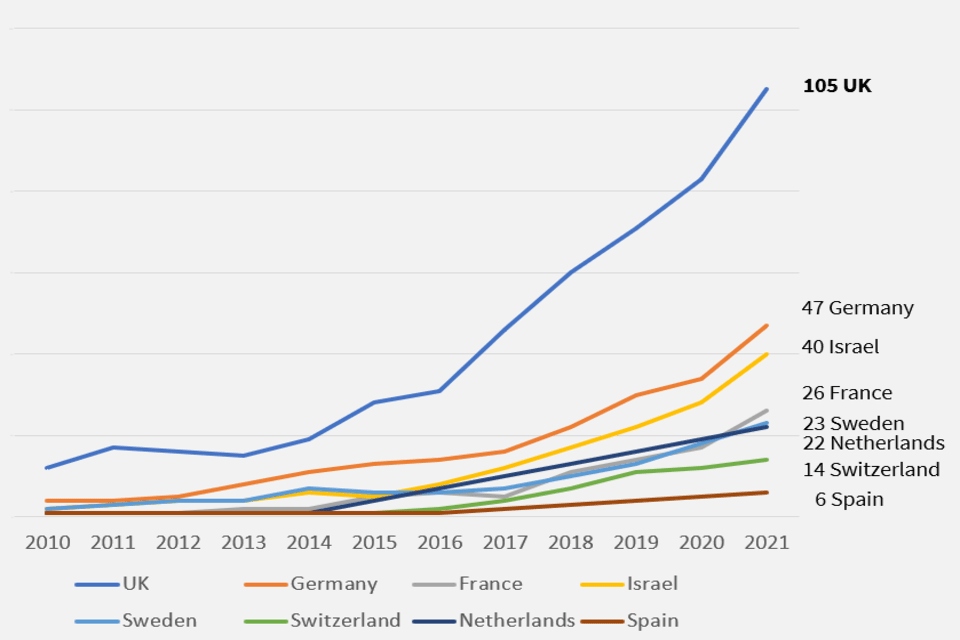

UK start-ups & investments grew 10 times in the last decade

In 2021 the UK became the third country in the world to pass 100 unicorns, after the US and China. The UK now has more unicorns than Germany, France and Sweden combined. The UK is also home to 153 potential future unicorns, valued over $250 million.

Figure 1: UK growth in unicorns, ‘futurecorns’ and venture capital (VC)

Figure 2: International comparison of cumulative unicorns and $1 billion exits

The UK is ‘top 3’ for unicorns in almost every sector

| USA | China | UK | India | Germany | Israel | France |

| Unicorns and over $1 billion exits | 1,000 | 281 | 105 | 49 | 46 | 40 | 26 |

| Fintech | 183 | 36 | 37 | 14 | 7 | 4 | 6 |

| ecommerce | 177 | 85 | 31 | 30 | 26 | 4 | 11 |

| Deep tech | 294 | 69 | 21 | 5 | 5 | 19 | 4 |

| Enterprise software | 316 | 28 | 17 | 5 | 8 | 11 | 3 |

| Health | 173 | 30 | 13 | 2 | 4 | 5 | 3 |

| Food | 42 | 26 | 7 | 5 | 5 | 0 | 0 |

| Transportation | 70 | 63 | 7 | 6 | 7 | 6 | 1 |

| Energy | 37 | 15 | 4 | 0 | 0 | 1 | 1 |

| Travel | 11 | 5 | 3 | 1 | 5 | 0 | 1 |

| Marketing | 88 | 12 | 1 | 4 | 4 | 5 | 3 |

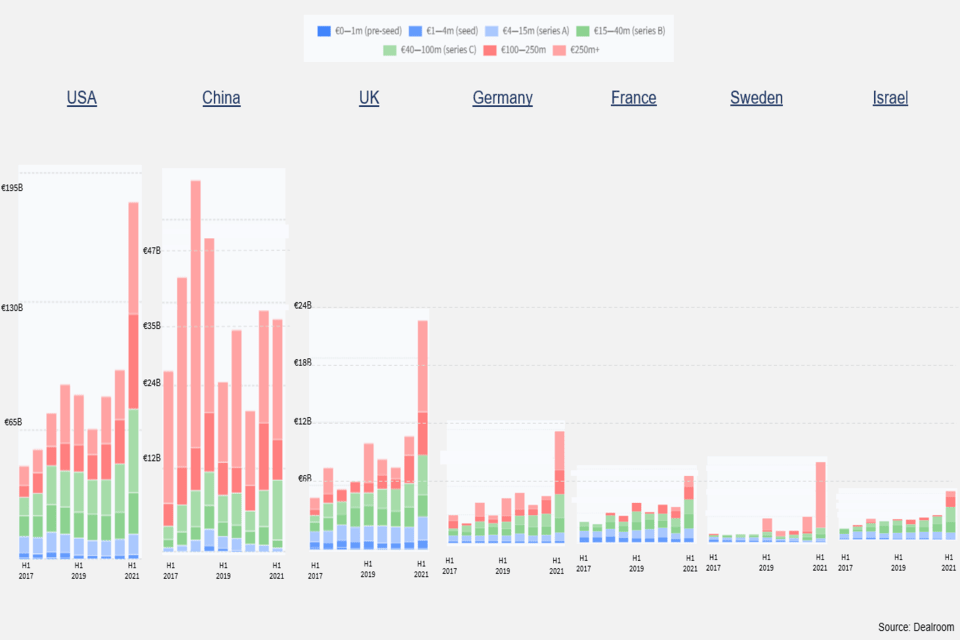

Despite being third in the world for VC investment, the UK is proportionately weak at scale up (over €100 million), particularly in comparison to the USA and China

