Child and Working Tax Credits statistics: finalised annual awards, supplement on payments, background and definitions - 2018 to 2019

Published 29 October 2021

© Crown copyright 2021

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/statistics/child-and-working-tax-credits-statistics-finalised-annual-awards-supplement-on-payments-2018-to-2019/child-and-working-tax-credits-statistics-finalised-annual-awards-supplement-on-payments-background-and-definitions-2018-to-2019

What are tax credits?

Tax credits are a system of financial support for families based on their specific circumstances.

The system, introduced in 2003, forms part of wider government policy to provide support to parents returning to work, reduce child poverty and increase financial support for families. The design of the system means that as families’ circumstances change, so does (daily) entitlement to tax credits.

Tax credits are based on household circumstances and can be claimed jointly by couples or by single adults. Entitlement is based on the following factors:

- age

- income

- hours worked

- number and age of children

- childcare costs

- disabilities

For further information about who can claim please refer to the benefits page on GOV.UK.

Tax credits are made up of Working Tax Credit (WTC) and Child Tax Credit (CTC), explained below.

Working Tax Credit (WTC)

Provides in-work support for people on low incomes, with or without children. It is available for in-work support to people who are aged at least 16 and either:

- are single, work 16 or more hours a week and are responsible for a child or young person

- are in a couple and are responsible for a child or young person where their combined weekly working hours are at least 24, with one claimant working at least 16 hours

- work 16 or more hours a week and are receiving or have recently received a qualifying sickness or disability related benefit and have a disability that puts them at a disadvantage of getting a job

- work 16 or more hours a week and are aged 60 or over

Otherwise, it is available for people who are aged 25 and over who work 30 hours a week or more. WTC is made up of the following elements:

- basic element: which is paid to any working person who meets the basic eligibility conditions.

- lone parent element: for lone parents

- second adult element: for couples

- 30 hour element: for individuals who work at least 30 hours a week, couples where one person works at least 30 hours a week or couples who have a child and work a total of 30 hours or more a week between them where one of them works at least 16 hours a week.

- disability element: for people who work at least 16 hours a week and who have a disability that puts them at a disadvantage in getting a job and who are receiving or have recently received a qualifying sickness or disability related benefit.

- severe disability element: for people who are in receipt of DLA (Highest Rate Care Component), PIP (Enhanced Daily Living Component) or Attendance Allowance at the highest rate.

- childcare element: for a single parent who works at least 16 hours a week, or couples who either (i) both work at least 16 hours a week or (ii) one of them work at least 16 hours a week but the other is out of work for being in hospital or in prison and who spends money on a registered or approved childcare provider. The childcare element of WTC can support up to 70% of childcare costs up to certain maximum limits

Further information on childcare cost support can be found on GOV.UK.

Child Tax Credit (CTC)

Provides income-related support for children and qualifying young people aged 16-19 who are in full time, non-advanced education or approved training into a single tax credit, payable to the main carer. Families can claim CTC whether or not the adults are in work. CTC is made up of the following elements:

- family element: which is the basic element for families responsible for one or more children or qualifying young people. From 6 April 2017, this element is only payable to families with at least one child born before this date

- child element: which is paid for each child or qualifying young person the claimant is responsible for. From 6 April 2017, this element is no longer payable in respect of third or subsequent children who were born after this date. Certain exceptions to this rule apply and are set out at the CTC exceptions to the 2 child limit page on GOV.UK

- disability element: for each child or qualifying young person the claimant is responsible for if Disability Living Allowance (DLA) or Personal Independence Payment (PIP) is payable for the child, or if the child is certified as blind or severely sight impaired.

- severe disability element: for each child or qualifying young person the claimant is responsible for if DLA (Highest Rate Care Component) or PIP (Enhanced Daily Living Component) is payable for the child

- out-of-work benefit families: some out-of-work families with children do not receive CTC but instead receive the equivalent amount via child and related allowances in Income Support or income-based Jobseeker’s Allowance (IS/JSA). These families are included in the figures, generally together with out-of-work families receiving CTC. The vast majority of these claimants have now moved to tax credits and the remainder will be migrated either to tax credits or Universal Credit (UC)

Tapering

Tapering is the amount of the award that will be reduced when the household income exceeds a given threshold.

For example, the income threshold for claimants receiving WTC only and for combined WTC and CTC claimants is £6,420 (2018 to 2019). After this threshold, the taper rate will be 41%. Tapering reduces WTC first and then CTC for claimants who receive both. The section below explains how the taper process works in practice.

