No Safe Havens 2019: responding appropriately

Updated 16 May 2019

© Crown copyright 2019

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/no-safe-havens-2019/no-safe-havens-2019-responding-appropriately

Only a minority of our customers pay less than they should and the UK tax gap is at a near record low[footnote 1].

HMRC actively responds where our customers are non-compliant, whether the problem arises within the UK or overseas. We respond robustly where people have sought to avoid or evade tax, or helped others to do so.

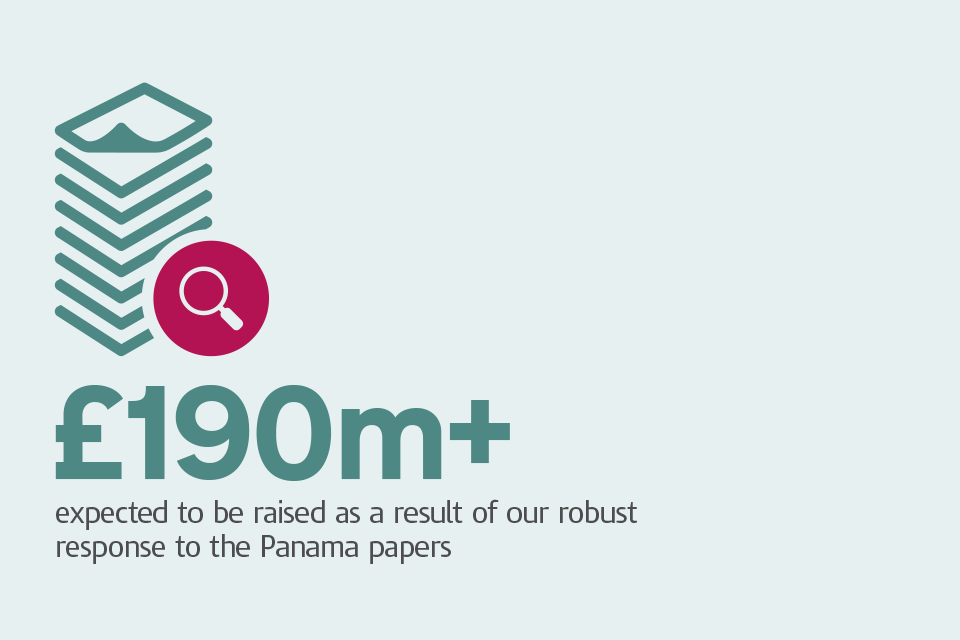

HMRC uses the full range of its criminal and civil powers to investigate fraudsters and to tackle organised crime. As a result of these investigations HMRC has protected £3.3 billion in tax revenues, including both onshore and offshore, in 2017 to 2018 alone. Our current portfolio of civil and criminal investigations resulting from the Panama Papers is forecast to yield over £190 million.

This image shows a graphic with the caption: £190m+ expected to be raised as a result of our robust response to the Panama papers.

The government has introduced extensive new penalties and tough new criminal offences (introduced in 2016 and 2017) for tax evaders and those who help them. This includes new Corporate Criminal Offences for companies that fail to prevent the facilitation of tax evasion, so that we can tackle the problem at all levels. Now, those who are determined to evade are taking bigger risks.

As part of our efforts to ensure that tax paid by multinational companies is commensurate with the activities they undertake in the UK, in 2015 the government introduced the Diverted Profits Tax. By the end of 2017 to 2018 this had delivered £700 million. In addition, HMRC investigations of profit diversion have delivered substantial amounts of additional Corporation Tax and VAT as businesses unwound aggressive structures.

Responding appropriately is the third of our 3 aims, as we understand that customers make mistakes with their tax for various reasons and only a minority seek to deliberately try to avoid or evade tax.

As we respond to those that pay less than they should, as well as those that deliberately enable them to do so, we will make use of all the tools at our disposal. This will allow us to identify risks and behaviours and respond in the most appropriate and proportionate way.

