Creative industries statistics commentary: August 2021

Published 24 August 2021

© Crown copyright 2021

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/statistics/creative-industries-statistics-august-2021/creative-industries-statistics-commentary-august-2021

1. Summary

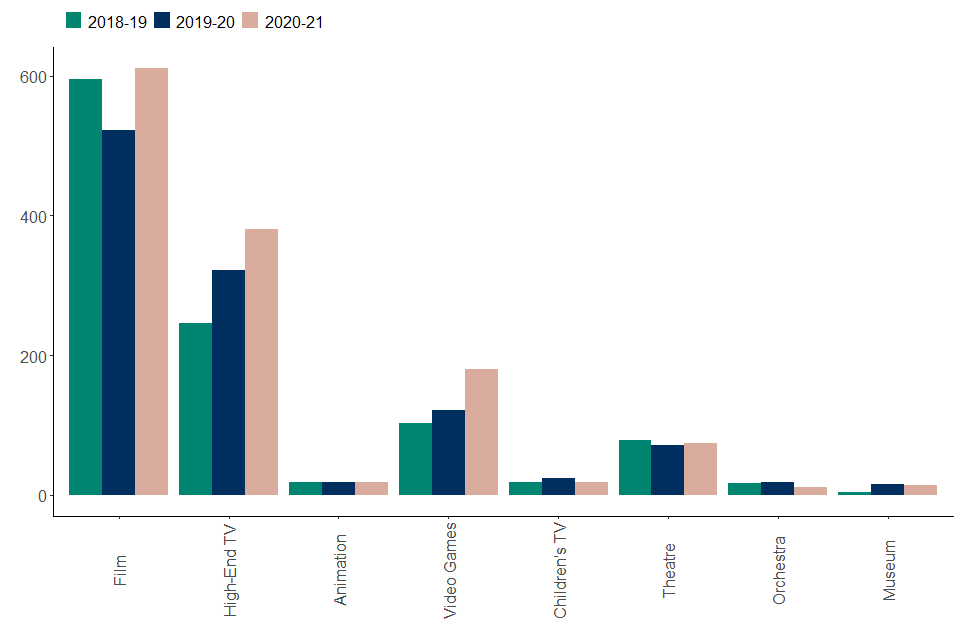

In the year ending March 2021, a total of £1.31 billion was paid out across all the creative industries tax reliefs. This is an increase from £1.11 billion in the year ending March 2020. In the year ending March 2021, Film tax relief accounts for nearly half of the total amount paid out and high-end television (HETV) tax relief accounts for almost 30% of the total (Figure 1 and Table 1).

Figure 1: Creative industries tax reliefs (£ million, receipts basis), 2018-19 to 2020-21

Table 1: Number of projects, claims and amount of creative industries tax relief paid out (£ million) in 2020-21

| Relief | Number of projects | Number of claims | Amount of relief paid |

|---|---|---|---|

| Film | 870 | 900 | 611 |

| High-End TV | 315 | 315 | 380 |

| Animation | 100 | 90 | 18 |

| Video Games | 640 | 350 | 180 |

| Children’s TV | 105 | 65 | 19 |

| Theatre | 3,660 | 1,070 | 74 |

| Orchestra | 750 | 175 | 11 |

| Museum | 1,555 | 190 | 14 |

| Total | 7,995 | 3,155 | 1,307 |

The number of projects refers to the number of films, programmes, games, productions or exhibitions.

2. Introduction

This is an Official Statistics publication produced by HM Revenue and Customs (HMRC). It provides information on the number and value of claims for film, high-end television, animation, video games, children’s television, theatre, orchestra, and museums and galleries exhibition tax reliefs, for the financial years up to March 2021.

The statistical tables are published on GOV.UK alongside this commentary document, together with information on the background and methodology.

This is an annual release and the next release is planned to be in Summer 2022.

The tax relief amounts paid out in the year ending March 2021 mainly relate to activity which took place in earlier years. The impact of the Covid-19 pandemic will be seen in next year’s statistics.