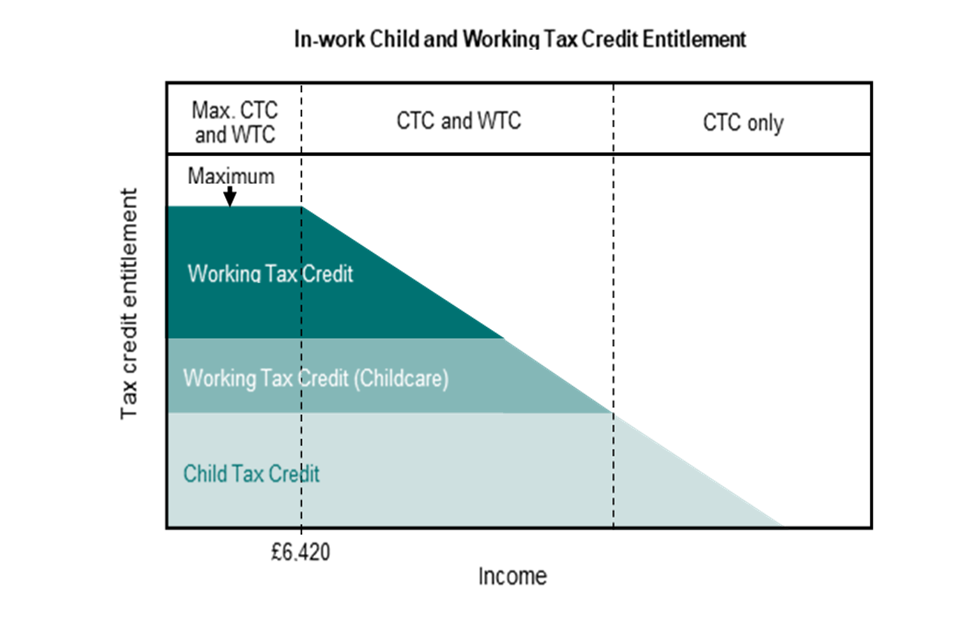

Child and Working Tax Credit Entitlement

The amount of support an eligible family can receive (known as their entitlement) varies depending on their income and their eligibility for specific tax credit elements.

First, a family’s maximum possible entitlement is worked out by adding up all the different elements of CTC and WTC that they are eligible for (described above).

A household’s actual entitlement is then determined by tapering this maximum amount according to different thresholds.

As demonstrated within the diagram below, families eligible for the WTC receive the full entitlement until their annual household income reaches £6,420, after which the amount of tax credits they receive is reduced by 41 pence for each £1 they earn beyond this threshold.

If a household is eligible for CTC only, they will receive the full entitlement until their annual household income reaches £16,105 (2018 to 2019). After this point, the amount of tax credits they receive is again reduced by 41 pence for each additional £1 of income beyond this threshold (note that this is not shown on the diagram below).

Because of the range of possible eligibilities and interactions between the elements, both the maximum award and the shape of the above award profile will be different for every family with different circumstances.

Tax credits are based on the taxable income of adults within the family. The income used to calculate the award is based on the families’ income from the previous tax year, or on their most recently reported circumstances in-year. Up to £2,500 of any change in annual income between the previous or current year is disregarded in the calculation.

A family’s tax credits award is provisional until finalised at the end of the year, when it is checked against their final income for the year. This publication relates to a snapshot of tax credit support based on provisional incomes and other circumstances as reported at the date when the statistics were extracted.

About this publication

Timing of this publication

The finalised awards supplement on payments is usually published around a year after completion of the entitlement year in question. The one year lag is due to the finalisation process built into the Tax Credits system.

Most families have until July 31st following the end of the entitlement year to renew their award reporting their finalised income for the year in question. However, families that report income from Self-Assessment (e.g., the self-employed) have until January 31st of the following year to finalise their income. As a result, the full picture is not known until at least February the year after the entitlement year ends and consequently publication is delayed until after this period.

Geographical Statistics

HMRC launched a wide-ranging consultation on a range of statistics on 8 February 2021 found on GOV.UK.

Following this consultation we decided to drop the geographical component of the supplements on payments publication as there was insufficient user demand for this information.

Provisional awards vs finalised awards

It is important to recognise that the finalised awards statistics are not a revision of the provisional statistics.

The provisional numbers relate to the caseload position at a snapshot point in time, based on the latest family circumstances HMRC have been informed of by each family prior to that particular time.