Focus: Connect – HMRC’s analytical tool

Connect cross-references more than 22 billion lines of data including customers’ Self Assessment returns, property and financial data.

Connect identifies more than 500,000 cases (onshore and offshore) for HMRC to enquire into every year.

Use of data to ensure the right tax is paid

HMRC recognises that the majority of customers pay the right tax at the right time and we are committed to helping them do so as easily as possible. However, some make mistakes, or fail to get up-to-date advice and become non-compliant. Others are not aware that they should, for example, account for income from a rental property in another jurisdiction and that UK tax may be due.

Some engage in tax avoidance by seeking to exploit the tax rules to gain an advantage that Parliament never intended. A minority deliberately decide to evade UK tax, for example using offshore structures to hide income that they should have declared.

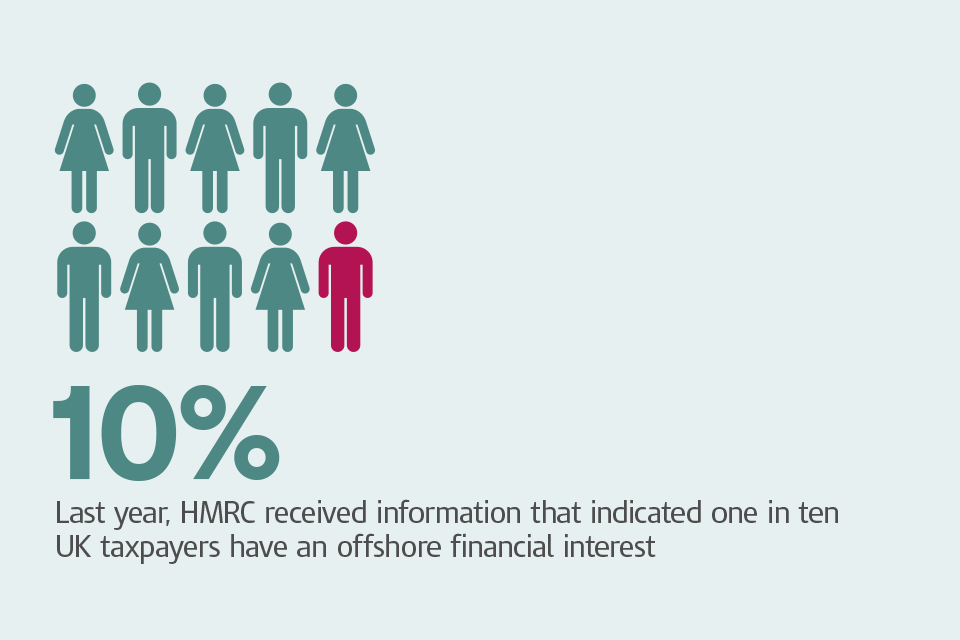

Global implementation of new international tax transparency standards is shedding unprecedented light on HMRC’s customers’ overseas arrangements. For example, early analysis of the information HMRC received last year suggests around one in 10 UK taxpayers have an offshore financial interest.

This image shows a graphic of people with the caption: Last year, HMRC received information that indicated one in 10 UK taxpayers have an offshore financial interest.

HMRC first received data under the Common Reporting Standard in 2017. We have already integrated this data into Connect to help us verify compliance and detect possible non-compliance and have started contacting customers where we believe there is a risk of tax having been underpaid.

We will build on this work over the coming months and years as increasing quantities of data are integrated into Connect and we develop our analytical tools, and gain further insights into risks related to offshore financial accounts.

Case study: HMRC recognises those who choose to voluntarily correct their affairs

Mrs P and her late husband had been using a complex structure to deliberately hide money overseas for many years. However, Mrs P recognised it was only a matter of time before HMRC detected her evasion.

Mrs P came forward to declare her evasion in 2016.

HMRC recognised Mrs P had come forward entirely voluntarily to put it right, and accordingly reduced the penalty from potentially around 100% to 30% of the tax owed. Mrs P also paid substantial interest, as she had been evading tax for many years.