Figure 3: Breakdown of investments by funding round for select countries

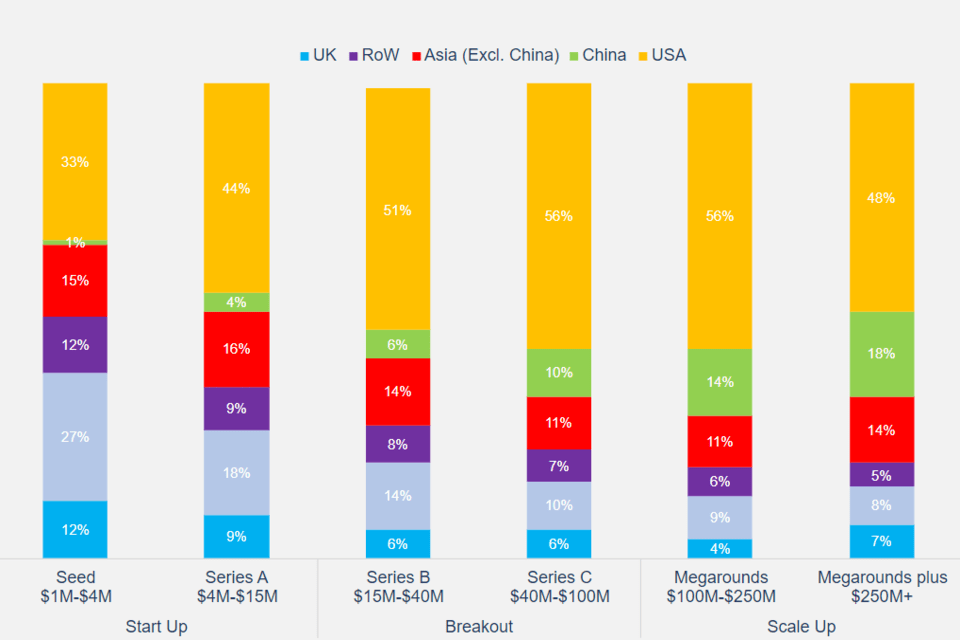

Comparing the fraction of global investments by stage, US investments are 3.6 times larger than UK at early stage, increasing to 9.45 times at scale up

Figure 4: Percentage of global investment in 2020 to 2021 year to date by region per round size

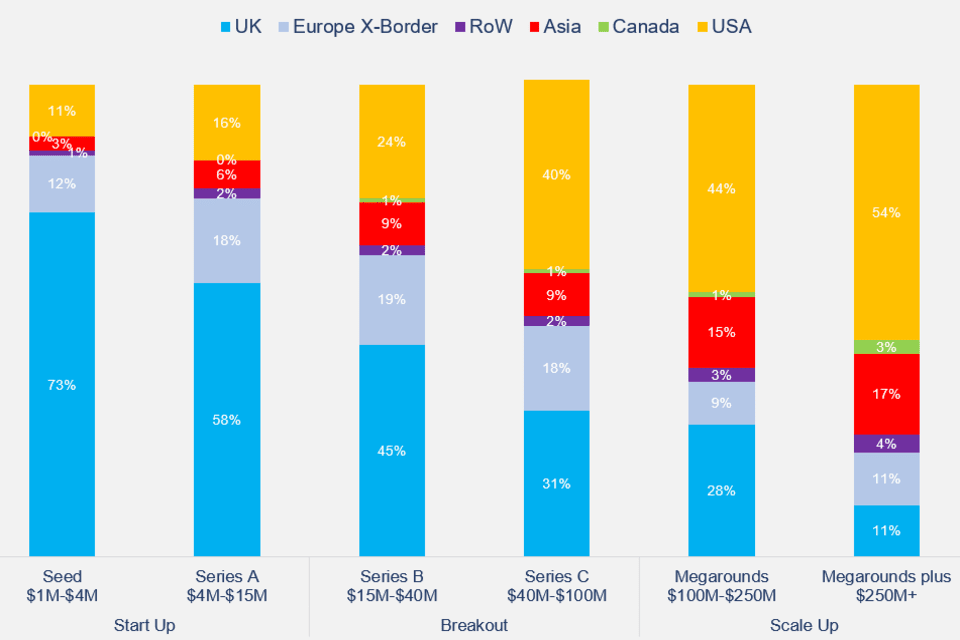

Due to the lack of domestic growth capital most of the investment for UK R&D intensive companies above $100 million is from international sources

Figure 5: Percentage investment in 2020 to 2021 year to date by source round size

Issues to address: experience from asset owners

The issues below were raised during an asset owner roundtable hosted by the Council for Science & Technology (CST), comprising of senior delegates from pension funds, insurers, and endowments This is a summary of themes intended to inform policy discussion and does not represent formal consultation.

Culture and human capital

a. The approach to science and technology (S&T) investment is focussed on the long-term benefits and is countercultural to existing investment culture. Once the environment is created and starts to become successful, it needs supporting and protecting.

b. Investment culture comes from the top diversity at board level could support cultural change. Further government engagement with regulators and other partners on diversity standards for investor and asset owner boards could help to ensure institutions have diverse representation and skills to maintain a focus on long-term performance for beneficiaries.

c. Specialist investing skills If you want to attract the best talent, you need to pay them. The focus should not just be about keeping admin costs down. There is a lack of incentives for investment in S&T businesses to scale up Pension funds do not have sufficient flexibility on fees to enable them to attract the specialist skills they need for impact investing.

d. The level of commercial acumen in deep tech companies is much lower than in other areas Do we lack commercially minded academics in the UK?

Funds

a. Government should focus on incentivising scale. There are not many late-stage growth funds in the UK (compared to USA) Nobody is doing ‘venture growth’ UK needs a scale up equivalent of the British Business Bank run by people who understand how to do investing for growth and impact.

b. Government needs to be ready to support ‘leap of faith’ investments that align with national goals.

Engage and convene investors

a. There is a need for a sustained programme of engagement with clear messages from government on opportunities around national goals.

b. The UK’s S&T strengths need to be better promoted to investors with specific emphasis placed upon emerging UK S&T companies and sectors. Put the spotlight on role models in the tech space who have commercialised their research and publicise where investment has been fruitful.

c. S&T companies solve problems and deliver social outcomes sustainability, energy security, health, addressing inequality. This is a powerful way of framing S&T proposition to investors, which aligns with increasing interest in environmental, societal and governance (ESG) investment opportunities.