The finalised awards relate to the complete retrospective picture for the year, based on a finalised view of family incomes and circumstances. The caseload population will be different between the two publications as a result of HMRC knowing the complete finalised picture of the award.

At the start of the year, the tax credit award will be a provisional award reflecting the reported circumstances as at 6 April (the start of the tax year). Over the course of the year, a family’s circumstances may or may not change.

The provisional award is updated each time HMRC are informed of a change in the family’s circumstances and a new provisional award is calculated. It is only at finalisation (usually four to nine months after the end of the tax year) that the family’s circumstances for the whole year are known and a finalised award can be calculated. As a result, the finalised award statistics are not available until around 12 months after the end of the entitlement year in question.

Given this lag in availability of data, there is some value in looking at a snapshot of families’ circumstances at any given time to give some indication of the level of support one might expect to see subsequently at finalisation.

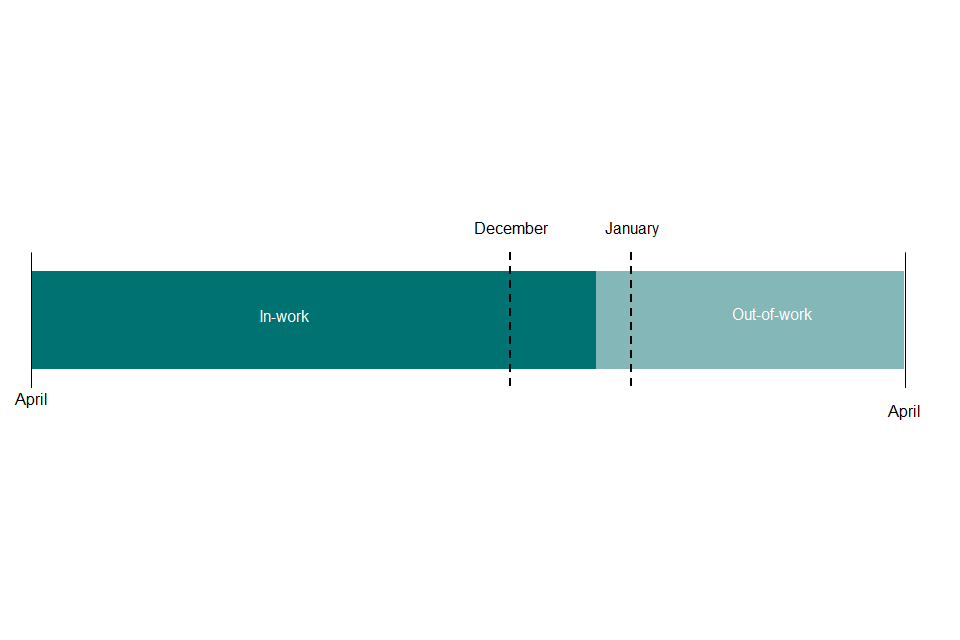

To illustrate the difference, let us look at a family that has one change of circumstance throughout the year, moving from in-work to out-of-work in January of any one year.

The snapshot data looking at the provisional award in April will model entitlement for the whole year on the basis that the family is in-work for the whole year (since we do not know about the move out-of-work at that time).

It is not until finalisation, and thereby in the finalised award data publication, that the family’s entitlement will be modelled on the basis of 9 months in-work and 3 months out-of-work.

Therefore, the figures for provisional awards are more up to date, but are subject to retrospective change. The sizes of these changes can be seen by comparing the data for selected dates in finalised awards with data published earlier on provisional awards at the same time snapshot dates.

The provisional award data classify families according to the levels of their entitlement at the reference date, modelled from data on their circumstances and their latest annual incomes reported by that date. The actual amount being received at that date can be lower, due to recovery of earlier overpayments.

Which publication should I use?

Generally, if you are interested in the final end of year position, use the finalised awards data publication. If you are more concerned with getting the latest up-to-date information that may not align exactly with finalised data further down the line, use the provisional awards data.

Using the finalised award data will also mean the figures will align with other published data on tax credits, such as information in HMRC’s Departmental Accounts. The latest provisional award publication can be found on the personal tax credits statistics page on GOV.UK.

What information do the tables contain?

CTC and WTC are claimed by individuals, or jointly by couples, whether or not they have children (described as “families” in this publication). These tables cover families who had claimed, and were eligible for, CTC (or the equivalent via benefits) or WTC for all or part of the 2018 to 2019 tax year.

