OGA annual report and accounts, 2023 to 2024 (accessible webpage)

Updated 30 July 2024

© Crown copyright 2024

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/ogansta-annual-report-and-accounts-2023-to-2024/oga-annual-report-and-accounts-2023-to-2024-accessible-webpage

Accounts presented to Parliament pursuant to Section 6 of the Government Resources and Accounts Act 2000 (Audit of Non-profit Making Companies) Order 2009.

Report presented to Parliament by Command of His Majesty.

Ordered by Parliament to be printed 18th July 2024.

Company number 09666504

HC12

ISBN 978-1-5286-4945-2

CCS E03127497

Chairman’s foreword

Energy has hardly been out of the headlines all year. We all want clean, reliable, and affordable energy supplies; things which are no longer taken for granted. Yet the North Sea with its oil and gas, wind, carbon storage and hydrogen resources, can supply much of the UK’s energy demand while driving the transition to net zero.

Sadly, much of the energy debate has been long on slogans and short on facts. The UK can manage the transition to net zero by 2050 affordably while enhancing energy security and protecting jobs if we do so by combining our natural advantages with consistent, timely and coordinated political and regulatory decision taking.

The North Sea Transition Authority (NSTA) remains resolutely focused on supporting responsible oil and gas production, emissions reduction, and the energy transition.

The NSTA’s team awarded 82 oil and gas licences and approved projects which will reduce our reliance on energy imports, while securing jobs and investment. In the world’s first-ever carbon storage licensing we awarded 21 licences, which are capable of safely storing 30 million tonnes of CO2 a year by 2030. This, in addition to the six licences already in existence, is a significant step on the path to net zero. The NSTA published the OGA Plan which supports industry in its efforts to meet emissions targets.

We pressed for improvements in key areas from Industry. Relevant licence holders must stand by the North Sea Transition Deal commitment to invest £2-3 billion in platform electrification. Decarbonising the power of platforms must happen. No ifs, no buts. Otherwise, the industry will not maintain its social licence to operate.

We were concerned at repeated requests to defer well decommissioning duties and warned that failure to meet licence requirements may well result in financial or other sanctions. We urged businesses to improve their ESG reporting to promote trust and encourage investment in the industry.

The Energy Act 2023 gave us welcome new powers to ensure vital North Sea assets are in the right hands. Companies must now seek our consent ahead of completing a change of control of a licensee or its parent company. It also allows us to require licensees to share valuable information about present and future carbon storage locations, helping identify prime sites.

The Offshore Petroleum Licensing Bill would have required us to hold annual licensing rounds, subject to net zero tests being met. Legislation is a matter for government and the NSTA will, of course, support the policies of the government of the day. However, the NSTA, as an independent arm’s-length body, has held regular licensing rounds since it was formed.

The NSTA takes great pride in adding value for industry and the wider stakeholder community by reducing bureaucracy and harnessing digital solutions which save time and money. This year alone:

-

Decom Data Visibility Dashboards, which give suppliers a clearer picture of upcoming decommissioning activities, now include 15 operators’ decommissioning schedules, up from three previously.

-

We relaunched the Wells Operations Notifications System, which added greater flexibility and improved functionality to processing hundreds of applications for wells activity every year.

-

Supply Chain Action Plans were transferred to an online portal for easier submission and analysis.

-

Our new digital consents system promotes easier submission and monitoring of applications to produce, flare and vent.

-

We unveiled our new website, designed to make it easier for users to find the information they need.

In the boardroom, we were delighted to reappoint Sarah Deasley and Iain Lanaghan to 2026, and Sara Vaughan and Malcolm Brown to 2027. We have a small but effective and committed board and an impressive leadership team very well led by Stuart Payne our Chief Executive.

I was due to stand down as non-executive Chairman in March 2024 after five years but agreed to stay on to give the Secretary of State more time to appoint a successor.

Those five years have seen many external and internal changes. I have been answerable to seven Secretaries of State and six Energy Ministers. Brent crude prices have varied between $20 per barrel and $120, while UK natural gas prices sank to lows of less than 10p per therm and reached highs of around 700p. We have welcomed taking on responsibilities for offshore carbon transportation and storage and hydrogen.

Throughout those external changes and challenges the NSTA teams have retained their professionalism and resilience and shown their ability to adapt and keep producing results throughout Covid and beyond. All our stakeholders owe them a huge debt.

The board reviewed and approved this Annual Report and Accounts on 20 June 2024.

Tim Eggar

Chairman

Chief Executive’s statement

In 2023-24 the NSTA remained strongly focused on supporting UK energy security, reducing emissions, and helping to accelerate the energy transition.

Where there was once just oil and gas, there is now an integrated energy basin in which offshore wind, carbon storage and hydrogen will all grow in importance as the UK strives to reach net zero by 2050.

We know that the UK still needs oil and gas, which meet three quarters of our energy demand and will remain part of our energy mix for decades. As a mature basin, UK North Sea production will continue to decline, and we will continue to be a net importer of oil and gas, but the eight new developments we approved in 2023-24 will bring valuable investment into the basin, support energy security options, and retain the skilled workforce and supply chain needed for the transition.

We recently concluded the 33rd oil and gas licensing round, offering production licences to dozens of companies. It was gratifying to see that there is still real appetite to do business in the North Sea and belief in a important future for oil and gas production. We are currently stewarding 13 projects to production, providing practical support for all stages of the licence lifecycle.

Questions are increasingly asked about the impact on the climate of burning hydrocarbons, and significant progress has been made - with production emissions reduced by nearly a quarter since 2018. But production emissions account for around 3% of total UK emissions, so more needs to be done.

And that is why we have adopted the OGA Plan. It is unashamedly ambitious, and some elements have raised concerns within parts of industry. But I make no apology for that. Decarbonisation is its central aim, and the Plan requires operators to get on low emissions pathways in a number of ways. It places electrification and low carbon power at its heart - power generation is 79% of offshore production emissions - and makes clear that where electrification is reasonable but has not been done, there should be no expectation of accessing future hydrocarbon resources on that asset. Electrification alone could deliver annual carbon savings of up to two million tonnes by 2030.

The Plan highlights three other emission reduction pathways: investment and efficiency, increased scrutiny of assets with high emissions intensity, and zero routine flaring and venting by 2030.

Carbon storage is key to emissions reduction and the energy transition. We awarded 21 licences in the UK’s first carbon storage licensing round and work with the licensees in the existing Track 1 and Track 2 clusters as they move closer to first injection. We have written new guidance to help companies navigate the terrain, opened a consultation on information sharing, and are adapting existing licensing and consents systems to accommodate the new industry.

In September 2023 we became the licensing and consenting authority for offshore hydrogen transport and storage and expect to expand our involvement in this small, but growing, sector.

A smooth and speedy transition is vital for the environment and also for the economy and the tens of thousands of jobs it supports.

The North Sea is becoming crowded, so we liaise with partners to ensure the optimal use of space - oil and gas, carbon storage, offshore wind, and other renewables and traditional industries.

The role of good data and digital tools grows constantly, and we are proud that the National Data Repository now contains more than one petabyte - equivalent to 500 billion pages of standard printed text - of freely available information, and we work with colleagues on the Offshore Energy Digital Strategy Group to make ever more high-quality data available.

At the NSTA our people are our greatest asset. Our core values are to be fair, accountable, considerate, and robust and we live them every day in our interactions with each other and the people we work with outside the NSTA.

We continue to strive to make the NSTA a Great Place To Work, an inclusive organisation that focuses on the wellbeing of all our colleagues. The organisation is fit for purpose and glad to continue to play an important role in shaping the energy future.

Stuart Payne

Chief Executive

Strategic report

Governance

The Oil and Gas Authority (OGA) is a government company whose sole shareholder is the Secretary of State for Energy Security and Net Zero.

On 21st March 2022, the OGA became known by a new business name: North Sea Transition Authority (NSTA) to reflect its evolving role in the energy transition. The OGA remains the legal name of the company.

References to the NSTA should be interpreted as the OGA. The NSTA’s Board of Directors is responsible for setting the authority’s strategic direction, policies and priorities.

The NSTA recovers its costs from a levy on licence holders and via direct fees for specific activities. This is in line with the established ‘user pays’ principle, where the regulator recovers its costs from those benefiting from its services. In addition, it receives some direct funding from its parent department, DESNZ.

The NSTA works closely with industry and governments to attract investment and jobs to retain and develop vital skills and expertise in the United Kingdom.

The NSTA seeks to exercise its powers in a proportionate way to achieve its principal objective of maximising the economic recovery of the UK’s oil and gas resources (MER UK) whilst taking appropriate steps to assist the Secretary of State in meeting the government’s net zero target. The NSTA also regulates the exploration and development of the UK’s onshore oil and gas resources and the UK’s offshore carbon storage, gas storage and offloading activities. It endeavours to do so in a transparent, consistent manner and works with industry to foster a culture where disputes are resolved based on our published prioritisation principles.