In total, the tax, interest and penalty amounted to £1.2 million – nearly double the tax due had Mrs P paid the correct tax in the first place.

HMRC always recognises voluntary disclosure and will reduce the penalty accordingly. Those who choose not to come forward face higher penalties and, potentially, prosecution.

Correcting inaccuracies

We recognise that the majority of HMRC’s customers seek to pay the correct tax, and we help them to correct mistakes. Helping people get things right helps us too.

Everyone has a responsibility to take reasonable care over their tax affairs. ‘Reasonable care’ means doing everything a person can reasonably do to make sure they comply with the tax rules, for example by ensuring that tax returns and other documents sent to HMRC are accurate.

What is reasonable will differ for each customer according to their abilities and circumstances. If a customer takes reasonable care but despite that gets their tax wrong, then no penalty will be due for that mistake.

Those who have failed to take reasonable care and have understated the tax due will be required to pay the appropriate penalties. These penalties can be reduced if the customer comes forward to correct their mistake and cooperates with HMRC’s enquiries.

A customer who chooses not to come forward and waits for HMRC to identify that they paid less than they should will always be in a worse position than a customer who comes forward voluntarily and cooperates with HMRC’s enquiries.

Finance (No 2) Act 2017 introduced a new Requirement to Correct regarding past tax non-compliance before 1 October 2018 or face greatly increased penalties. Over 18,000 customers have notified HMRC that they want to correct past offshore tax non-compliance.

This image shows a graphic of a bell with the caption: 18,000+ notifications of intent to correct past offshore tax non-compliance received.

We will examine how else to encourage, and help, customers to correct inaccuracies. Using the insight we are gaining from the Requirement to Correct and elsewhere we will be better able to identify risks and spot possible mistakes with customers’ tax affairs as they arise.

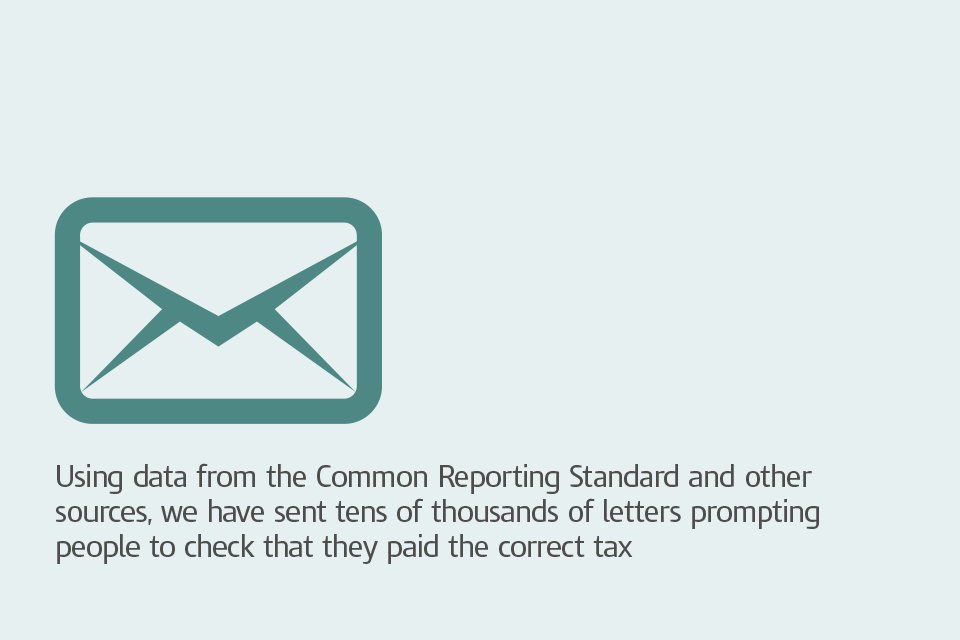

Where we suspect a taxpayer may have made a mistake, we will encourage them to check their tax return is accurate. In 2018, HMRC wrote to tens of thousands of customers we believed may have tax due on an overseas account or investment to ask them to check they had paid the correct tax.