Table 1 includes both out-of-work and in-work families, and show the time series since 2003 to 2004 of the number of overpayments and underpayments paid to the tax credits population. Also included are the aggregate amount of tax credits overpaid or underpaid since 2003 to 2004.

Table 2 provides an overview of payments to the tax credits population during 2018 to 2019.

Table 3 breaks up these payments by the size of under or overpayment.

Table 4 breaks up these payments by whether the recipients are single or in a couple (as assessed at the time of payment).

Table 5 breaks up the payments by the families income during 2018 to 2019.

Table 6 breaks up these payments by the families income during 2018 to 2019 compared to the families income during the previous year (2017 to 2018).

These tables will also include part year claims for individuals who have moved to UC (an explanation of UC is found below) and these claimants could fall into any payment category (underpaid, overpaid or neither). The actual payment category will be dependent on the in-year finalisation figure for that claimant.

Recent policy changes

In the 2015 Summer Budget, the Government announced that the child element of CTC would be limited to two children for those born on or after 6 April 2017 unless certain exceptions apply. Prior to 6 April 2017, the child element of CTC was paid for each child or qualifying young person that the claimant (or his or her partner) was responsible for.

The change means that any family with two or more existing children do not receive any child element (worth up to £2,780 a year per child in 2018 to 2019) for children born on or after that date, subject to exceptions. The child element of CTC continues to be paid for all children born before 6 April 2017.

In addition, any family having their first child born on or after 6 April 2017 do not receive the family element (worth up to £545 a year) of CTC. The family element was previously paid to all families. From 6 April 2017, it is only be paid where the claimant is responsible for at least one child or qualifying young person born before 6 April 2017.

For further information, please visit the CTC exceptions to the 2 child limit page on GOV.UK.

Statistics related to this policy can be found on the Official Statistics on GOV.UK.

Universal Credit

UC is a payment to help with living costs for those on a low income or out of work. UC was introduced in April 2013 in certain areas of North West England. Since October 2013, it has progressively been rolled out to other areas.

Claimants receive a single monthly household payment, paid into a bank account in the same way as a monthly salary and support for housing costs, children and childcare costs are integrated into UC.

CTC will be replaced as UC rolls out. Since December 2018 there have been no new tax credit claims (with the exception of a small number of families claiming the family premium).

Further information about UC, including making a claim, is available on the UC page on GOV.UK.

Statistics related to UC are available online and can be found on the UC statistics page on GOV.UK.

Uses of these statistics

The statistics contained in this publication will be of interest for anyone that is looking for the most comprehensive data on Tax Credits. Specifically, there are aggregate statistics on who is getting what level of tax credits support and the amount of that support, as well as breakdowns of both by various sub-categories - e.g., family composition, family income and work status.

It may be of interest to academics, think tanks, political parties interested in the twin aims of Tax Credits: eradicating child poverty and improving work incentives. Equally, it may be of interest for people considering wider questions on government support systems and/or others designing benefit systems.

User Engagement

Bespoke analysis of tax credits data is possible although there may be a charge depending on the level of complexity and the resources required to produce. If you would like to discuss your requirements, to comment on the current publications, or for further information about the tax credits statistics please use the contact information at the end of this publication, or from the Statistics at HMRC page.

We are committed to improving the official statistics we publish. We want to encourage and promote user engagement, so we can improve our statistical outputs.

We would welcome any views you have by email to the below address. We will undertake to review user comments on a quarterly basis and use this information to influence the development of our official statistics. We will summarise and publish user comments at regular intervals.

benefitsandcredits.analysis@hmrc.gov.uk

Revision policy

This policy has been developed in accordance with the UK Statistics Authority Code of Practice for Official Statistics and Her Majesty’s Revenue and Customs Revisions Policy. The UK Statistics Authority Code of Practice can be found on GOV.UK.

There are two types of revisions:

Scheduled revisions

This requires explanation of the handling of scheduled revisions due to the receipt of updated information in the case of each statistical publication.

Unscheduled revision

HMRC aims to avoid the need for unscheduled revisions to publications unless they are absolutely necessary and put systems and processes in place to minimise the number of revisions. Where revisions is necessary due to errors in the statistical process, an explanation along with the nature and extent of revision is also provided. Also, the statistical release and the accompanying tables will be updated and published as soon as is practical.

Disclosure control

To avoid the possible disclosure of information about individual families, values have been supressed when underlying sample counts are low. An entry of “-“ or “[no data]” in a table indicates that the data has been rounded down to 0 or has been withheld in line with HMRC’s Dominance and Disclosure policy.