The NSTA’s performance against the key performance measures in its 2022-27 Corporate Plan is set out on pages 14 to 22.

The NSTA is headquartered in Aberdeen, with a second office in London.

NSTA role

We regulate and influence the oil, gas, offshore hydrogen and carbon storage industries. We help drive North Sea energy transition, realising the significant potential of the UK Continental Shelf as a critical energy and carbon abatement resource. We hold industry to account on halving upstream emissions by 2030.

Energy security

Helping meet UK energy demand

Oil and gas production, stewardship and storage

Emissions reduction

Regulating for emissions reduction

Driving electrification and zero routine flaring and venting

Accelerating the transition

Carbon storage and offshore hydrogen licensing

Providing open access data

Decommissioning and repurposing

We aim to be an integrating force in the UKCS, helping realise its full economic potential.

We champion the supply chain and job creation across the UK.

NSTA Values

We aim to create a diverse, high-performing team and be a great place to work, where employees are supported to develop their capability, in an organisation with simple processes and systems.

Our values and behaviours are at the heart of everything we do. Created by our people, they guide how we act and how we expect to be treated, providing a sound basis for decisions.

- Accountable: We are reasonable and responsible in exercising our powers and take the appropriate actions to deliver our commitments with pace.

- Fair: In our work we are honest and straightforward. We are open and data-led in our analysis, proportionate and balanced in our decisions.

- Robust: We support security of supply, whilst championing the transition to net zero, holding all parties to account.

- Considerate: We are a respectful and inclusive organisation that supports collaboration. We seek to understand the views of others and engender trust.

UKCS – integrated energy basin

The seas around the UK contain an abundance of opportunity. The real prize is in harnessing these rich resources and infrastructure to deliver an integrated energy basin and a new economic success story. The NSTA is fully committed to enabling the achievement of the UK government’s commitment to reach net zero emissions by 2050.

4.8 billion boe oil & gas

78GT of CO2 storage potential

250TWh blue H2 potential by 2050

50GW offshore wind target by 2030

100+ pipelines with repurposing potential

250+ subsea systems

290+ offshore installations

760+ suspended wells ready for decom

Integrated Energy Basin

The landmark North Sea Transition Deal is an agreement between industry and government to deliver an orderly energy transition. The NSTA is helping deliver on many of the aims of the deal.

£16bn by 2030

Supply decarbonisation:

- Emissions

reduction targets:

- 50% by 2030 as a minimum

- interim targets throughout 2020s

- Methane Reduction Plan

Carbon capture and storage:

- Deploy four clusters by 2030

- Capturing 20-30Mt CO2 by 2030

- New business model for transport and storage

Hydrogen:

- Aim to deliver 10GW Hydrogen by 2030 (4GW Blue, 6GW Green)

- New business models for production, transport and storage

Supply chain transformation - People and skills:

- 50% local content target for all new energy and decommissioning projects

- Develop low carbon industrial capability

Interactive energy map for UKCS

We have worked with The Crown Estate (TCE) and Crown Estate Scotland (CES) to create the app, which, at launch, listed more than 60 in-construction or active wind, wave and tidal sites on the UKCS as well as recently awarded CCS licences and 489 petroleum licences.

The application is automatically updated as each organisation logs new information and is the first time that the locations of all oil and gas and renewables sites have been presented together.

The application shows the proximity of existing oil and gas infrastructure to wind farms, electrical cables and CCS sites, which will assist in gauging the potential for reuse when decommissioning assessments are being made. It has also provided valuable information in prioritising areas for seismic shooting before a wind farm development is built.

Scan to see how it works:

Board of Directors and Company Secretary

- Chairman - Tim Eggar

- Chief Executive - Stuart Payne CBE

- Non-Executive Director - Sara Vaughan

- Non-Executive Director - Malcolm Brown

- Non-Executive Director - Dr Sarah Deasley

- Non-Executive Director - Iain Lanaghan

- Shareholder Representative Director - Fiona Mettam

- Shareholder Representative Director - Vicky Dawe

- Director of Corporate and Chief Financial Officer - Nic Granger

- Company Secretary and General Counsel - Dr Russell Richardson

Leadership team

- Chief Executive - Stuart Payne CBE

- Director of Operations - Tom Wheeler

- Director of Regulation - Jane de Lozey

- Director of Strategy - Hedvig Ljungerud

- Director of Supply Chain and Decommissioning - Pauline Innes

- Director of New Ventures - Andy Brooks

- Director of Corporate and Chief Financial Officer - Nic Granger

- Head of HR - Suzanne Lilley

- Company Secretary and General Counsel - Dr Russell Richardson

Financial overview

Revenue

The NSTA (North Sea Transition Authority) raised levy funding for the year of £35M and fees and charges of £2.6M to cover the core costs of running the organisation. Fees and charges were lower in 2023-24 than 2022-23 because the bulk of fees and charges for the first carbon storage licensing round and the 33rd petroleum licensing round were collected in 2022-23.

As in previous years, where levy funding is unspent it will be returned to licence holders. This year there will be a rebate of approximately £2.7M returned to licence holders through a levy repayment, which has therefore been excluded from the Statement of Comprehensive Income. The NSTA will continue to set the levy in a fair and transparent manner, returning any levy that is not required to the industry each year.

Expenditure

The NSTA financed its core business as well as made significant investment in enhancing digital and data services. Investment was made in developing applications to support UK energy security, drive emissions reduction from UK supplies, and help accelerate the transition to net zero to realise the potential of the North Sea as an integrated energy basin.

Savings were achieved within staff costs due to unfilled vacancies following changes to the organisation structure. Some savings were reinvested in digital projects and the remainder will be returned to industry. In all decisions with a financial impact, the NSTA ensured that best value for money was achieved.

Viability statement

The Directors have assessed the company’s prospects over the 2022-27 Corporate Plan period, taking into account the current financial position, its historical performance, the 2022–27 Corporate Plan and the principal risks and mitigating factors described on page 8. Whilst the principal risks all have the potential to affect future performance, none are considered likely to threaten the viability of the NSTA over the Corporate Plan period. The Board regularly reviews the financial position of the NSTA, including its project funding requirements.

The NSTA has consistently recorded underspends and, with robust financial controls in place, is confident that it will continue to deliver consistent financial outcomes over the Corporate Plan period. The NSTA cash flow is actively managed during the year. The Directors are satisfied that responsibility is delegated systematically in the NSTA, by way of a delegation framework which is regularly reviewed by the Leadership Team. Directors agree that information provided to the Board is concise and clear and can be readily scrutinised.

The NSTA has reviewed its strategic financial framework and is confident that its financial management processes will ensure that its expenditure and liabilities will be covered by its income, as set out in the 2022-27 Corporate Plan. Directors are not aware of any impending regulatory or legal changes which would impact the NSTA’s operations over the period of the Corporate Plan. Based on this review, Directors confirm that they have a reasonable expectation that the NSTA will continue in operation and meet its liabilities as they fall due.

Summary

In summary, the NSTA has used the available funding to deliver value adding activities, ensuring best value for money for both the industry and the Exchequer.

Developing our people

The NSTA has policies in place which ensure its recruitment, performance management, training and reward activity together contribute to making the NSTA a great place to work and mean that the NSTA can attract, develop and retain a talented and diverse workforce to deliver its objectives. The NSTA embraces inclusion and diversity and ensures it promotes equality of opportunity. Our values are at the heart of everything we do. Created by our people, they guide how we act and how we expect to be treated, providing a sound basis for decision making.

The NSTA’s goal is to ensure that these principles, reinforced by the NSTA’s values, are embedded in day-today working practices for all staff, our partners in government and in industry.

The NSTA’s inclusion report forms part of the remuneration and staff report.