This image shows a graphic with the caption: Using data from the Common Reporting Standard and other sources, we have sent tens of thousands of letters prompting people to check that they paid the correct tax.

Challenging those who try to avoid UK tax

Tax avoidance involves bending the rules of the tax system to gain a tax advantage that Parliament never intended. It often involves contrived, artificial transactions that serve little or no purpose other than to produce this advantage. It involves operating within the letter – but not the spirit – of the law.

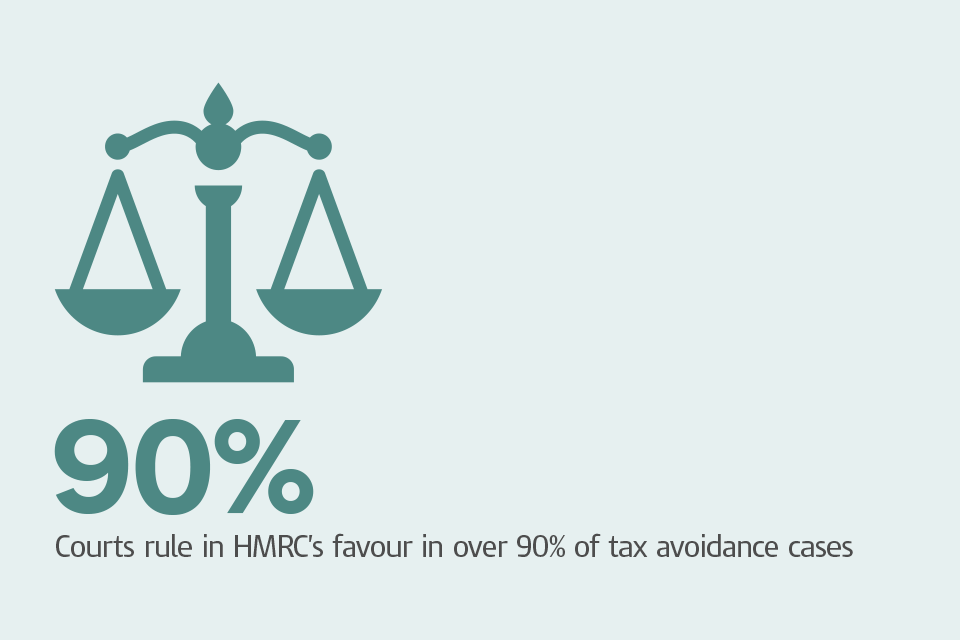

Most tax avoidance schemes simply do not work. We challenge those who try to avoid tax and HMRC wins 9 out of 10 avoidance cases taken to court.

This image shows a graphic of scales with the caption: Courts rule in HMRC’s favour in over 90% of tax avoidance cases.

Those who engage in avoidance can find they pay more than the tax they attempted to save once HMRC has successfully challenged them. Many others choose to settle their dispute without resorting to litigation.

HMRC investigates every customer we suspect may be trying to avoid tax to determine whether a challenge is appropriate. Whether this is a marketed scheme sold to hundreds of people or a ‘bespoke’ scheme devised and implemented by a wealthy individual or a large company, HMRC will investigate it. We work with our partner tax authorities where the tax arrangements involve overseas elements or features.

Where necessary, the government will continue to take action domestically and multilaterally to update the law to reflect modern business practices and close loopholes that exploit offshore structures. This will help ensure the correct UK tax is paid.

We will use targeted communications to customers, and the full range of powers provided by Parliament, to reduce both the number of existing avoidance cases and the appetite for new avoidance schemes.

Recently introduced powers, like Accelerated Payment Notices, are taking the profits out of tax avoidance by ensuring that any tax in dispute is paid up front. Follower Notices are requiring users of similar schemes to settle once HMRC wins a lead case in litigation.

Case study: collaboration across tax authorities

Mr G used an avoidance scheme in an attempt to reduce his tax liability. HMRC identified the scheme, the offshore company involved, and that a small number of UK taxpayers were using the same scheme.