Statistical contacts: N. Chowdhury, P. Patel and D. Parry; ct.statistics@hmrc.gov.uk

Media enquiries: HMRC Press Office; news.desk@hmrc.gov.uk

3. Film tax relief

Film tax relief (FTR) allows qualifying film production companies to make a deduction in their taxable profits or to surrender a loss for a payable tax credit. A film may make several tax relief claims during the production process. A claim may cover several films.

Since FTR was introduced in 2007, 3,845 films have made claims, with UK expenditure of £20.2 billion.

3.1 Number and value of claims by date paid (receipts basis)

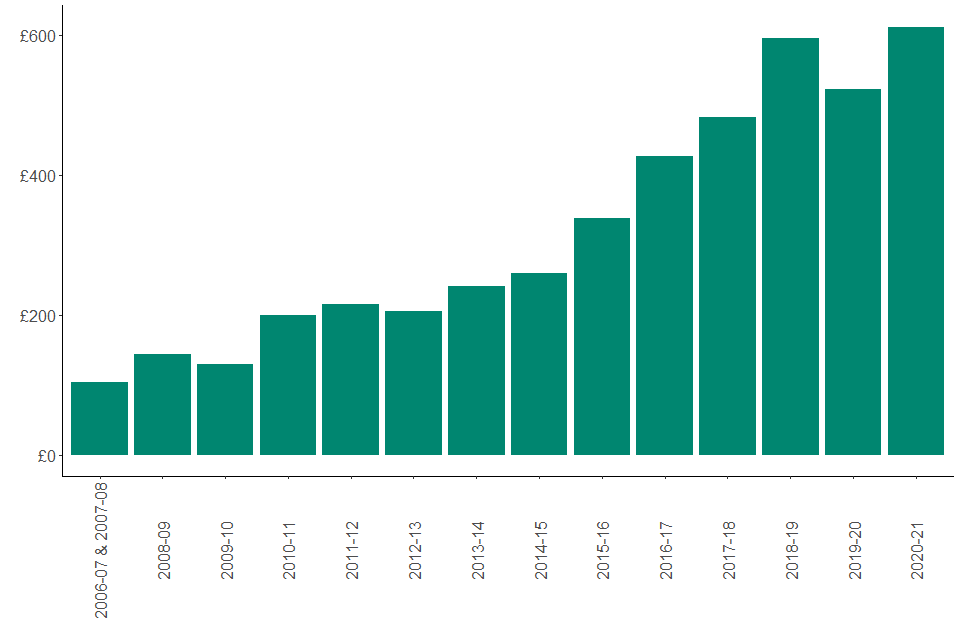

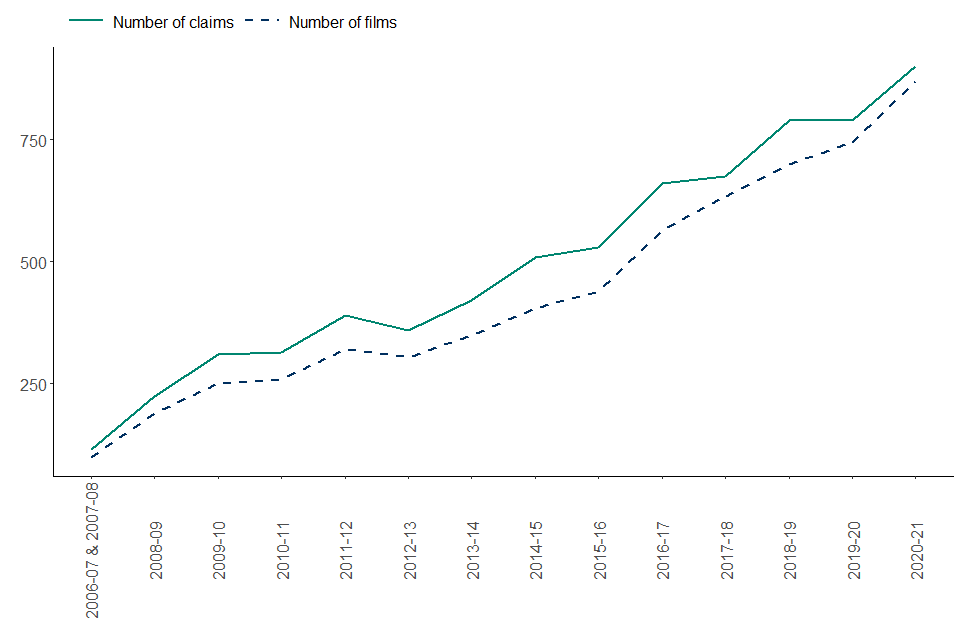

In the year ending March 2021, £611 million of FTR was paid in response to 900 claims, representing 870 films. The number and cost of claims has generally tended to increase year on year (see Figure 2, Table 1.3). There was a larger increase in relief paid out in the year ending March 2019, with a fall in the following year and another large increase in the year ending March 2021. The fluctuations were greatest for claims worth between £5 million and £10 million (Table 1.4). The accruals data (Table 1.2) show a smoother trend. The proportions of the total relief amount paid out in the same year and the following year have varied considerably, resulting in a more volatile profile on a receipts basis. A total of £4.5 billion has been paid since 2007.

Figure 2: Amount of film tax relief paid (£ million, receipts basis) 2006-07 to 2020-21

Figure 3: Number of films and number of claims, 2006-07 to 2020-21

In the year ending March 2021, 67% of all claims were for £100,000 or less. The proportion is similar to last year. Despite only 4% of the claims being for over £5 million in the year ending March 2021, they account for more than two-thirds of the total amount paid.

4. High-end television tax relief

HETV tax relief allows qualifying production companies to make a deduction in their taxable profits or to surrender a loss for a payable tax credit. A programme may make several tax relief claims during the production process. A claim may cover several programmes.

Since HETV tax relief was introduced in 2013, 760 programmes have made claims, with UK expenditure of £7.9 billion.