Principal risks

| Risk | Mitigation action |

|---|---|

| Uncertain political and economic landscape / attractiveness of the UKCS. | - Enhanced senior engagement with industry and investors. - Engagement plan with MPs and MSPs. - Collaborate with industry and DESNZ to deliver North Sea Transition Deal measures. - Maintain watching brief on ongoing government efficiency and spending review measures |

| Industry / NSTA lose social licence to operate (up to 6bboe production at risk). | - OGA Plan for emissions reductions. - NSTA has set net zero goals for industry: stewarded with Emissions Reduction Plans. - Carbon storage licensing and stewardship programme. - Effective net zero test. Effective use of sanction powers and soft powers, including on corporate governance. - OGA Strategy Judicial Review Judgement strongly supportive of NSTA approach and position. |

| External Risk: Complex regulatory landscape hinders developments and energy integration ambitions. | - NSTA supports DESNZ work on Strategic Spatial Energy Strategy, Offshore Energy Strategy, Offshore Energy Integration Decision Framework. - NSTA represented in Defra Marine Spatial Prioritisation programme. - NSTA inputting to The Crown Estate (TCE) on its Whole of Seabed initiative. - NSTA participates in TCE-chaired offshore wind/CCS co-location forum. - NSTA attends DESNZ-hosted Government and Regulators Electrification Group. - NSTA represented in Scottish National Marine Plan 2 work. - NSTA has become the hydrogen transport and storage regulator. - OPRED net zero work and Gas and Oil New Projects Accelerator (GONPA). - Work with parties on specific conflicts as they arise and offer DESNZ technical and commercial input should any conflict require ministerial views. |

Environment report

Implementing its refreshed policy for 2023-24, the NSTA continues to focus on the Environment, Social and Governance (ESG) aspects of its internal activities and on its approach to meeting Greening Government Commitments (GGC).

The NSTA undertook the following activities in 2023-24:

| Environment | Social | Governance |

|---|---|---|

| - Integrated a CO2 emissions display into the travel booking portal, allowing staff to see the environmental impact of their journeys and make informed choices. - Optimised transportation choices for staff, comparing CO2 emissions against similar-sized businesses. - Commenced development of systems and digitised manual processes to reduce paper usage and work more efficiently. - Replaced outdated monitors with more energy-efficient models to minimize plastic waste and conserve energy, while ensuring proper disposal of the old monitors. |

- Teams engaged in volunteering initiatives to support various charitable causes. - Launched an Energy Education Alliance conjunction with industry and Skills Development Scotland to widen narrative around the energy sector. |

In addition to the governance disclosures in this annual report and accounts: - Reported and satisfied Greening Government Commitments. - Reviewing procurement processes an documents to incorporate sustainability policies. |

The NSTA’s operational activities in 2023-24 produced 269.88 tonnes of carbon dioxide equivalent (tCO2e), with business travel accounting for the largest proportion.

Annual Greenhouse Emission By Activity Type (% of Total)*

*Water and waste emissions are too low to be visible on chart.

Total emissions from business travel nearly doubled to 203.13 tCO2e as travel has continued to increase following the pandemic. The total kilometres travelled by air increased significantly more than by rail, with commensurate increases in CO2 emissions.

The NSTA’s total carbon emissions from electricity increased marginally by 2.54 tCO2e and 6.49 tCO2e for gas consumption as staff have returned to the office.

Data for the Aberdeen and London offices are provided by building facilities management and are estimated based on the floorspace occupied.

Electricity

Waste

Gas

Travel

Year on Year Carbon Emissions

The chart above indicates that carbon emissions have increased with headcount, except during the financial years 2020/21 and 2021/22, which were affected by COVID-19 travel restrictions. However, the NSTA is committed to reducing overall emissions, and a downward trend in emissions per headcount has been observed since 2018/19 through to 2023/24.

Year on Year Analysis

| Activity | 2019-20 | 2020-21 | 2021-22 | 2022-23 | 2023-24 |

|---|---|---|---|---|---|

| tCO2e | tCO2e | tCO2e | tCO2e | tCO2e | |

| Electricity | 38.22 | 26.03 | 27.22 | 27.53 | 30.08 |

| Gas | 11.50 | 24.33 | 25.38 | 30.10 | 36.59 |

| Water | 0.29 | 0.14 | 0.13 | 3.53 | 0.03 |

| General waste | 0.06 | 0.03 | 0.09 | 0.11 | 0.03 |

| Recycled waste | 0.06 | 0.02 | 0.03 | 0.06 | 0.03 |

| Shred-it recycled | 0.12 | 0.05 | 0.08 | 0.01 | 0.01 |

| Flights | 158.87 | 0.63 | 47.08 | 68.85 | 194.95 |

| Rail | 4.25 | 0.05 | 1.70 | 35.24 | 8.18 |

| Total | 213.37 | 51.28 | 101.71 | 165.42 | 269.88 |

Breakdown of annual greenhouse gas emissions by activity type for 2023-24

Electricity (kWh)

| Activity | Units | tCO2e | % of total |

|---|---|---|---|

| Aberdeen | 113,930 | ||

| London | 31,316 | ||

| Total | 145,246 | 30.08 | 11.14 |

Gas (m3)

| Activity | Units | tCO2e | % of total |

|---|---|---|---|

| Aberdeen | 5,166 | ||

| London | 13,128 | ||

| Total | 18,294 | 36.59 | 13.56 |

Water (m2)

| Activity | Units | tCO2e | % of total |

|---|---|---|---|

| Aberdeen | Not metered | ||

| London | 145 | ||

| Total | 145 | 0.03 | 0.01 |

General Waste (kg)

| Activity | Units | tCO2e | % of total |

|---|---|---|---|

| General waste | |||

| Aberdeen | 946 | ||

| London | 267 | ||

| Sub-total | 1,212 | 0.03 | |

| Recycled waste | |||

| Aberdeen | 860 | ||

| London | 577 | ||

| Sub-total | 1,437 | 0.03 | |

| Shred-It recycling | |||

| Aberdeen | 375 | ||

| London | |||

| Sub-total | 375 | 0.01 | |

| Total waste | 3,025 | 0.06 | 0.02 |

| Travel (km) | |||

| Flight | 715,206 | 194.95 | |

| Rail | 230,547 | 8.18 | |

| Total travel | 945,756 | 203.13 | 75.27% |

| Total | 269.88 | 100% |

Signed for and on behalf of the Board

Stuart Payne

Chief Executive

12 July 2024

Accountability report

Key Performance Indicators

In May 2022, the NSTA published an updated ‘NSTA Corporate Plan 2022-2027’, which provides a clear operational framework and identifies the key performance indicators that will be used to benchmark both them NSTA and industry, measure success and hold industry to account. 2023 was the first year in which the NSTA could report quantitatively on progress for the full calendar year 2022. 2024 reporting allows the NSTA to identify and report trends and progress from full calendar years 2022 and 2023 against these published KPIs.

Of particular note:

Emissions Targets

UKCS upstream emissions of greenhouse gases (GHG) fell by 27% between 2018 and 2022. This decline also signifies that industry currently exceeds the target of reducing emissions by 25%. However, industry needs to continue with further emissions reduction measures to meet the 2030 target.

Carbon Capture and Storage (CCS)

In 2023 the NSTA exceeded its aim to award 3-5 licences by awarding 22 carbon storage licences, which have all been accepted and fully executed.

Data

The full year 2023 represents a 1020% increase in the amount of data publicly available for download measured against the 2021 baseline and representing a 240% increase measured against 2022.

2022 Key Performance Indicators: 2024 updates (arrows denote direction of travel)

Energy

| KPI Area | Key Performance Indicator | April 2024 update | RAG | Direction of travel |

|---|---|---|---|---|

| Stewardship | 1. Zero routine flaring and venting by 2030. | The average proportion of routine flaring in 2022 was 47%, reducing to 45% in 2023. Routine venting decreased from 50% in 2022 to 41% in 2023*. | Amber: Behind target 10 – 20% | Up |

| Stewardship | 2. Maintain average UKCS production efficiency at 80%. | 2023 UKCS Economic production Efficiency dropped by 1 percentage point from 2022, to 77%. This was driven by a 9% fall in economic maximum production potential and an 11% fall in actual production. |

Green: On target +/- 10% | Down |

| Stewardship | 3. 10% reduction in the cost of decommissioning between 2023 and 2028 (from £37bn to £33.3bn, from an updated 2022 baseline). | The 2024 forecast cost estimate of decommissioning is £40bn (in 2021 prices) – which is an 8% increase since 2022, reflecting the extremely challenging and unpredictable year for the economy, coupled with global competition for decommissioning equipment and resources. | Red: Behind target >20% | Down |