HMRC asked our partner tax authority to provide information on the offshore company. This information exposed a complex web of transactions designed to avoid UK tax liabilities involving several companies across different jurisdictions. In addition, many more UK scheme users were identified.

Working with our partners to address the avoidance scheme will recoup around £100 million in tax for the UK – over 8 times the tax originally estimated.

HMRC will challenge and investigate cases where tax avoidance is identified, working in collaboration with our partner tax authorities where necessary to recover all the tax due. If an avoidance scheme sounds too good to be true, it probably is.

Tackling those who try to evade UK tax

Tax evasion is a crime. Whilst customers’ circumstances will vary, those who misrepresent their affairs, or know they are not paying the right amount of tax and do nothing to correct it, are evading tax. In line with HMRC’s criminal investigation policy[footnote 2] we tackle those who evade tax using the most cost-effective methods to help deliver value for money.

As a result, many that evade tax are subject to civil penalties, including substantial fines.

The government has strengthened HMRC’s civil response to offshore tax evasion in recent years. This includes introducing a new asset-based penalty from April 2016 onwards which can be up to 10% of the value of any asset that underlies the evasion (in addition to the existing penalties that apply). The government has also introduced new specific criminal offences for offshore evasion.

We will continue to undertake criminal investigations where the conduct involved is such that only a criminal sanction is appropriate and where HMRC needs to send a strong deterrent message. Where HMRC’s tax evasion investigations result in prosecution, more than 9 in 10 end in conviction.

This image shows a graphic of handcuffs with the caption: 90%+ investigations wich result in prosecution end in conviction.

New international tax transparency agreements are shedding unprecedented light on our customers’ offshore affairs. This, combined with HMRC’s robust operational approach, will ensure there are no safe havens for those who seek to evade tax.

We will continue to monitor our approach and, where appropriate, will implement reform to help HMRC tackle those who seek to cheat the system.

Case study: HMRC responds robustly to those that don’t co-operate

Mr W owned a small business selling kitchens in the UK. He diverted some of his business’s income to his personal bank account in Spain in an attempt to hide it from HMRC and evade over £277,000 in UK tax.

In line with HMRC’s criminal investigation policy, we initially opened a civil enquiry after our analysis indicated potential discrepancies. However, Mr W still chose not to come forward to declare and pay the tax he owed.

Mr W was given the opportunity to disclose the irregularities and reduce potential penalties, as well as the risk of prosecution, on a number of occasions during HMRC’s investigation, but refused to cooperate.

As a result, HMRC escalated the enquiry by launching a criminal investigation. Mr W was prosecuted for tax fraud.

He now faces a 21 month prison sentence – suspended for 2 years – and if he fails to pay the tax and penalties he owes within 3 months of his conviction, he will go to prison for 5 years.

HMRC will respond robustly where there is less than full cooperation with our enquiries.

Case study: where appropriate, HMRC will not hesitate to open a criminal investigation

Four conspirators devised and marketed a scheme they said would avoid tax by claiming relief on industrial investments. Two hundred and seventy-five clients invested over £78 million in the scheme, and claimed over £100 million in tax relief on the advice of the conspirators.

However, the scheme was a sham. The conspirators only invested £4 million of the £300 million they claimed, the rest was hidden in 24 offshore trusts and companies owned by the conspirators and managed or administered from 4 different jurisdictions.

The conspirators were arrested and HMRC’s criminal investigation, delivered in partnership with other tax authorities, proved they had attempted to cheat the public of revenue through their actions.

As a result, custodial sentences totalling 27 years were handed down and HMRC is recouping the lost public revenue from their clients.

HMRC will not hesitate to open criminal investigations in appropriate cases, where we need to send a strong deterrent message or where the conduct involved is such that only a criminal sanction is appropriate. This can lead to prosecution and, on conviction, to a long prison sentence.

Collecting the tax owed

HMRC takes swift action to collect unpaid tax, interest and penalties, whether the customer resides in the UK or overseas, and wherever their assets are located.