Issues to address: experience from business

CST members and secretariat reviewed the experience of more than 30 UK and US businesses as a pilot study to explore the comparatively low rates of scale up investment for innovative UK S&T companies and understand what factors influence the culture and behaviour of funders Interviews centred on what challenges S&T companies had faced in accessing scale up investment in the UK compared to international competitors, and experiences of scaling their company in the UK.

The following issues and suggestions were raised during interviews with companies.

a. There remain barriers to early-stage investment in innovative S&T companies, including university spin outs. Universities and public sector funders have not adequately explored how to strengthen the business management expertise of UK S&T company founders to improve the potential for spin outs to scale up.

b. Government should explore tax as a lever to encourage domestic and international investment in S&T scale ups and the establishment of growth funds in the UK. In addition, research and development (R&D) tax credits should be targeted to drive the S&T priorities identified by government and better promote UK based R&D.

c. There is a lack of specialised innovation infrastructure for testing, experimentation and large-scale manufacturing This creates a challenge for some companies when engaging investors on the long-term plans for the commercialisation of their technologies, and leads to a greater proportion of companies needing to test and manufacture abroad. There is an opportunity for government to engage investors and support the prioritisation of investment in infrastructure to support UK companies commercialising technologies of national importance.

d. There are vast differences in the expertise and experience of UK and US investors (S&T expertise and experience scaling successful businesses). Human capital development for UK investors, as well as ensuring talent on UK company boards, is critical.

We provide case studies of UK and US comparisons in specific technology areas in the following slides We gratefully acknowledge the support of Margaret McLeod at the Massachusetts Institute of Technology for her support on interviews and analysis.

UK and US Twins Funding Experiences – Pilot Study

Differences in the funding experiences of UK and US twins

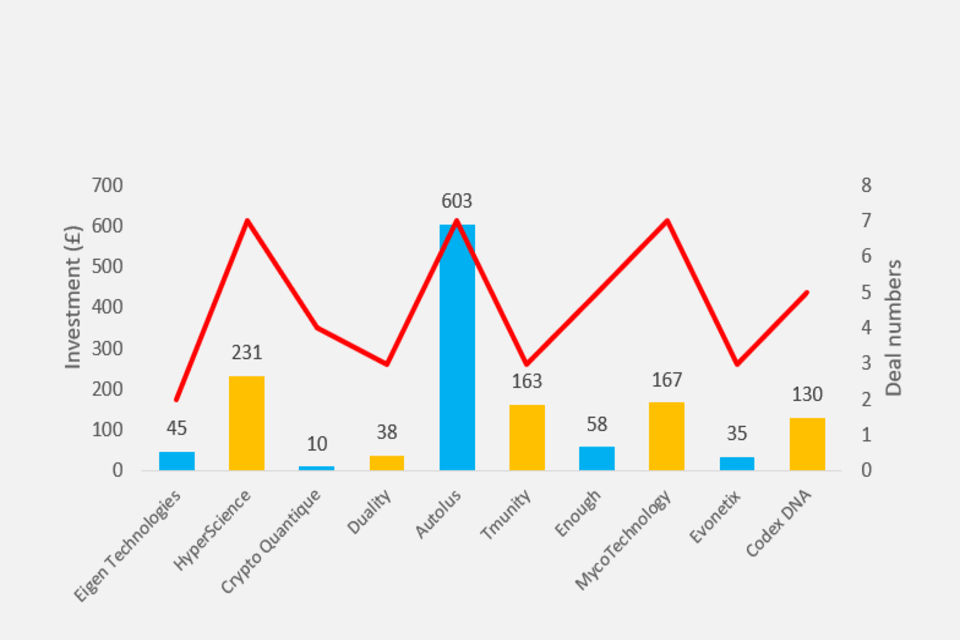

On average, US twins received more than 2.5 times more capital (with numbers rounded to the nearest million) than their UK counterparts, with a greater number of funding rounds.

-

The median funding received by US twins was £162 million and £45 million for UK twins.

-

The mean number of funding rounds for US twins was 5 compared to 4.2 for UK twins.

-

Science-based twins attracted more capital and more funding rounds than those in high technology sectors.

It took US and UK twins a similar amount of time between receiving their first and second VC investment rounds, but US second round VC funding was a third bigger by value.

-

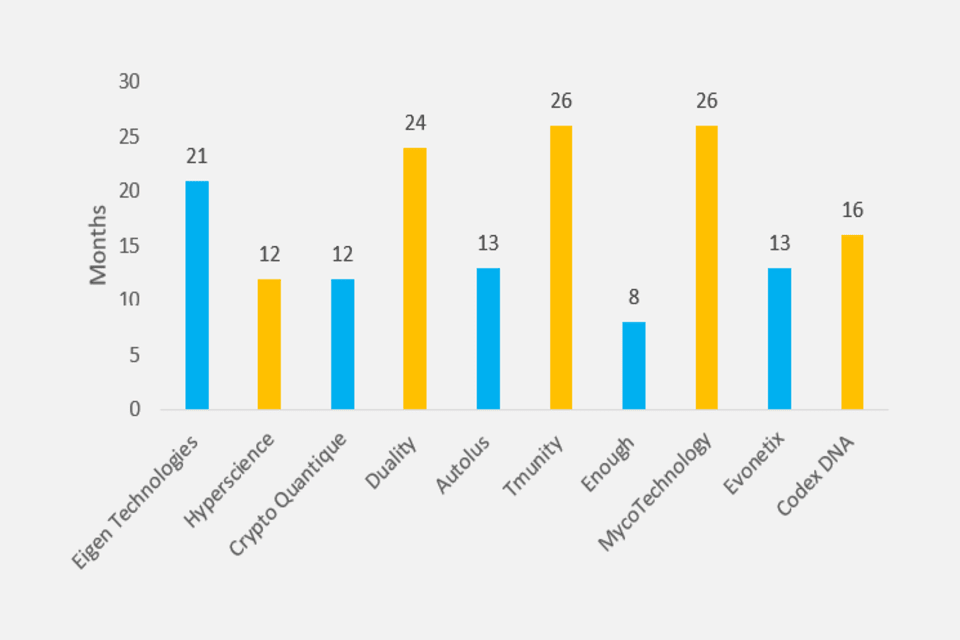

On average, it took UK twins 16 months between their first and second funding rounds. US twins had a similar experience, taking 18 months between first and second rounds.