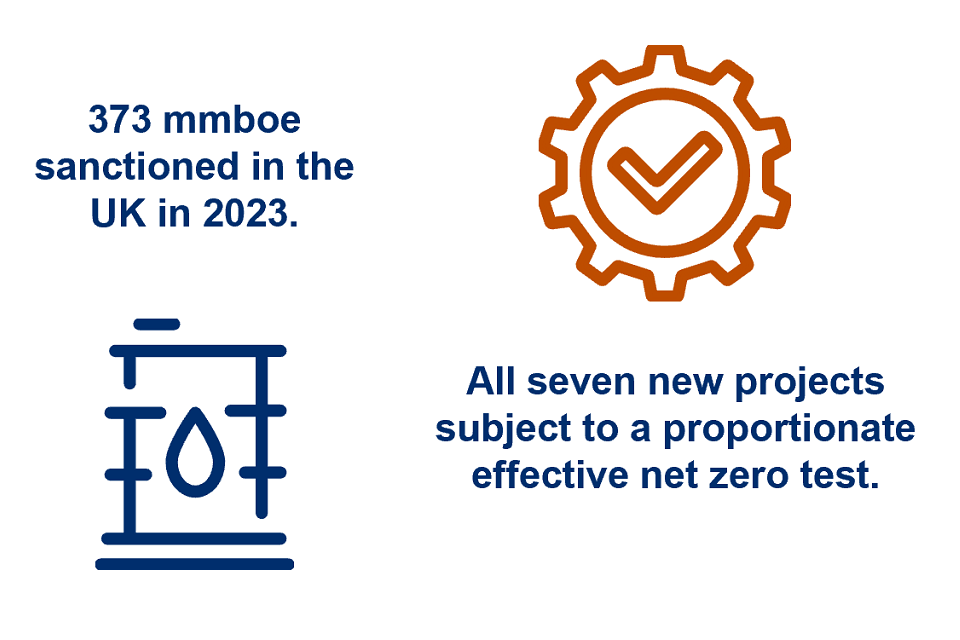

| Meeting demand / security of supply | 4. Optimise UKCS production within the effective net zero test. | Seven projects were sanctioned in the UKCS in 2023. All seven were subject to a proportionate effective net zero test. They total 373 mmboe UK potential production, and incremental UK ‘life of field’ emissions (Mid/P50 Case) of 3,607 KtCO2e - giving an average production GHG emissions intensity of 9.8 kgCO2e/boe - significantly below the 2022 offshore average of 23 kgCO2e/boe. |

Green: On target +/- 10% | Up |

*Updated and revised figures for 2022 may not match previously published figures:

- Data is received annually in September.

- Previous figures for 2022 were based on the 9 months to Sept 2022 - now updated to include 12 months.

- Figures for 2023 based on 9 months to Sept 2023.

Transition

| KPI Area | Key Performance Indicator | April 2024 update | RAG | Direction of travel |

|---|---|---|---|---|

| Emissions targets | 5. As a minimum, reduce UKCS upstream greenhouse gas emissions by 50% by 2030*, 10% by 2025, and 25% by 2027. |

UKCS upstream emissions of GHGs fell by 27% between 2018 and 2022 ** Full data for 2023 has not yet been released but is expected to show a continued decline as indicated by a ~3% fall in CO2 emissions recorded by the Environmental Emissions Monitoring System (EEMS) *** . |

Green: On target +/- 10% | Up |

| Energy integration | 6. At least two electrification projects to be commissioned by 2027. | Currently the NSTA is monitoring three projects which are progressing well but with challenging timescales expected. One project is progressing frontend engineering (FEED) with a view to project sanction in 2024 and two multiplatform projects should reach concept select in 2024, then will progress to FEED. A key developer has bid in CFD Auction Round six, which was an essential enabling step for a windbased electrification project. | Amber: Behind target 10 – 20% | Up |

| CCS | 7. To support ambition of capturing 20-30 million tonnes of CO2 per year by 2030.The NSTA will aim to award two licences in 2022, 3-5 in 2023, and 10+ by 2025.*** | In 2023 the NSTA awarded 22 carbon storage licences, which have all been accepted and fully executed. These new licences are now being stewarded through their work programme and licence obligations. The UK now has a total of 27 Carbon Storage licences, the largest portfolio in Europe. |

Green: On target +/- 10% | Up |

*Emissions targets include all greenhouse gases emitted from offshore production facilities, onshore terminals, drilling rigs and associated logistics.

**Current estimate based on revised and updated NAEI 2022 data. Full details will be published in the 2024 Emissions Monitoring Report.

**Note this is from EEMS - previous updates have referenced ETS which is not received, as yet.

***This target will remain under re-evaluation as existing carbon storage projects develop; however, it is already clear that the scale and pace of activity will need to increase in order to meet the UK’s long-term domestic net zero targets.

Value

| KPI Area | Key Performance Indicator | April 2024 update | RAG | Direction of travel |

|---|---|---|---|---|

| Supply Chain | 8. Evidence of meeting North Sea Transition Deal content commitments for Net Zero and decommissioning projects. | From data exported from approved Decommissioning SCAPs detailing open contracts awarded in the business year 1st April 2023 to 31st March 2024, the NSTA estimates that 95% of the value of these contracts awarded were to UK based organisations, exceeding the target of 50% agreed as part of the North Sea Transition Deal. Actual expenditure from 2023 UKSS data shows UK supply chain accounts for 93% of overall abandonment expenditure (AbEx) global spend, which ties with SCAPs data. Developers have commenced the SCAP process for the first contracts now being placed from the track 1 CCUS projects and early indications show encouraging levels of local content. |

Green: On target +/- 10% | Up |

| Investment, efficiency, jobs | 9. Compliance with environmental, social and governance reporting standards. | Analysis as part of the ESG Disclosure Report 2023 identified that five companies, out of the 29 companies involved, demonstrated ESG disclosure that the NSTA considered to be lagging behind expectations. ESG Stewardship will be undertaken with these companies and others, over the course of 2024. The NSTA has reviewed 20 companies’ governance, relating to a range of matters, such as, licence assignment and change of control over the course of 2023. |

Green: On target +/- 10% | Up |

| Digital/ technology | 10. Increasing volume of data available from the Digital Energy Platform | From January to end December 2023, 549 Terabytes (TB) of well and seismic data was loaded onto the National Data Repository, 602 TB of this data is publicly available to download. The full year 2023 represents a 1020% increase in the amount of data publicly available for download, measured against the 2021 baseline, and representing a 240% increase measured against 2022. During the year, data held in the National Data Repository increased by 136% to 1.07 petabytes. |

Green: On target +/- 10% | Up |

| Digital/ technology | 11. Successful technology development /deployment case studies. | During 2023, the NSTA tracked the successful deployment of 14 technologies within the UKCS, compared with 12 technologies deployed in 2022. The deployments fall into four distinct categories: Well P&A, Reservoir & well management, Facilities management & Well drilling & construction, plus two cross cutting categories, Net Zero and Digital & Data. Deployments in Net Zero were the most abundant throughout the year, with five examples recorded. |

Green: On target +/- 10% | Up |

*There is no data as yet.

Corporate

| KPI Area | Key Performance Indicator | April 2024 update | RAG | Direction of travel |

|---|---|---|---|---|

| Great Place to Work | 12. Sustain staff engagement at 70% or above as measured by the bi-annual NSTA staff survey. | The 2023 NSTA staff survey showed an overall engagement score of 67%, representing an 8% decrease from 2021 and 3 percentage points below target. In each HSE wellbeing survey conducted in 2020 to 2022 overall, the NSTA has scored above the HSE benchmark and the 75th percentile when introduced in 2022. The next staff survey will take place in 2025. | Green: On target +/- 10% | Down |

| Digital Excellence | 13. Delivery of internal Digital Excellence programme of developments. | A five year roadmap to modernise the UK Energy Portal began in April 2023. In 2023 the new service for Supply Chain Action Plans (SCAP) went live, CCS enhancements were made to the Well Operations and Notifications System (WONS) and Pipeline Works Authorisation service, while a key data warehouse milestone was achieved with the full deployment of WONS data. | Green: On target +/- 10% | Up |