We will support those who try to pay outstanding tax debts. However, if customers choose not to cooperate and will not pay what they legally owe, we will look to collect the debt through formal procedures. Where the customer and their assets are based overseas, we can often work with our partner tax authorities to collect the tax due.

While we have a very high success rate in collecting overdue tax in the UK, this is more difficult for customers outside our jurisdiction – this is the same for all tax authorities. Inevitably, some debt is written off, resulting in a permanent loss of tax to the UK Exchequer and less money to fund public services.

We will consider reforms to prevent the non-payment of UK tax in the first place and will strengthen our collaboration with other tax authorities to help ensure UK tax debts are paid.

We will also explore opportunities to disrupt and deter those who try to not pay the tax they owe, learning from the experience of other jurisdictions.

Case study – it doesn’t pay to delay

Mr Z moved to another country without paying UK tax that he owed and bought a new home to settle there.

HMRC asked the tax authority in that country to pursue the debt on HMRC’s behalf. Mr Z disputed the amount of tax and paid only half what he owed. When the UK court ruled in HMRC’s favour, the overseas tax authority was able to recover the full amount of tax plus interest and late payment penalties.

HMRC will pursue UK tax debt overseas in collaboration with our international partners to ensure those who owe UK tax pay what is due.

Pursuing those who enable tax avoidance and criminality, including tax evasion

An ‘enabler’ is any person who knowingly helps their client to avoid or evade tax. We will strengthen our understanding of enablers as we detect and investigate more of their clients, using the data we are receiving and through our collaboration with our partners in other jurisdictions.

We will relentlessly pursue enablers using the new penalty regime for anyone who designs, sells, or otherwise enables the use of a tax avoidance arrangement which HMRC later defeats. Similarly, we will impose new civil penalties on those who deliberately enable another person’s offshore evasion or non-compliance.

We have already seen behavioural responses to these penalties. Enablers of tax avoidance schemes have chosen to move out of that business altogether, publicly announcing this decision.

In addition, in 2017 the government introduced new Corporate Criminal Offences[footnote 3] for companies and partnerships that fail to prevent the facilitation of tax evasion by those providing services for them, or on their behalf.

As a result of this legislation we have seen organisations strengthening their internal processes to guard against the risk that their representatives may facilitate tax evasion. We will continue to work with organisations to help them prevent facilitation of tax evasion within their ranks.

HMRC is using a new system that collates data on non-compliant enablers across sectors that allows a holistic view across the department. This complements HMRC’s existing tools to identify and assess risk and respond accordingly.

We will continue to build on existing initiatives and operational collaboration as we explore opportunities to deter, disrupt and penalise those who enable their clients to avoid or evade tax, whether they are based in the UK or overseas. This includes working with our international partners to tackle their activities.

We are actively pursuing a number of enablers suspected of facilitating cross-border tax fraud and money laundering through the ‘J5’ alliance.

These joint projects help effectively disrupt the operations of those who enable international tax crime, and often support HMRC’s work to tackle other criminal activities including fraud and money laundering. We will work together with other tax authorities to gather information, share specific operational intelligence and conduct joint operational activity to detect and crack down on those who enable tax avoidance and evasion.

Taking a proportionate response, appropriate to the risk and behaviour, ensures fairness and trust in the tax system, from helping customers understand their tax obligations to robustly tackling those who try to cheat the system. No individual or company is above the law.

Our response will ensure offshore tax compliance and that there are no safe havens for offshore tax avoidance and evasion.

You can read the next section: No Safe Havens 2019: Annex A - glossary.

-

Measuring tax gaps 2018 edition - tax gap estimates for 2016 to 2017, page4. HMRC: 14 June 2018. ↩

-

HMRC’s criminal investigation policy HMRC: updated 4 September 2018. ↩

-

Tackling tax evasion: Government guidance for the corporate offences of failure to prevent the criminal facilitation of tax evasion. HMRC: 1 September 2017, updated 18 May 2018. ↩