Market Data Insights - October 2021

Published 11 November 2021

© Crown copyright 2021

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/market-data-insights-october-2021/market-data-insights-october-2021

Economic summary

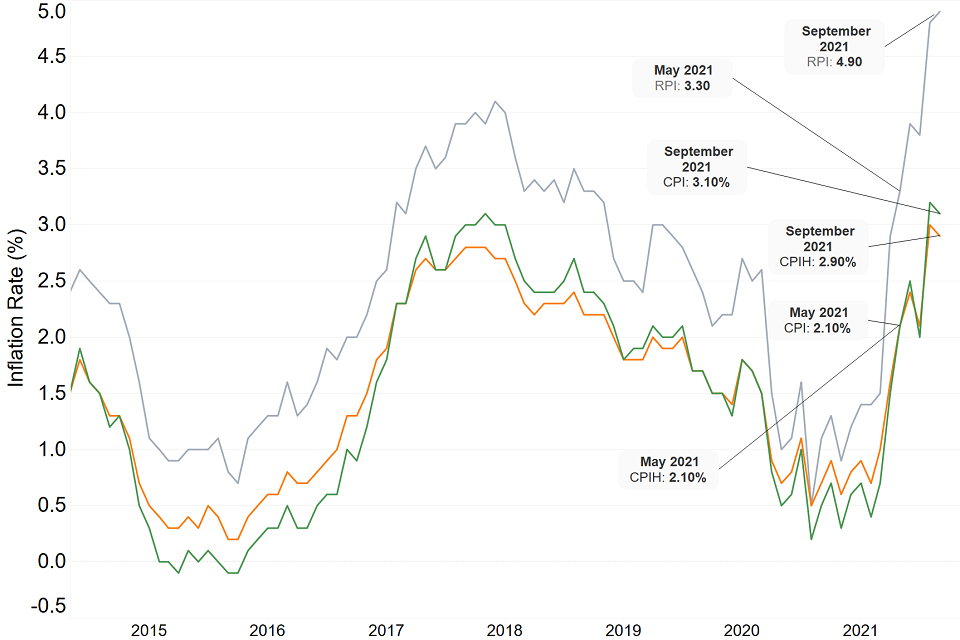

This month, high inflation levels continued to make economic news. The Consumer Prices Index including owner occupiers’ housing costs (CPIH) inflation stayed above the 2% Bank of England target for the fifth consecutive month. It was at 3.0%, the largest level observed since 2012. The Bank of England has forecast inflation will be 5% by April 2022.

The Chancellor unveiled the Autumn Budget this month, which he said was focused on the ‘post-COVID’ era. The Chancellor needed to manage pressures to invest in recovering from the effects of the pandemic with high levels of taxation and government borrowing. Notably, the Chancellor promised to increase spending on skills and training by £3.8bn by 2025 and reduce borrowing from 7.9% of GDP this year to 3.3% next year.

Meanwhile, there were minimal announcements related to climate change and meeting net zero carbon emissions. In November, global leaders will meet at COP26 in Glasgow to discuss how to combat climate change, where more announcements are expected.

October marked the first full month where COVID-19 booster vaccinations were available to eligible people who had their second vaccination over 6 months ago. So far, more than 8 million have received their booster vaccination.

As the UK enters the winter months, virus transmission becomes more prevalent as more spend more time indoors. The 7-day average number of cases stood at 32,013 as at 30 September and rose by 23% to 39,524 by 28 October. The government have not ruled out re-introducing social distancing measures to combat rising case numbers, known as ‘Plan B’.

Inflation

The Consumer Prices Index (CPI) measures the average change in prices over time that consumers pay for a basket of goods and services. CPIH is similar to CPI, in that it also measures inflation, but it also factors in owner occupiers’ housing costs.

The Retail Prices Index (RPI) is an older method of measuring inflation which has a different calculation method to CPI and CPIH. This method has been criticised as being flawed by the UK Statistics Authority and has suggested reforming. The Chancellor has acknowledged this but has ruled out making reforms prior to 2030 as some financial instruments still rely on RPI.

This month, CPIH inflation has surpassed 2% for the fifth month in a row. As a barometer, the Bank of England has a government mandate to set its base rates to target an CPIH inflation rate of 2%.

If this level of inflation is sustained or continues to rise, it might prompt an increase in the base rate. However, increasing base rates is often seen as stifling the economy as it causes borrowing costs to rise, reducing spending and investing.

The Bank of England’s decisions around future base rate changes, will therefore need to balance inflationary pressures against the impact on the UK economy as it attempts to recover from the effects of the pandemic. The Bank of England has not ruled out increasing base rates this year.