-

The median deal size for second round funding for US companies was £14 million. UK twins received a third less funding, with a median deal of £10.5 million.

On average, UK twins had to wait 5 months longer between their second and third funding rounds.

- Of the 5 UK twins presented in this analysis, only 3 received a third VC funding round, while 4 of 5

US companies received a third round.

- UK twins had to wait longer than US twins on average (18.5 months versus 13.5 months) between their second and third funding rounds.

Further work could dive deeper to look into US and UK funding comparisons of all the early stage companies in the tech sectors, to gain greater confidence in comparing the UK and the US.

Figure 6: Comparison of investment by UK and US twins. (UK is blue, US is orange)

Figure 7: Comparison of time (months) taken between 1st and 2nd VC funding rounds for UK and US twins. (UK is Green, US is orange)

CST Twins Analysis

’Twins’ case study: Oxbotica versus Aurora

Oxbotica

Founded in 2014. Headquartered in Oxford, United Kingdom.

Oxbotica is an autonomous vehicle software company formed as a spin out from Oxford University’s Mobile Robotics Group by Professor Paul Newman (BP Professor of Information Engineering at University of Oxford) and Professor Ingmar Posner (Professor of Engineering Science, Applied Artificial Intelligence, at the University of Oxford).

To date, Oxbotica has raised a total of $114.5 million over 5 funding rounds.

Their latest funding was raised in April 2021 from a Series B round led by Ocado Group, as part of a partnership on hardware and software interfaces for autonomous vehicles. Those that have invested in Oxbotica typically invest in intellectual property rich, R&D intensive sectors; three of these investors have headquarters outside the UK (Hostplus and Venture Science).

| Date | Funding round | Number of investors | Money raised | Lead investor |

| April 2021 | Series B | 1 | £10 million | Ocado Group |

| December 2020 | Series B | 8 | £38.3 million | BP Ventures |

| June 2019 | Series A | 3 | £12.5 million | IP Group Plc |

| September 2018 | Series A | 3 | £7.7 million | IP Group Plc |

| April 2017 | Grant | 1 | £13.5 million | Innovate UK |

| November 2014 | Seed | 1 | £100k | Oxford University Innovation |

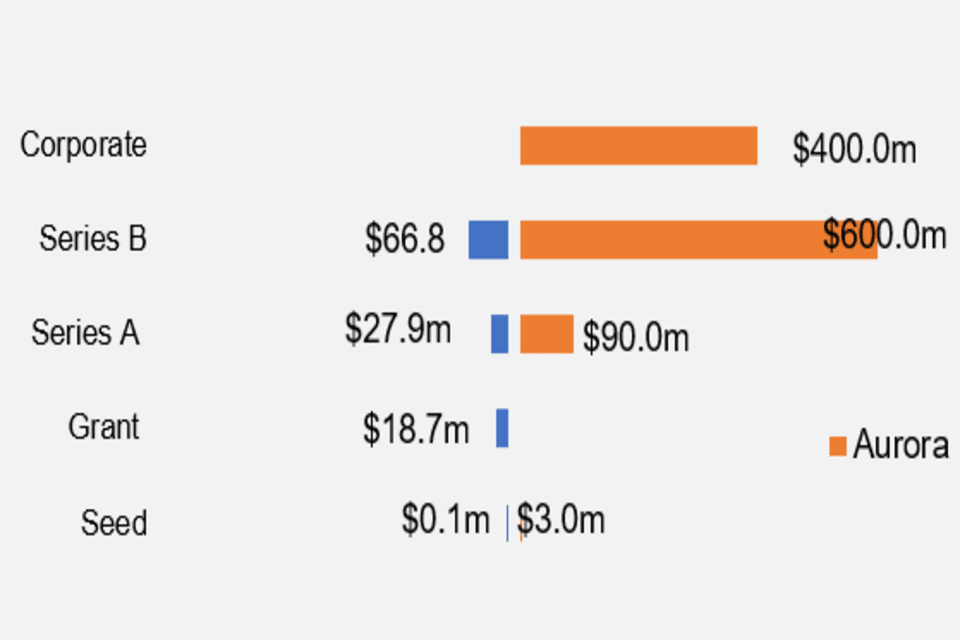

Aurora

Founded in 2016. Headquartered in California, United States.

Aurora is an autonomous vehicle software company founded by Chris Urmson (former Chief Technology Officer of Google’s self-driving car team and technology director for Carnegie Mellon), Sterling Anderson (former Director of Tesla Autopilot), and Drew Bagnell (former autonomy architect at Uber Advance Technology centre).

To date, Aurora has raised a total of $1.1 billion in funding over 5 rounds. Their latest funding was raised in December 2020 from a Corporate Round. Aurora is funded by 15 investors, Uber and Millennium Technology Value Partners are the most recent investors.

Aurora has acquired 3 organisations: Blackmore Sensors and Analytics in May 2019; Uber Advanced Technologies Group in December 2019; and OURS Technology in February 2021. In July 2021, Aurora announced plans to go public and merge with special acquisitions company Reinvent Technology Partners. The deal represents an equity value of $11 billion for Aurora, and the combined company will be valued at $13 billion.

| Date | Funding round | No. of investors | Money raised | Lead investor |

| December 2020 | Corporate | 1 | $400 million | Uber |

| August 2019 | Series B | 1 | - | - |

| July 2019 | Series B | 1 | $70 million (due to limited data this may include funding from August 2019) | Hyundai Motor Group |

| February 2019 | Series B | 13 | $530 million | Sequoia |

| February 2018 | Series A | 2 | $90 million | Greylock, Index Ventures |

| March 2017 | Seed | - | $3 million | - |

Figure 8: Comparison of investment in Aurora and Oxbotica at different funding rounds

Analysing the investment received by both Oxbotica and Aurora in the first five years of being founded highlights significant differences in the scale of investment between the UK and US.