2022 Key Performance Indicators: 2024 updates in charts

Energy

1. Stewardship: Routine Flaring & Venting

2. Stewardship: Production Efficiency

3. Stewardship: Decommissioning Cost

4. Security of Supply: Optimize Production

Transition

5. Emissions: Reduce Upstream Emissions

6. Energy Integration: Electrification

7. Carbon Storage: Licences

Value

8. Supply Chain: Local Content

9. ESG: Reporting Standards

10. Digital/ Technology: Data Availability

11. Digital/ Technology: Technology Deployment

Corporate / Organisational

12. Great Place to Work: Staff Engagement

13. Digital Excellence: Programme of Developments

Success Stories Dashboard

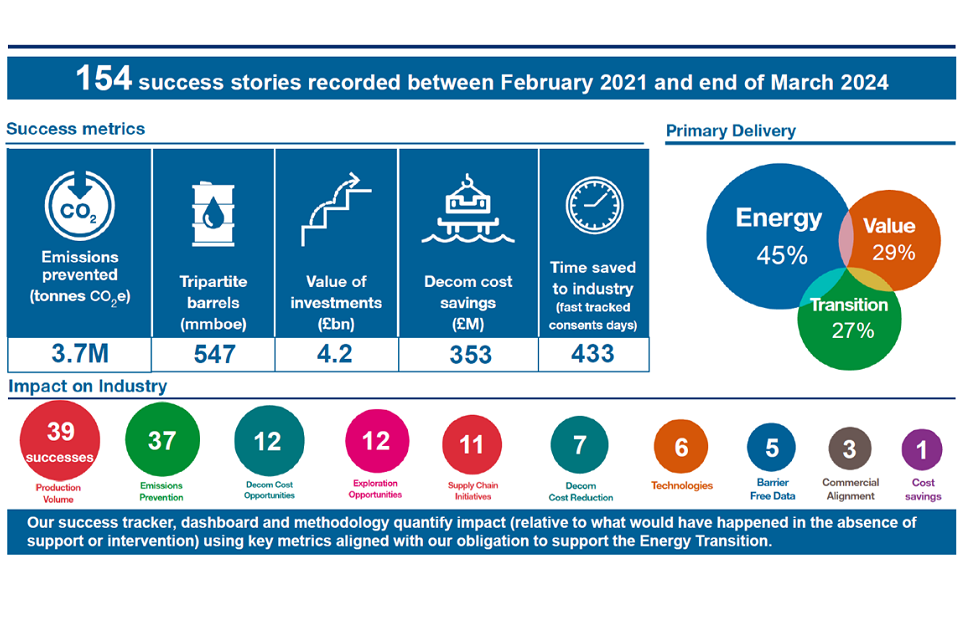

The NSTA continues to measure success through the use of a success stories tracker which allows the impact of the NSTA to be identified and quantified using key metrics.

These metrics include expected future volume of oil and gas production, capital expenditure committed to new projects, reduced or avoided costs through improved or accelerated outputs and greenhouse gas emissions prevented through proactive NSTA intervention.

Infographic: text

154 success stories recorded between February 2021 and end of March 2024*

Success metrics:

- emissions prevented (tonnes CO2e) - 3.7M

- tripartite barrels (mmboe) - 547

- value of investments (£bn) - 4.2

- decom cost savings (£m) - 353

- time saved to industry (fast tracked consents days) - 433

Primary delivery:

- energy 45%

- value 29%

- transition 27%

Impact on industry:

- production volume: 39 successes

- emissions prevention - 37

- decom cost opportunities - 12

- exploration opportunities - 12

- supply chain initiatives - 11

- decom cost reduction - 7

- technologies - 6

- barrier free data - 5

- commercial alignment - 3

- cost savings - 1

Our success tracker, dashboard and methodology quantify impact (relative to what would have happened in the absence of support or intervention) using key metrics aligned with our obligation to support the energy transition.

*The Success Stories Dashboard format was updated in February 2021 to reflect the Strategy.

NSTA Project Summary: 2022

In progress (rescheduled) - 14 (22%)

Complete - 43 (67%)

Proceeding to plan in 2024 - 7 (11%)

Commentary

As of January 1st, 2023, the NSTA commenced tracking a total of 53 high level projects. This represented a slight increase compared to the 50 projects defined in early 2022.

Throughout 2023, 14 additional priority projects were identified within the NSTA and accommodated into the project schedule.

2023 closed out with 67% of projects proceeding to plan.

Parliamentary accountability and audit report

Regularity of Expenditure (audited)

No special payments have been made which exceed £300,000.

No material gifts have been made by the NSTA.

The Trust Statement incurred losses in 2023-2024, see Note 8 Financial instruments for more information. No individual losses have been incurred in excess of £300,000*.

*The Managing Public Money threshold mandated for financial statements prepared under the government financial reporting manual.

| 2023-24 Number of cases | 2023-24 total value (£’000) | 2022-23 Number of cases | 2022-23 total value (£’000) | |

|---|---|---|---|---|

| Trust Statement Debts written off | 1 | 242 | 3 | 489 |

Fees and charges disclosures (audited)

The NSTA, as a Public Sector Information Holder, has complied with the cost allocation and charging requirements set out in HM Treasury and the Office of Public Sector Information guidance.

Analysis (see Note 3.a) disclosed for fees and charges includes:

- i. the financial objective(s) and performance against the financial objective(s)

- ii. the full cost and unit costs charged in year

- iii. the total income received in year

- iv. the nature/extent of any subsidies or overcharging

In line with its statutory function, the NSTA does not seek to make a profit from its charges but merely to recover costs in carrying out its functions. All payers of the levy will receive a proportionate rebate of any surplus.

Remote contingent liabilities (audited)

The NSTA is not exposed to any remote contingent liabilities.

Directors’ report

Directors hereby present their annual report on the company together with the audited accounts for the company for the year ended 31 March 2024. The corporate governance report forms part of the Directors’ report. The Directors’ report is followed by the internal auditor’s opinion, the remuneration and staff report, the auditor’s report and the company’s financial statements for the year from 1 April 2023 to 31 March 2024.

The Directors of the company who were in office during the year and up to the date of signing the financial statements are listed on page 34.

No Director has had any material interest in any contractual agreement, other than an employment contract, which is or may be significant to the company.

When making decisions, Directors have regard to their duties as Directors, including their broad duty under section 172 of the Companies Act 2006 to consider the views of relevant stakeholders.

Directors agree that data and information provided to the Board is accurate, presented clearly and concisely and can be readily scrutinised. The Board invites industry and regulatory experts to present at Board stakeholder meetings and at its annual strategy meeting with the Leadership Team.

Directors recognise the importance of meeting staff outside the Board and Committee cycle. A majority of Directors attended the 2023 and 2024 all staff meetings. The Board periodically invites staff to informal lunches coinciding with Board meetings and periodically invites members of the extended leadership team to Board meetings to present and discuss the key challenges they are tackling.

Directors appreciate the considerable contribution of its skilled, experienced and committed staff in delivering the company’s objectives and functions and Directors take care to consider the impact on staff of the decisions it takes. The NSTA is a fair and considerate employer which offers flexible and hybrid working arrangements and recognises the value of a workforce from diverse backgrounds.

The NSTA provides access to a broad range of training opportunities and encourages career, leadership and personal development, including through mentoring. All applications for employment are treated equally and are fully considered. A code of conduct and related policies are in place and are available to all staff on the NSTA intranet.

The company encourages open and honest communication between employees and senior management. An Employee Engagement Forum offers a structured opportunity for staff to contribute ideas and share their views. Regular company briefings, spanning both offices, provide a further opportunity for staff to raise questions and concerns.

The bi-annual staff engagement survey was run in autumn 2023. In response to survey feedback and subsequent discussions within Directorates, the leadership team committed to further improving leadership capability and to enhance career development and learning opportunities. The leadership team also heightened its focus on values and behaviours, resulting in a new Positive Behaviours at Work Policy, to supplement the Code of Conduct.

The NSTA publishes a large volume of data on its website and is working to transform the collection, storage, analysis and publication of UKCS data across the oil and gas, carbon storage and hydrogen industries. The data team seeks customer feedback on the discoverability and usability of its data and insights. Industry and staff feedback informed the 2023 redesign of the NSTA website.

The NSTA is committed to minimising its own impact on the environment and launched its sustainability strategy in 2021. The company presents its environment report on pages 10-13.

The company made no charitable donations during the year. NSTA staff raised money in raffles to support a number of local charities.

Directors are satisfied that the company engages constructively with its suppliers and that it settles all payments in accordance with contractual obligations.

The company has prepared its 2023-24 financial statements in accordance with UK adopted International Financial Reporting Standards (IFRS). The audited financial statements for the year ended 31 March 2024 are set out on pages 51 to 85.

The NSTA is a not-for-profit company largely funded by an annual levy on industry and fees. Additional interim grant-in-aid funding is provided by its shareholder. Any surplus operational levy funding is returned to levy payers. This refund is recognised in the financial statements.

The NSTA had 225 employees on 31 March 2024 (including secondees and executive directors, but excluding interim contractors and non-executive directors). There were three interim contractors as at 31 March 2024.

The financial results for the period reflect a neutral profit position.

Directors’ third-party indemnity provisions

Directors have been provided with an indemnity against liability in respect of proceedings brought by third parties, subject to the conditions set out in the Companies Act 2006. Such third-party indemnity remains in force as at the date of approving this Directors’ report.

Going concern statement

The Directors have a reasonable expectation that the company has adequate resources to continue as a going concern for a period of at least twelve months from when the company financial statements have been authorised for issue, and therefore they have been prepared on a going concern basis. The basis of this view is outlined in more detail in note 2.3 to the financial statements.

The Directors have assessed the company’s prospects and are satisfied that the company’s financial arrangements minimise the risk of the company being unable to meet its liabilities.

Furthermore, the Directors do not envisage any changes to the current regulatory and legal regime which would adversely affect the operation of the company within the next twelve months.

Directors’ responsibility statement

The Directors are responsible for preparing the Strategic Report, Directors’ Report and the financial statements in accordance with applicable law and regulation.