4.1 Number and value of claims by date paid (receipts basis)

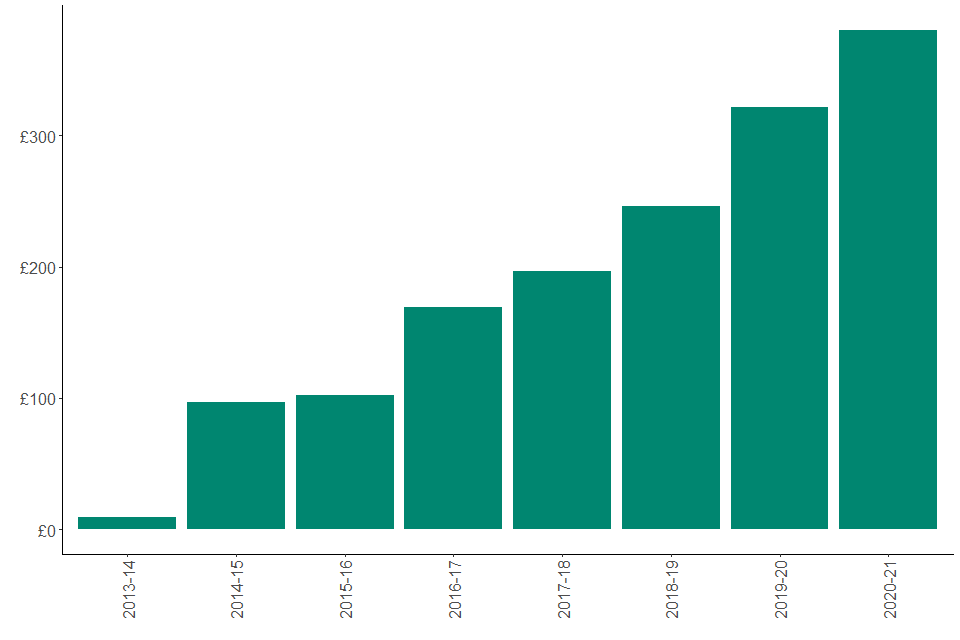

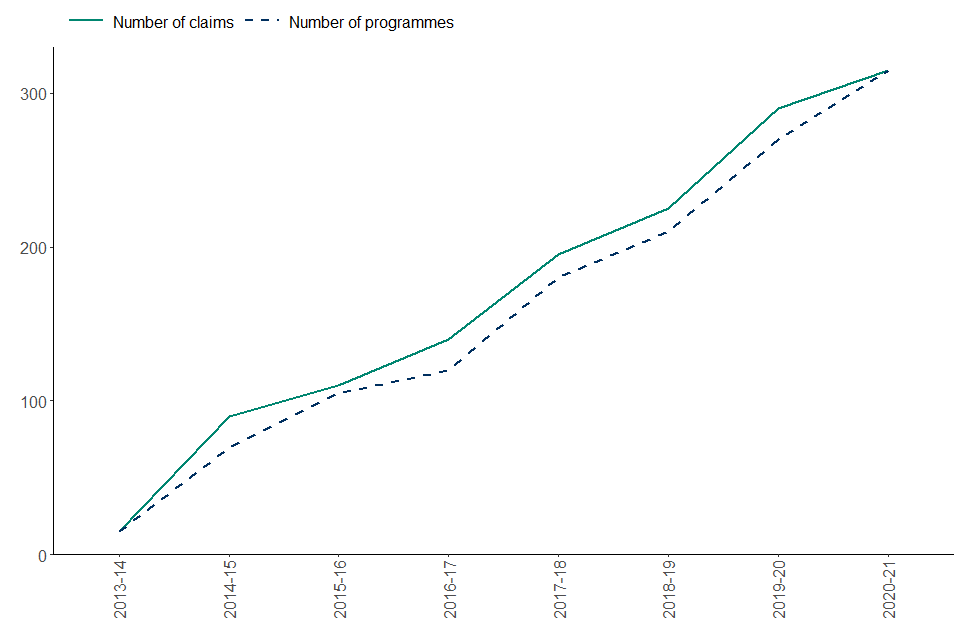

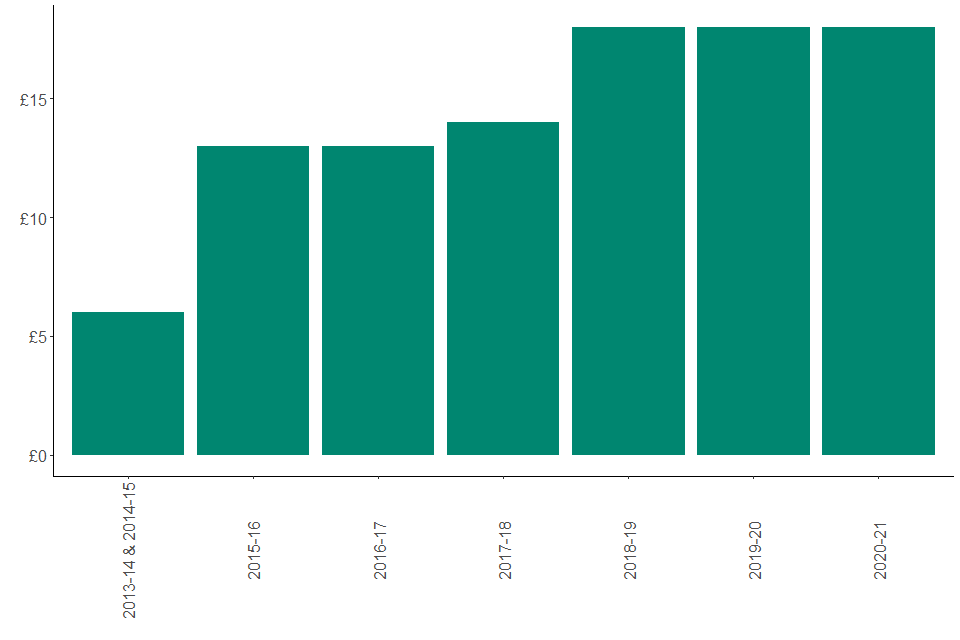

In the year ending March 2021, £380 million of HETV tax relief was paid in response to 315 claims, representing 315 programmes. The amount of tax relief rose by 18% from the previous year, reflecting continued growth in the volume and value of large claims. The accruals data (Table 2.2) show a sharp increase in the amount of relief claimed for the year ending March 2020. This reflects an expansion of activity in the high-end television industry. The trend is more gradual on a receipts basis (Figure 4 and Table 2.3) because some claims were received later than usual and were paid out after March 2021. A total of £1.5 billion has been paid since the relief was introduced.