Oxbotica has received substantially smaller rounds of funding compared to Aurora, with greater length of time between investment rounds. Oxbotica has raised a total of $94.7 million through series A and B funding rounds, compared to Aurora which has raised over $1 billion through series A and B funding rounds.

’Twins’ case study: Eigen Technologies cs Hyperscience

Eigen Technologies

Founded in 2015. Headquartered in London, United Kingdom.

Eigen Technologies is a research-driven AI company which specialises in nonperforming loans (NPL) for businesses in finance, law and professional services. The company was founded by Lewis Lui (Physicist and former McKinsey business analyst) and Jonathan Feuer (former managing partner at CBC Capital).

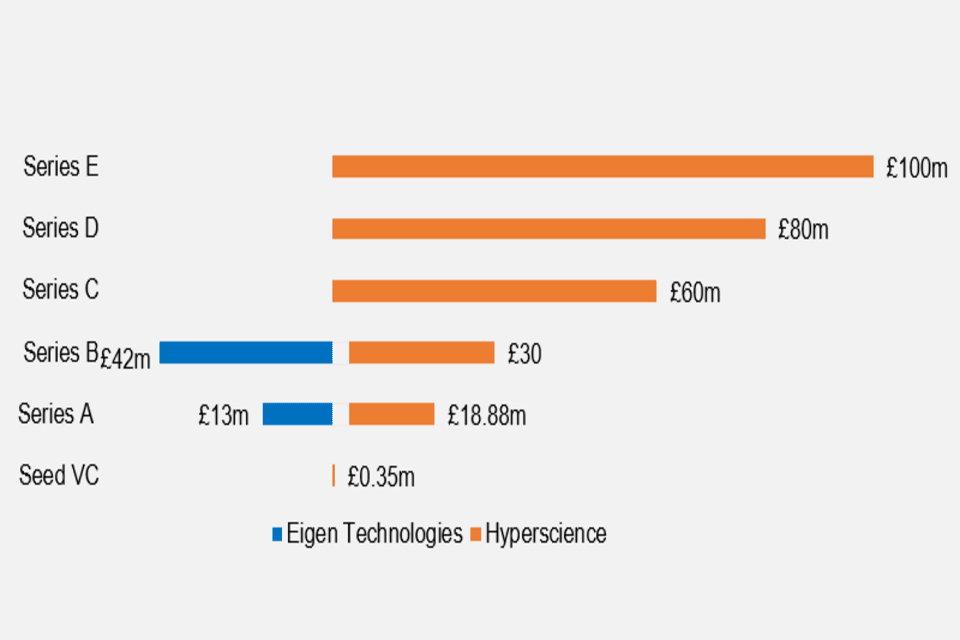

To date, Eigen Technologies has raised a total of £45 million over 2 funding rounds.

Their latest funding was raised in March 2020 from a Series B funding round which was led by Lakestar and Dawn Capital.

| Date | Funding round | Number of investors | Money raised | Lead investor |

| March 2020 | Series B | 1 | $5 million | ING Ventures |

| November 2020 | Series B | 4 | £37 million | Dawn Capital, Lakestars |

| June 2018 | Series A | 2 | $13 million | GS Growth, Temasek Holdings |

Hyperscience

Founded in 2014. Headquartered in New York, United States.

Hyperscience develops AI based enterprise software designed to automate office work processes through using machine learning to streamline complex processes automatically and increase productivity. The company was founded Peter Brodsky (former Director at SoundCloud), Vladimir Tzankov (R&D lead at Instinctiv) and Krasimir Marinov (former Backend Software Engineer).

To date, Hyperscience has raised a total of £289 million over 14 funding rounds.

Their latest funding was raised in January 2022 from a Series E II funding round which was lead by Gaingel.

| Date | Funding round | Number of investors | Money raised | Lead investor |

| January 2022 | Series E II | 1 | - | Gaingel |

| December 2021 | Series E | 1 | £100 million | Bessener Venture Partners |

| December 2020 | Incubator V | 1 | - | Plug and Play Accelerator |

| October 2020 | Series D | 1 | £80 million | Tiger Global Management |

| September 2020 | Incubator IV | 1 | - | Plug and Play Accelerator |

| June 2020 | Series C | 4 | £60 million | Bessener Venture Partners |

| March 2020 | Incubator III | 1 | - | Plug and Play Accelerator |

| February 2020 | Incubator II | 1 | - | Decode Accelerate |

| January 2019 | Incubator | 1 | - | FinTech Innovation Lab |

| January 2019 | Series B | 8 | £30 million | Stripes |

| December 2016 | Series A - III | 2 | £8 million | Felicis Ventures |

| July 2015 | Series A - III | 9 | £880k | - |

| July 2015 | Series A | 7 | £10 million | First Mark |

| December 2014 | Seed VC | 1 | £350k | Slow Ventures |

Figure 9: Comparison of investment in Eigen Technologies & Hyperscience at different funding rounds

Eigen Technologies and Hyperscience raised similar amounts over series A and series B funding rounds. Hyperscience was able to secure a further £240 million through Series C to E funding rounds.