Company law requires the Directors to prepare financial statements for each financial year. Under that law the directors have prepared the financial statements in accordance with UK adopted International Accounting Standards.

Directors are satisfied that the financial statements give a true and fair view of the state of affairs of the company and of the income and expenditure of the company for the year.

In particular, directors are satisfied that:

i. the company’s accounting policies are reasonable and have been applied correctly.

ii. judgements taken and accounting estimates are reasonable and prudent.

iii. applicable IFRS standards have been followed and any material departures have been disclosed and explained in the company financial statements.

iv. the financial statements have been prepared on a going concern basis.

v. the company has taken reasonable steps to prevent and detect fraud and other irregularities.

vi. adequate accounting records have been kept so as to demonstrate that the financial statements comply with IFRS and Companies Act 2006 requirements, as applicable.

vii. Directors consider that the annual report and financial statements, taken as a whole, are fair, balanced and understandable and provide the information necessary for the shareholder to assess the company’s position, performance, business model and strategy.

Principal risks

Directors carefully consider the way the company manages and mitigates the risks which could adversely impact the company’s ability to deliver its principal objective. The NSTA’s principal risks are set out on page 8 above.

Auditor

Directors are not aware of any relevant audit information of which the auditor is unaware when giving its opinion on the accounts.

In line with the Government Resources and Accounts Act 2000 (Audit of Non-Profit Making Companies) Order 2009, the Comptroller and Auditor General has been appointed as the company’s auditor.

Directors reviewed the effectiveness of the external auditor. No non-audit services were provided by the external auditor.

By order of the Board

Dr. Russell Richardson

Company Secretary

12 July 2024

Corporate Governance Report

The North Sea Transition Authority (NSTA) is the business name of the Oil and Gas Authority (OGA), a company registered in England and Wales with registered number 09666504. The company has one shareholder, the Secretary of State for Energy Security and Net Zero, as a Corporation Sole. The OGA remains the legal name of the company.

References to the NSTA should be interpreted as the OGA, and references to the OGA include the NSTA.

The NSTA’s Chief Executive is also the Accounting Officer, accountable to Parliament for the performance of the NSTA. The role of Accounting Officer is delegated by the Principal Accounting Officer of the Department for Energy Security and Net Zero (DESNZ), the DESNZ Permanent Secretary.

The NSTA’s principal objective is to maximise the economic recovery of petroleum from the UK Continental Shelf whilst assisting the Secretary of State in meeting the UK government’s net zero greenhouse gas emissions target. The NSTA encourages and supports industry in identifying and taking the steps necessary to reduce its greenhouse gas emissions as far as is reasonable in the circumstances.

The company’s primary constitutional document is its Articles of Association. In addition, there is a Framework Document - supplemented by a Finance Letter and a Chairman’s Letter - which sets out the NSTA’s financial and performance accountabilities to Parliament and to its shareholder, the Secretary of State of DESNZ. A revised Framework Document was published in early 2023. The NSTA is classified by government as a Non-Departmental Public Body (NDPB), sponsored by DESNZ.

The second review of the NSTA was undertaken by DESNZ in 2022 and the review report was published on 22 June 2023. All the recommendations of the review report have been implemented.

Board practice

Directors are collectively responsible for the overall strategic direction of the company and for monitoring its performance. Strategic discussions form a significant part of every Board meeting and the Board sets aside a day every year to meet offsite with the Leadership Team to review the strategic direction of the NSTA.

The NSTA recognises the value of good corporate governance and complies with all applicable principles of the Code of Good Practice for Corporate Governance in Public Bodies and the UK Corporate Governance Code.

The NSTA has set out the powers which are reserved to Directors and those which have been delegated to management

Matters reserved to the Board are:

- approving the NSTA’s corporate plan, long-term objectives and overall strategic policy framework

- approving the NSTA’s annual budget and overall financial policy

- approving the NSTA’s annual report and accounts

- undertaking a formal regular review of the Board’s own performance and that of Board Committees. Approving the terms of reference of Board Committees

- making sanction and third-party access decisions. The powers delegated to management are detailed in a Delegation Framework, which is available to all staff on the NSTA’s management system and is regularly reviewed and updated

The Board met eight times in 2023-24. Seven Board meetings are scheduled for 2024-25. The Chairman periodically meets Non-executive Directors independently of the Executive Directors.

Board composition

The Secretary of State invited Tim Eggar to serve a further six months as Chairman of the NSTA to allow sufficient time for his successor to be selected. Tim Eggar agreed to remain as Chairman.

The Board reappointed Sarah Deasley to September 2026, Iain Lanaghan until April 2026 and Sara Vaughan and Malcolm Brown until September 2027.

The Board considers Tim Eggar, Iain Lanaghan, Sarah Deasley, Malcolm Brown and Sara Vaughan to be independent Directors.

Induction of Directors

Directors receive a tailored induction to the NSTA and its broader context, including a programme of meetings with executive directors, heads of teams and senior industry leaders. The Company Secretary briefs directors on their legal duties both as company directors and board members of a public body.

Directors receive appropriate guidance on matters of corporate governance and have full and open access to the company secretary, professional advisers and senior managers for information or advice when required, including access to appropriate training opportunities.

The Board Secretary notifies Directors by email between meetings of NSTA announcements, press releases and significant developments.

Board committees

The Board has three permanent committees: Audit and Risk, Remuneration and Nomination.

The Audit and Risk Committee reviews and monitors the company’s financial accounting, reporting and control processes. It takes assurance on the company’s financial statements, the internal auditor and the effectiveness of management’s actions to identify and mitigate strategic risks. It scrutinises the independence and effectiveness of the external auditor. Cyber security and data protection are standing agenda items.

The Audit and Risk Committee is chaired by Iain Lanaghan and met three times in 2023-24.

Iain Lanaghan, Sarah Deasley, Sara Vaughan and Malcolm Brown were committee members during the year.

The Audit and Risk Committee reviewed the external and internal audit plans and reports, took assurance on the NSTA’s financial statements, financial management, and management of strategic risks. The ARC received assurance on management’s actions to defend the NSTA against fraud and cyber attack.

The Nomination Committee reviews the size, composition and effectiveness of the Board and its Committees and ensures that the Board has the necessary breadth of skills, knowledge and experience to execute its duties. The Committee recommends appointable candidates for Board approval and appointment.

The Nomination Committee is chaired by Tim Eggar. Tim Eggar, Iain Lanaghan, Sarah Deasley, Malcolm Brown and Sara Vaughan were committee members during the financial year. The Nomination Committee met once in 2023-24, to discuss the re-appointment of Sara Vaughan, Iain Lanaghan and Malcolm Brown. Sarah Deasley’s reappointment was agreed in March 2023.

The Remuneration Committee reviews and recommends to the Board the framework and policy for the remuneration of Executive Directors and senior management, and for implementing the Directors’ Remuneration policy.

The Remuneration Committee is chaired by Tim Eggar. Tim Eggar, Iain Lanaghan, Sarah Deasley, Sara Vaughan and Malcolm Brown were committee members during the financial year.

The Remuneration Committee met four times in 2023-24. It reviewed 2023-24 performance management outcomes and approved annual bonuses; it reviewed and approved 2023-24 pay awards and 2024-25 objectives setting; it reviewed the Chief Executive’s 2023 performance and reviewed and approved his 2024 objectives.

Board performance review

The Board reviews its effectiveness every year using a questionnaire, with the Chairman discussing the results with Directors individually and as a group at the May Board meeting. Every three years the Board commissions an external performance review. An external Board performance review had been anticipated in spring 2024 however, as a new Chairman had been expected to be joining the Board at that time, the Board decided to postpone the external review until spring 2025 and to instead proceed with an internal review in 2024. The Board noted that the incoming Chairman, who is expected to be in post by October 2024, may wish to bring forward the external performance review.

In spring 2024, the Board Secretary led the internal Board performance review. Directors completed a questionnaire to evaluate the effectiveness of the Board and its Committees and the Chairman assessed the performance of individual Directors.

The Senior Independent Director led the annual appraisal of the Chairman. The Chairman discussed the outcomes one to one with Directors followed by a discussion at the May Board meeting.

Directors concluded that the Board continues to operate effectively, led by a Chairman who fosters robust and open debate. All Directors contribute fully to Board discussions and they agreed that the Board is strongly supported. The Board will in the coming months consider the delineation of roles between non-executive and executive directors to ensure that the balance is correct. Non-executive directors in particular find site visits with industry very beneficial and the Board agreed that additional meetings would be added to the Board calendar.

Declaration of Directors’ financial interests

In accordance with the NSTA’s conflict of interest policy, Directors must declare any financial interests which may, or may be perceived to, influence their judgment in performing their duties as Directors of the NSTA. This is done on appointment and annually. Directors are further asked to declare any conflicts of interest at the start of each board meeting. If a Director declares a conflict of interest with any agenda item, they will not participate in the discussion of that item.