Equities

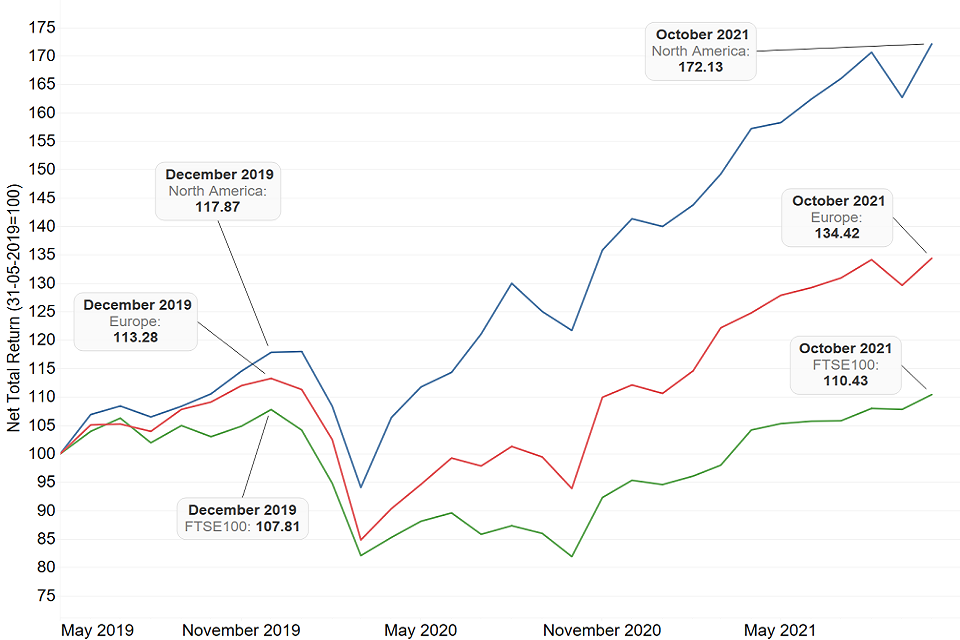

The stock markets across Europe, North America and the FTSE 100 reached a peak in late 2019 prior to the start of the COVID-19 pandemic before reaching a low in March 2020. However, they have shown markedly different recoveries since. The FTSE 100 has surpassed its December 2019 high in September 2021. Comparatively, the North America stocks reached their all-time high in July 2020 and Europe in February 2021 and have shown strong levels of growth since.

The reason for the FTSE 100 underperformance outside of COVID-19, could be explained by the UK’s withdrawal from the EU on 31 January 2020. This withdrawal affected the trade deals the UK had with the EU and the rest of the world. However, since the FTSE 100 is comprised of the performance of the UK’s largest 100 companies by market capitalisation which is a relatively small sample size, it could be influenced by the performance of a few companies.

Furthermore, as the FTSE 100 has a large number of multinational companies whose earnings are in US Dollars, the recent strengthening of the pound may have caused overall earnings to reduce.

Exchange rates

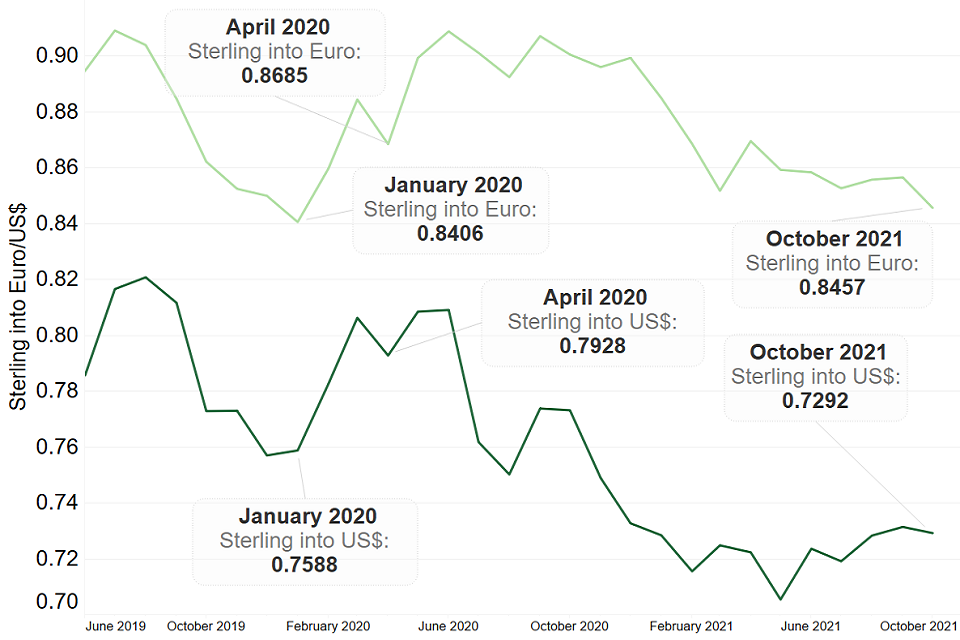

The graph below shows the exchange rate of pound sterling to euro and US Dollar over the past 2 years. Since March 2020, the pound has strengthened against the euro and the US Dollar.

When a domestic currency strengthens, it makes imports cheaper and exports dearer. While exchange rates can be influenced by many factors including interest rates and inflation, the strengthening of sterling could be attributed to the uncertainty around Brexit now no longer being a factor.

However, the pound sterling is currently weaker against the euro than it was prior to the UK withdrawing from the EU on 31 January 2020.

Disclaimer

The information in this publication is not intended to provide specific advice. Please see our full disclaimer for details.

The Government Actuary’s Department is proud to be accredited under the Institute and Faculty of Actuaries’ Quality Assurance Scheme.