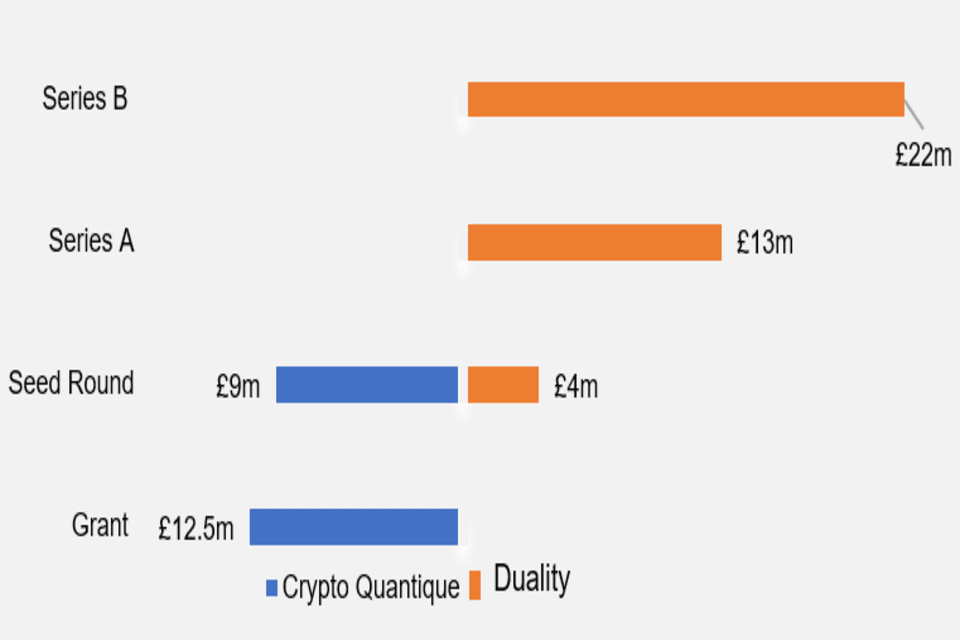

’Twins’ case study: Crypto Quantique vs Duality Technologies

Crypro Quantique

Founded in 2015. Headquartered in London, United Kingdom.

Crypto Quantique focuses on combining quantum technologies with modern cryptography to develop next generation hardware and software products to future proof cyber security solutions. It was co-founded by Dr Shahram Mossayebi PhD in Post Quantum Cryptography from Royal Holloway University) who has published several scientific papers on the security of modern cryptosystems against quantum adversaries and Dr Patrick Camilleri (PhD in microelectronics engineering and complex systems from Otto bon Guericke University) who was formally a Phillips semi-conductor IC designer.

To date, Crypto Quantique has raised £19 million from UK grants and seed funding and a €2.2 million grant from the European Commission.

Their latest funding was raised in September 2019 from a seed funding round led by Entrepreneur First.

| Date | Funding round | Number of investors | Money raised | Lead investor |

| July 2020 | Grant | 1 | £300k | Innvoate UK |

| 2019 | Grant | 1 | €2.2 million | EU Innovation Council |

| September 2019 | Seed Round | 2 | £8 million | Kim Ventures |

| September 2018 | Seed Round | - | £1 million | - |

| September 2016 | Grant | 1 | £10 million | Entrepreneur First |

Duality Technologies

Founded in 2016. Headquartered in New York, United States.

Duality Technologies enables organisations to securely collaborate on sensitive data via operationalising Privacy Enhancing Technologies and enables secure analysis and artificial intelligence (AI) on encrypted data. Dr Alon Kaufman (formally RSA’s global director of Data Science and Innovation founded Duality Technologies) founded the company alongside three individuals with technical science backgrounds (and one former VC general partner who specialises in hi tech companies).

To date, Duality Technologies has raised a total of £39 million in 3 declared funding rounds.

Their latest funding was raised in July 2021 from a Series B funding round led by LG Technology Ventures. All of the investors were based in North America apart from one which was based in Israel.

| Date | Funding round | Number of investors | Money raised | Lead investor |

| September 2021 | Incubator | 1 | - | Plug and Play Accelerator |

| July 2021 | Series B | 7 | £22 million | LG Technology Ventures |

| October 2019 | Series A | 5 | £13 million | Heast Ventures |

| October 2017 | Seed | 1 | £4 million | Team8 |

Figure 10: Comparison of investment in Crypto Quantique and Duality Technologies at different funding rounds.

Crypto Quantique obtained a higher seed funding round compared to Duality Technologies, £9 million and £4 million respectively. Duality Technologies went on to raise a total of £25 million through Series A and Series B funding rounds, whereas Crypto Quantique have not secured any further funding.

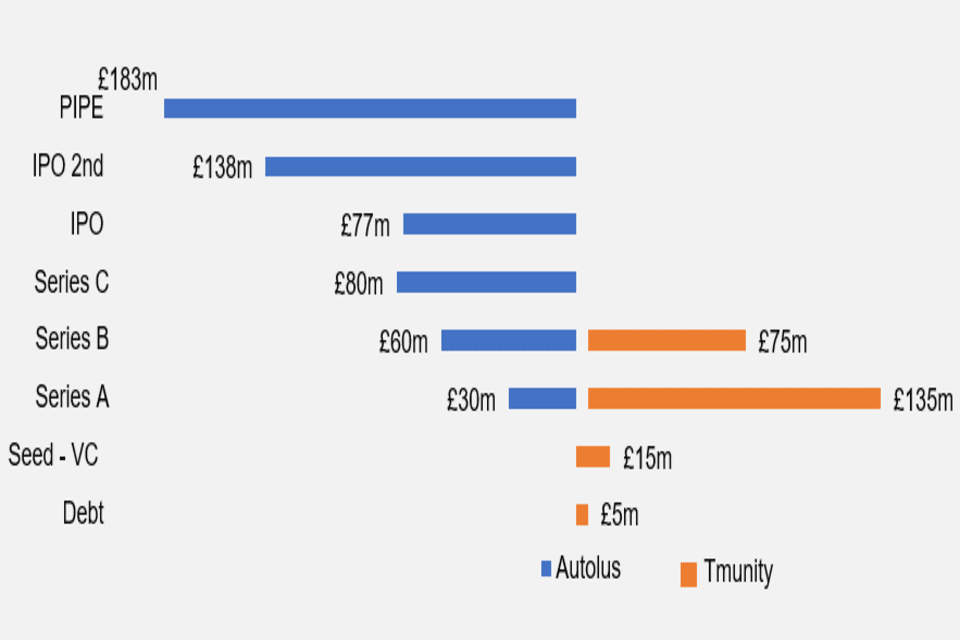

’Twins’ case study: Autolus vs Tmunity

Autolus

Founded in 2014. Headquartered in London, United Kingdom.