The Board does not consider the interests held by Tim Eggar, Iain Lanaghan and Sarah Deasley, as declared below, to be sufficiently significant to impair their independent judgement in Board discussions. The Board does not consider that any decision within the NSTA’s powers could materially impact the value of their shareholdings. Directors’ declared interests are shown below.

| Director | Date first advised Board Secretary | Nature of interest | Total value (£) at 31 March 2024 |

|---|---|---|---|

| Tim Eggar | 6 March 2019 | 140,511 equity shares MyCelx Technologies Corporation | 73,066 |

| Family member holdings: 4,099 BP ordinary shares | 20,331 | ||

| 1,875 Shell ordinary shares | 49,219 | ||

| Iain Lanaghan | 21 April 2020 | 1,017 BP ordinary shares | 5,044 |

| 358 Shell ordinary shares | 9,398 | ||

| 9 April 2024 | 450 SSE ordinary shares | 7,425 | |

| Sarah Deasley | 12 April 2024 | 8,999 BEPC (Brookfield Renewable COR-A) shares | 175,146 |

| Family member holding: 597.5 BEPC (Brookfield Renewable COR-A) shares | 11,629 |

Sarah Deasley declared her and her family member’s holdings in BEPC after the NSTA revised its conflict of interest policy to reflect its expanded remit. It is a requirement of Sarah’s BEPC Directorship that she builds up a financial stake in the company to a pre-agreed level within a five-year period from joining the Board.

Iain Lanaghan disclosed his SSE holding after the NSTA revised its conflict of interest policy to reflect its extended remit.

Malcolm Brown’s investments are held in managed funds over which he has no control. Sara Vaughan, Stuart Payne and Nic Granger submitted nil returns.

Fiona Mettam and Vicky Dawe submitted a nil return to DESNZ.

Directors’ other directorships and offices

| Member | Remunerated activities | Non-remunerated activities | Memberships of professional bodies | |

|---|---|---|---|---|

| Tim Eggar | - Chairman, Raw Charging Group Limited (until 14 March 2024). - Chairman of Haulfryn Holdings Limited; Director of its subsidiary Haulfryn Limited; Director of Haulfryn Limited’s subsidiary Lleyn Estates Limited. - Chairman of Suffolk Street Holdings Limited; Director of its subsidiary Haulfryn Group Limited. - Director, The Gipsy Hill Brewing Company Limited. |

- Strategic Advisory Board, Braemar. - Energy Ventures. |

||

| Stuart Payne | - Director, Energy Transition Zone Limited. - Chairman, The Brightside Trust. - Advisory Board member, Barnardo’s Scotland. |

- Fellow, Energy Institute (FEI). - Fellow of the Chartered Institute of Personnel & Development. - Associate Fellow of the British Psychological Society. |

||

| Iain Lanaghan | - Lead Non-executive Director, The UK Supreme Court. - Non-executive Board Member and Audit Chair, Scottish Water (owned by the Scottish Government) and two subsidiaries. - Non-Executive Director and Audit Committee Chairman of UK Government Defence Equipment and Support Agency (DE&S), an Arms’ Length Body of the Ministry of Defence (until 30 June 2023). - Occasional consultancy as Iain M. Lanaghan. |

Institute of Chartered Accountants of Scotland. | ||

| Sarah Deasley | - Executive Director, Frontier Economics. - Independent Director, Brookfield Renewable (Brookfield Renewable BEP and BEPC and two Bermuda Holding Entities: BRP Bermuda GP Limited and Brookfield Renewable Investments Limited). - Director of Brookfield BRP Holdings (Canada) Inc. (from 3 May 2024). |

- Trustee, Sustainability First. - Advisory Board, Carbon Connect. |

||

| Sara Vaughan | - Chair, Elexon Limited and the Balancing and Settlement Code (BSC) Panel. - Director, Poolserco Limited* (until 30 May 2023). - Director, BSC CO Limited. - Director, Poolit Limited (until 30 May 2023). - Director, EMR Settlement Limited. - Director, Elexon Clear Limited. - Co-chair of Icebreaker One’s Steering Group on Open Energy (as consultant). * A subsidiary of Elexon Limited. |

Member of Energy Advisory Panel and Energy Policy Debates Committee, Energy Institute. | - Member of The Law Society. - Fellow, Energy Institute. |

|

| Malcolm Brown | - Chair, Imperial College Trust. - Chair of the Development Committee, Geological Society. |

- The Geological Society of London. - Energy Exploration Society of Great Britain. |

||

| Nic Granger | - Trustee, Falklands Conservation (UK) - Member of the Risk, Audit and Finance Committee and the Data Management Committee, BCS (Chartered Institute for IT). |

- Institute of Chartered Accountants in England and Wales. - The Chartered Institute of Public Finance and Accountancy. - Institute of Directors (until December 2023). - BCS (Chartered Institute for IT). |

||

| Fiona Mettam | - | - | - | - |

| Vicky Dawe | - | - | - | - |

Directors’ dates of appointment

At the end of the reporting year, and at the date of signing, the company had nine Directors, as follows.

| Name | Date of appointment |

|---|---|

| Tim Eggar | 6 March 2019 |

| Nic Granger | 2 November 2016 |

| Iain Lanaghan | 20 April 2020 |

| Sarah Deasley | 1 October 2020 |

| Malcolm Brown | 1 October 2021 |

| Sara Vaughan | 1 October 2021 |

| Fiona Mettam* | 3 November 2021 |

| Vicky Dawe* | 11 July 2022 |

| Stuart Payne | 1 January 2023 |

*Only one of the two Alternate Shareholder Directors attends Board and Committee meetings.

Directors – attendance at Board meetings and Committees

| Board | Audit and Risk Committee | Nomination Committee | Remuneration Committee | |

|---|---|---|---|---|

| Total meetings 2023-24 | 8 | 3 | 1 | 4 |

| Tim Eggar | 8 | - | 1 | 4 |

| Stuart Payne | 8 | 3 | - | 4* |

| Nic Granger | 8 | 3 | - | - |

| Iain Lanaghan | 8 | 3 | 1 | 4 |

| Sarah Deasley | 8 | 2(3) | 1 | 4 |

| Malcolm Brown | 8 | 2(3)** | 1 | 4 |

| Sara Vaughan | 8 | 3 | 1 | 4 |

| Fiona Mettam / Vicky Dawe*** | 8 | 2(3)***** | 1 | 4 |

Numbers in brackets denote the number of meetings held during a Director’s Board or Committee tenure.

*The Remuneration Committee invites Stuart Payne to attend meetings meetings to present evidence in support of Committee decisions.

**Malcolm Brown’s absence was due to ill health. He reviewed the Committee papers before the meeting and provided comments to the Committee Chairman.

***Only one of the two Alternate Shareholder Directors attends Board and Committee meetings.

*****A senior DESNZ official represented the Shareholder Director at one Audit and Risk Committee meeting.

Staff policies

The NSTA periodically reviews its Code of Conduct, which sets out the obligations and responsibilities of staff and Directors, including under Statute.

Quality assurance of analytical models

The NSTA has appropriate Quality Assurance (QA) procedures in place for modelling and analysis purposes which are subject to active monitoring. The arrangements are compliant with Aqua Book guidance and adhere to the principles of proportionality and risk with an emphasis on business-critical models.

Government functional standards for arm’s length bodies

The NSTA was compliant with the mandatory elements of all applicable government functional standards in 2023-24. With the introduction of new Procurement Regulations due on 1st October 2024, functional standards will be reviewed and aligned with the regulations during 2024 and 2025.

Declaration of staff financial interests

The NSTA identified no new material conflicts of interest following the annual declaration by staff and Board Directors of any financial interests in oil and gas, carbon capture or offshore energy or related supply chain companies.

Fraud and whistleblowing

The Chief Digital and Information Officer chairs the NSTA’s Security Advisory Board. The Information Security Manager produces dashboard reports for the Security Advisory Board and the Audit and Risk Committee. The NSTA’s Security Operations Centre monitors cyber security and fraud threats. Staff undertake mandatory online fraud prevention training.

During the financial year no concerns were raised under the raising concerns at work (whistleblowing) policy. The NSTA has four whistleblowing officers.

Data protection

The NSTA’s Data Protection Officer monitors the NSTA’s compliance with data protection law. Staff are required to undertake annual Security and Data Protection online training. In 2023 the NSTA reported a data breach to the Information Commissioner’s Office (ICO). The ICO confirmed that it was satisfied with the actions the NSTA had taken in response to the breach and closed the case.