Autolus are developing the next generation of CAR-T cell therapies targeting both haematological cancers and solid tumours . Autolus was founded upon the work of Dr Martin Pule (senior haematology lecturer at UCL) and was spun out of University College London in 2014.

To date, Autolus has raised a total of £632 million over 7 funding rounds.

Their latest funding was raised in November 2021 the lead investor was Blackstone Life Sciences Autolus listed on NASDAQ in June 2018.

| Date | Funding round | Number of investors | Money raised | Lead investigator |

| November 2021 | PIPE | 1 | £183 million | Blackstone Life |

| January 2020 | IPO (second) | £61 million | - |

| April 2019 | IPO (second) | - | £77 million | - |

| June 2018 | IPO | £77 million | - |

| September 2017 | Series C | 6 | £80 million | Syncona Partners |

| March 2016 | Series B | 5 | £60 million | Arix Bioscience |

| January 2015 | Series A | 1 | £30 million | Syncona Partners |

Tmunity

Founded in 2015. Headquartered in Philadelphia, United States.

Tmunity Therapeutics are developing novel products which will utilise the immunological potential of T cells to treat a wide range of diseases. The company was founded by Carl June (Professor in Immunotherapy in the Department of Pathology and Laboratory Medicine) and four other individuals who are all professors in biomedical sciences at the University of Pennsylvania.

To date, Tmunity has raised a total of £230 million over 6 funding rounds.

Their latest funding was raised in October 2019 from a Series B funding round.

| Date | Funding round | Number of investors | Money raised | Lead investor |

| October 2019 | Series B | 10 | £75 million | - |

| April 2018 | Series A - II | 4 | £35 million | - |

| March 2018 | Series A | 6 | £100 million | - |

| May 2016 | Seed VC - II | - | £5 million | - |

| December 2016 | Seed VC | 2 | £10 million | - |

| December 2015 | Debt | - | £5 million | - |

Figure 11: Comparison of investment in Autolus and Tmunity at different funding rounds

Analysing the investment received by Tmunity and Autolus over the last 7 years highlights how Autolus raised significantly more overall compared to Tmunity. The life sciences sector was the only sector within our research sample in which the UK company raised more in total than the US equivalent. Autolus went on to obtain a further $80 million through a Series C funding round before listing on NASDAQ in June 2018.

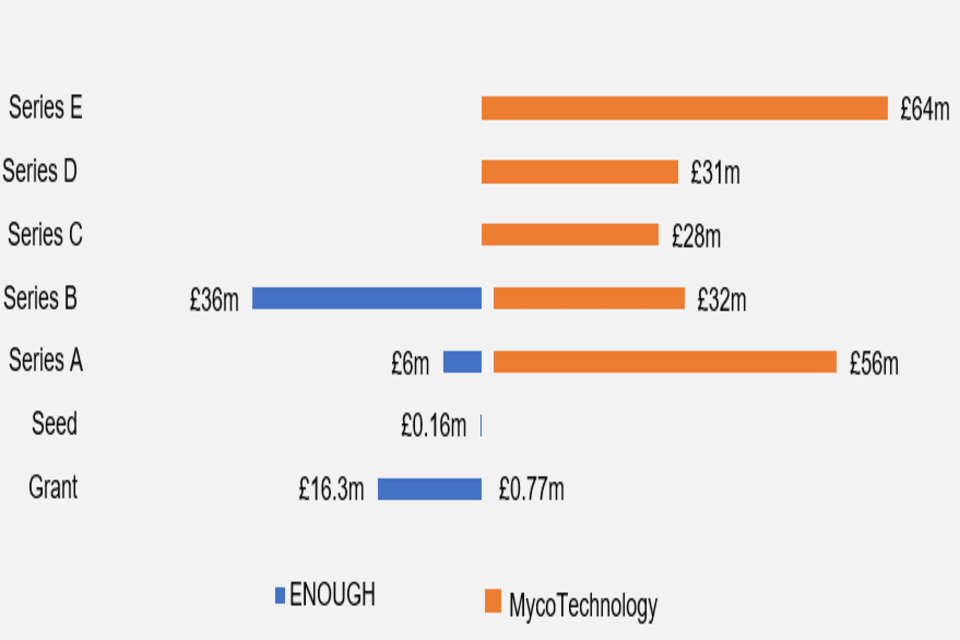

’Twins’ case study: ENOUGH vs MycoTechnology

ENOUGH

Founded in 2015. Headquartered in Glasgow, United Kingdom.

ENOUGH uses the natural process of fermentation to produce mycoproteins for a range of food products such as burgers and noodles. ENOUGH formed as a spinout of Strathclyde University and was founded by three chemical engineers with over 25 years experience in the food industry: Jim Laird (formally Managing Director of Value Creation Partners), David Ritchie (ICI Chemical Engineer), and Craig Johnson (former industry director of CMAC Future Manufacturing Research Hub).

To date ENOUGH have raised £78 million over 3 funding rounds.

Their latest funding was raised in June 2021 from a Series B funding round led by Nutreco and Olympic Investments.

| Date | Funding round | Number of investors | Money raised | Lead investor |

| June 2021 | Series B | 4 | £36 million | Nutreco and Olympic Investments |

| July 2019 | Grant | 1 | £16 million | Horizon 2020 SME Instrument |

| April 2018 | Series A | 3 | £6 million | Scottish Enterprise |

| November 2017 | Grant | 1 | £70k | Innovate UK |

| July 2017 | Seed | 2 | £160k | Scottish Enterprise |

MycoTechnology

Founded in 2013. Headquartered in Great Denver Area, United States.

MycoTechnology is a food ingredient company that uses fungi-based food processing platforms to create novel ingredients such as meat analogue substitutes and fermented protein. Out of the four original founders, Jim Langan and Brooks Kelly (fugus scientist from Pennsylvania State University) have a scientific background and Alan Hahn and Peter Lubar have a background in business working in Silicon Valley.

To date, MycoTechnology have raised $208 million over 6 founding rounds.

Their latest funding was raised in March 2022 from a Series E round led Oman Investment Authority.

| Date | Funding round | Number of investors | Money raised | Lead investor |

| March 2022 | Series E | 14 | £64 million | Oman Investment Authority |

| January 2021 | Series D | 13 | £41 million | Evolution VC |

| November 2020 | Grant | 1 | £770k | Syngenta |

| January 2019 | Series C | 7 | £23 million | Cibus Fund |

| December 2018 | Series C1 | - | £5 million | - |

| October 2017 | Series B | 10 | £32 million | Bunge Ventures |

| July 2015 | Series A | 9 | £56 million | S2G ventures |

Figure 12: Comparison of investment in ENOUGH & MycoTechnology at different funding rounds

ENOUGH received a substantially smaller Series A funding round compared to MycoTechnology who were unsuccessful in securing funding. ENOUGH has raised a total of £42 million through Series A and B funding rounds, compared to MycoTechnology which has raised £88 million through Series A and B funding rounds. MycoTechnology also went on to secure a further £123 m through Series C - E funding rounds.

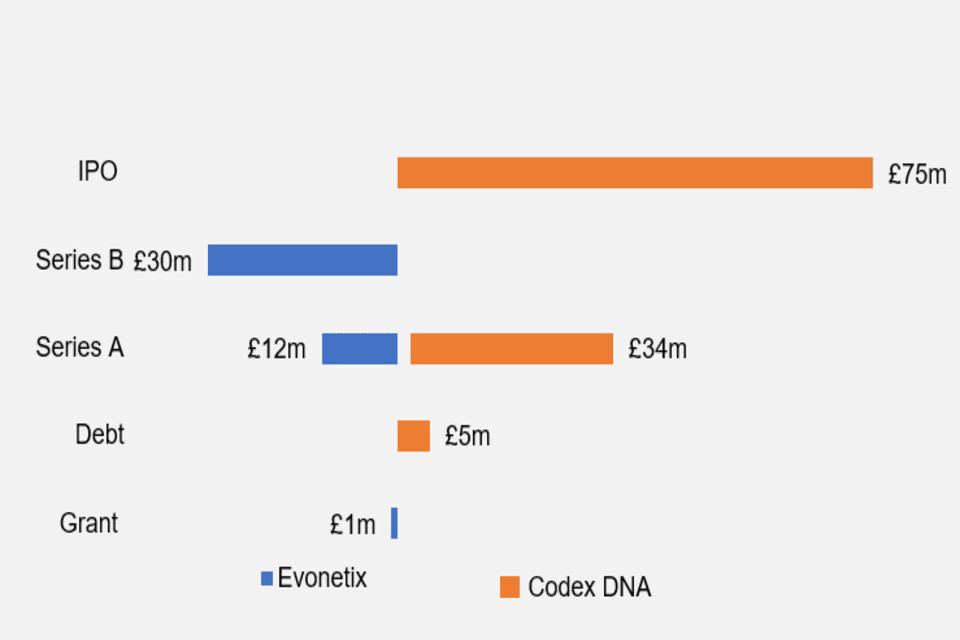

’Twins’ case study: Evonetix vs Codex DNA

Evonetix

Founded in 2015. Headquartered in Cambridge, United Kingdom

Evonetix are developing a desktop DNA synthesis platform which provides the ability to quickly synthesise DNA accurately and at scale. The company was primarily founded by Matthew Hayes (former CTO of the global MedTech division at Cambridge Consultants). The other five members of the founding team also worked at Cambridge Consultants and possess a diverse range of experiences in finance, marketing, comms and business development.

To date, Evonetix has raised a total of £43 million over 3 funding rounds.

Their latest funding was raised in March 2020 from a Series B round led by Foresite Capital, all 3 of the Series A investors also invested at Series B.

| Date | Funding round | Number of investors | Money raised | Lead investor |

| March 2020 | Series B | 9 | £30 million | Foresite Capital |

| July 2018 | Grant | 1 | £1 million | Innovate UK |

| January 2018 | Series A | 3 | £12 million | DCVC & Molten |

Codex DNA

Founded in 2013. Headquartered in San Diego, United States.

Codex DNA provides the tools needed for the designing, coding and creation of synthetic DNA. The company was founded by Todd Nelson (former CEO of Discover X and MP Biomedicals) and Daniel Gibson (Principle Scientist at Synthetic Genomics Inc.).

To date, Codex DNA has raised a total of £114 million over 4 funding rounds.

Their latest VC funding was raised in December 2019 from a Series A funding round, led by the Participation Fund and Northpond Ventures. In June 2021 Codex DNA listed on the NASDAQ stock exchange.

| Date | Funding round | Number of investors | Money raised | Lead investor |

| June 2021 | IPO | - | £75 million | NASDAQ stock exchange |

| March 2021 | Debt | - | £5 million | - |

| December 2019 | Series A - I | 2 | £14 million | Participation Fund & NorthPond Ventures |

| August 2019 | Series A | 3 | £20 million | NorthPond Ventures |

Figure 13: Comparison of investment in Evonetix & Codex DNA at different funding rounds

Codex DNA raised £34 million at series A compared to £12 million by Evonetix. Codex also went on to list on the NASDAQ stock exchange in June 2021.

Annex: Quantitative Analysis Methodology

Company investment data for the analysis of twins funding round was drawn from PitchBookin May 2022. For each twin, data covers funding rounds from their launch up until early 2022 (to note there is a time lag for investment deals to appear on PitchBook).

Only investment deals that are confirmed as being completed, verified, and have a disclosed amount and are included in the analysis. It may be the case that further undisclosed investments were made into the twins.