Risk management

Directors have delegated the regular review of management’s handling of the company’s strategic risks to the Audit and Risk Committee. The NSTA maintains a strategic risk register which lists the principal external and internal risks facing the company, including those identified and escalated from within the organisation and those identified by the Leadership Team or by the Board or one of its Committees.

All risks in the strategic risk register have a named leadership team risk owner. All risks have mitigation measures in place to reduce the potential impact to an acceptable level, wherever possible.

Material changes to the risks, including any new or escalated risks, are reviewed quarterly by the Leadership Team. The Audit and Risk Committee takes assurance on management’s handling of strategic risks three times a year.

The Board reviews strategic risks, from a ‘clean sheet’ perspective, once a year. In 2023-24, the Board reviewed strategic risks in November 2023 and continues to monitor them closely.

The Chief Executive and the Leadership Team continue to foster a strong culture of risk awareness and risk management in the organisation. The principal risks identified by the NSTA are detailed on pages 8-9.

Internal auditor’s statement

Public Sector Internal Audit Standards (PSIAS) require the Head of Internal Audit (HIA) to give the Accounting Officer an opinion on the overall adequacy and effectiveness of the organisation’s framework of governance, risk management and control, timed to inform the Governance Statement.

The NSTA’s focus continues to progress, with the organisation undergoing changes aligned with key risk areas and strategic and business priorities, and internal audit continues to provide assurance activity relating to this, as well as reflecting core controls.

Whilst improvements are needed in some areas, audit testing confirms that controls are proportionate and working as intended.

The HIA opinion on the NSTA’s framework of governance, risk management and management control is ‘Moderate’. Where potential weaknesses have been identified through our internal audit reviews, we have worked with management to agreed appropriate actions and a timescale for improvement.

By order of the Board signed

Stuart Payne

Chief Executive

12 July 2024

Remuneration and staff report

Remuneration policy

The remuneration policy for NSTA staff, including former senior civil servants, is set by the NSTA Board, as recommended by the Remuneration Committee, in consultation with both DESNZ and HM Treasury.

Whilst governed in large part by the rules relating to public bodies, specific arrangements were reached with HM Treasury in 2016 to better align the basic salary arrangements of staff to the relevant talent markets for those roles. This was a one-off adjustment.

Performance and reward

The NSTA has a policy and procedure for managing the performance of all staff to drive performance and reward delivery against clearly articulated goals.

All staff are reviewed during the year and a final assessment of their delivery against agreed goals is made in May. Annual bonus awards are dependent on the consistent attainment or exceeding of goals. No bonus payments are made if staff fail to meet their goals.

Recruitment policy

NSTA recruitment is underpinned by the company’s values:

| Considerate | the best available candidate will be appointed |

|---|---|

| Accountable | those involved take responsibility for their campaigns |

| Robust | the selection processes must be objective, impartial and applied consistently |

| Fair | opportunities are advertised openly and there is no bias in the assessment of candidates |

Recruiting and retaining a diverse range of people to work in the NSTA and ensuring that there is an inclusive environment for them to deliver, is something the company is serious about and demonstrates the NSTA’s values in action. As part of this commitment the NSTA sought and was awarded external accreditation as a Disability Confident employer and signed up to the AXIS network pledge.

As we make clear in our job application process, candidates with a disability who apply for a post in the NSTA (under the Guaranteed Interview Scheme) automatically go forward to the interview stage, provided they satisfy the minimum criteria.

Staff covered by this report hold open-ended appointments, with one exception: the Chief Executive holds a fixed term appointment, which terminates on 31st December 2027. Early termination of any appointment other than for misconduct would result in the individual receiving compensation as set out in the Civil Service Compensation Scheme.

Payments to Directors (audited)

The salary and pension entitlements of executive directors were:

| Member | Salary (actual) 2023-24 (£’000) | Bonus Payment 2023-24 (£’000) | Pension Benefits 2023-24 (£’000) | Total 2023-24 (£’000) | Total 2022-23 (£’000) | Accrued pension at pension age at 31/3/24 (£’000) | Real increase in pension and related lump sum at pension age to 31/3/24 (£’000) | CETV at 31/3/24 (£’000) | CETV at 31/3/23 (£’000) | Real increase in CETV (£’000) |

|---|---|---|---|---|---|---|---|---|---|---|

| Stuart Payne | 260-265* | 45-50** | 84 | 395-400 | 70-75*** | 35-40 | 5-7.5 | 489 | 370 | 55 |

| Nic Granger | 155-160 | 10-15 | 43 | 210-215 | 200-205 | 25-30 | 2.5-5 | 310 | 242 | 29 |

The opening CETV balance is higher than the previously published 2022-23 closing balance, for people with history in final salary schemes. This is because it has been recalculated by MyCSP on the assumption that everyone elects to keep their final salary benefits in the 2015-22 transition period, where they have a choice between this and the scheme they were actually enrolled in during this period (alpha). This is the key part of the Remedy to a 2015 transition into alpha, which the courts decided had been unlawful (the ‘McCloud Remedy’)1.

Stuart Payne was appointed to the Board on 1st January 2023.

*Includes £5k of bought out annual leave.

**Chief Executive’s 2023-24 bonus is for the 2023 performance year (calendar year).

*** The annualised 2022-23 figure for the Chief Executive was £240,000-£245,000.

‘Salary’ includes gross salary, recruitment and retention allowances and any other allowance that is subject to UK taxation.

Fees and benefits in kind paid to non-executive directors during the year (audited)

| Non-executive directors | Expiry date of contract | Fee 2023-24 (£) | Fees 2022-23 (£) |

|---|---|---|---|

| Tim Eggar | |||

| Non-executive Chairman | 30 September 2024 | 80,000 | 80,000 |

| Iain Lanaghan | |||

| Non-executive director (wef 20 April 2020) and from 1 October 2021 Chairman of Audit and Risk Committee. | 30 April 2026 | 25,200 | 25,200 |

| Sarah Deasley | |||

| Non-executive director (wef 1 October 2020) | 30 September 2026 | 20,200 | 20,200 |

| Malcolm Brown | |||

| Non-executive director (wef 1 October 2021) | 30 September 2027 | 20,200 | 20,200 |

| Sara Vaughan | |||

| Non-executive director (wef 1 October 2021) | 30 September 2027 | 20,200 | 20,200 |

Fair pay disclosures (audited)

The relationship to the remuneration of the organisation’s workforce is disclosed in the table below (based on the annualised banded remuneration of the highest paid executive director of £310,000-£315,000):

| 25th percentile | Median | 75th percentile | |

|---|---|---|---|

| 2023-24 | |||

| Total remuneration (£) | 52,256 | 78,997 | 91,247 |

| Salary component of total remuneration (£) | 48,993 | 77,062 | 88,815 |

| Pay remuneration ratio information | 5.98:1 | 3.96:1 | 3.42:1 |

| 2022-23 | |||

| Total remuneration (£) | 45,473 | 74,531 | 86,121 |

| Salary component of total remuneration (£) | 43,012 | 73,387 | 82,588 |

| Pay remuneration ratio information | 8.19:1 | 5.00:1 | 4.33:1 |

The decrease in the pay ratios compared to the previous year is due to a number of factors including the lower salary of the current CEO, an increased headcount where roles have been generally more highly graded and a number of pre- existing posts re-graded upwards.

The assessment in the current year is in line with the performance management period. The NSTA believes the median pay ratio for the relevant financial year is consistent with the pay, reward and progression policies for the NSTA’s employees taken as a whole. NSTA pay ratios have been calculated by determining the total full-time-equivalent (FTE) remuneration for all of the company’s workforce for the relevant financial year; ranking those individuals from low to high, based on their total remuneration; and identifying the people whose remuneration places them at the 25th, 50th (median) and 75th percentile points.

The percentage changes in the highest paid director salary and allowances is -13.22% (2022-23: 3.42%) and for performance pay and bonuses payable is -34.48% (2022-23: 26.09%). The variance in the percentage is due to the lower salary of the highest paid director than in previous years. The average percentage changes for the employees of the NSTA compared to the prior year in respect of salary and allowances is 4.96% (2022-23: 5.01%) and for performance pay and bonuses payable is -4.23% (2022-23: 8.95%). The fluctuation in the percentages, is a result of the annual pay award and an increased headcount, but also a decrease in the CEO bonus payable.

In 2023-24, nil (2022-23: nil) employees received remuneration in excess of the highest-paid director. Remuneration ranged from £28,000 to £315,000 (2022-23: £27,000 to £370,000).

Total remuneration includes salary, non- consolidated performance-related pay and benefits- in-kind. It does not include severance payments, employer pension contributions and the cash equivalent transfer value of pensions.

No senior management or non-executive directors were in receipt of benefits in kind for the financial year 2023-24.