Figure 4: Amount of HETV tax relief paid (£ million, receipts basis) 2013-14 to 2020-21

Figure 5: Number of programmes and number of claims, 2013-14 to 2020-21

In the year ending March 2021, over a third of the number of claims were for less than £250,000 – however, these only accounted for 3% of the total amount paid. Large claims over £2 million accounted for two-thirds of the total amount paid. This proportion has increased from the previous year.

5. Animation tax relief

Animation tax relief (ATR) allows qualifying animation companies to make a deduction in their taxable profits or to surrender a loss for a payable tax credit. A programme may make several tax relief claims during the production process. A claim may cover several programmes.

Since ATR was introduced in 2013, 360 programmes have made claims, with UK expenditure of £593 million.

5.1 Number and value of claims by date paid (receipts basis)

In the year ending March 2021, £18 million of ATR was paid in response to 90 claims, representing 100 programmes. A total of £99 million has been paid since the relief was introduced.

Figure 6: Amount of animation tax relief paid (£ million, receipts basis) 2013-14 to 2020-21

Figure 7: Number of claims and number of programmes, 2013-14 to 2020-21

In the year ending March 2021, 28% of ATR claims were for values of over £250,000 and they accounted for 81% of the total amount paid out.

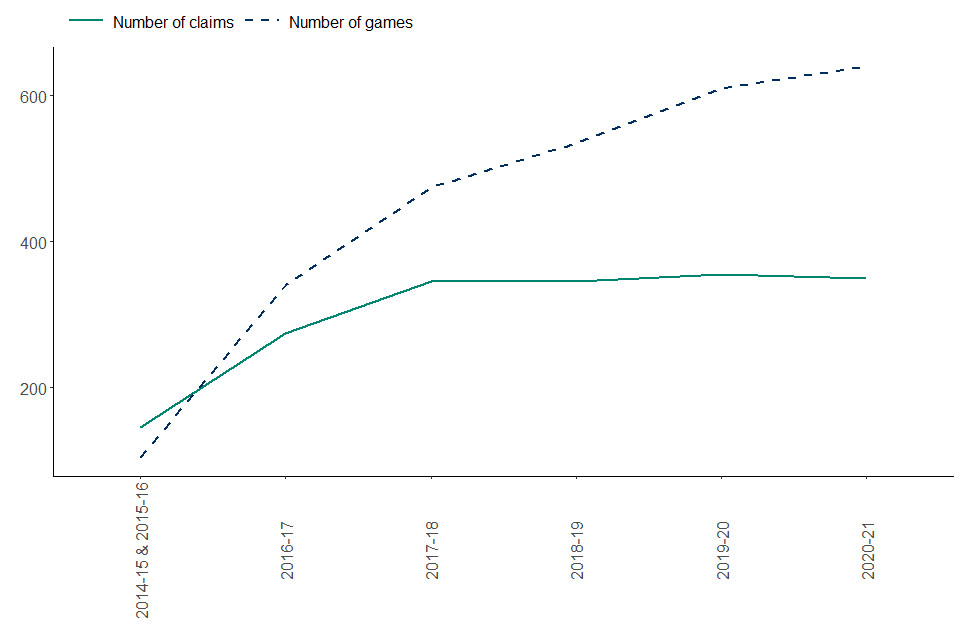

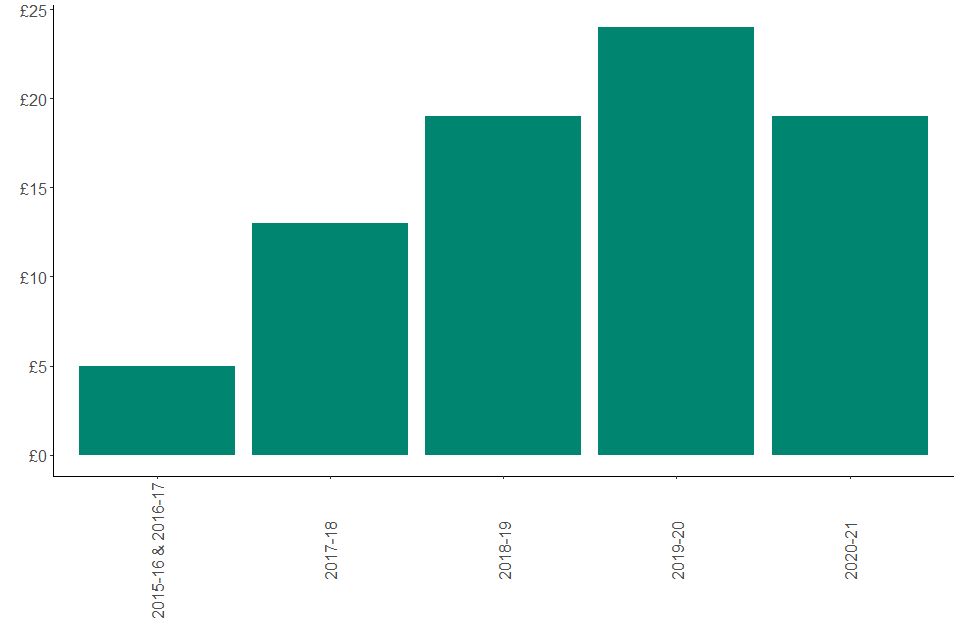

6. Video games tax relief

Video games tax relief (VGTR) allows qualifying video games companies to make a deduction in their taxable profits or to surrender a loss for a payable tax credit. A game may make several tax relief claims during the production process. A claim may cover several games.

Since VGTR was introduced in 2014, 1,640 games have made claims, with UK expenditure of £4.4 billion.

6.1 Number and value of claims by date paid (receipts basis)

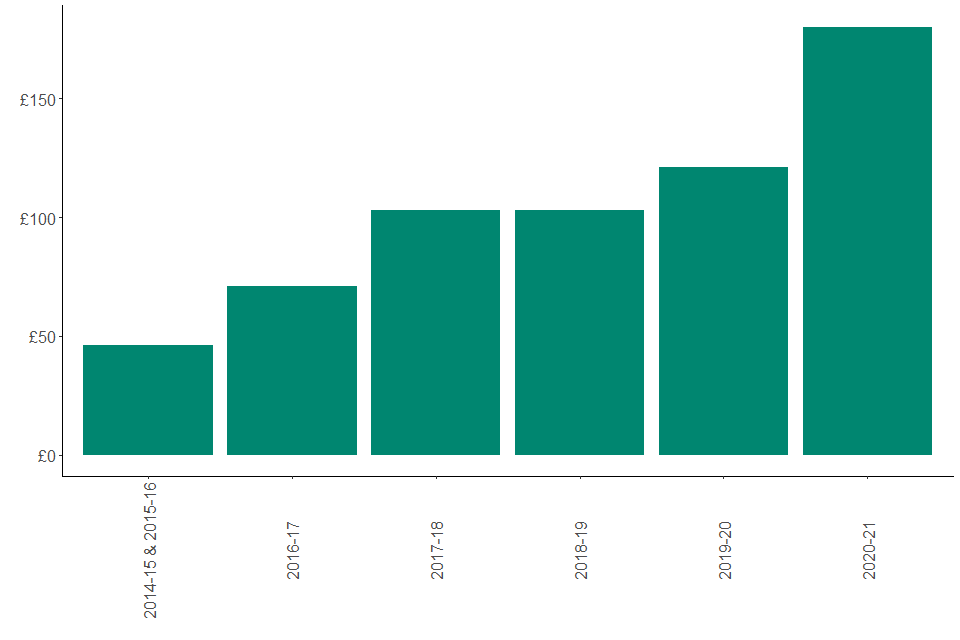

In the year ending March 2021, £180 million of VGTR was paid in response to 350 claims, representing 640 games. The amount of relief increased by 48% compared with the previous year (Figure 8 and Table 4.3). This can be explained by the timing of large payments for a small number of very high-budget games and underlying growth in the value of claims. A total of £624 million has been paid since the relief was introduced.

Figure 8: Amount of video games tax relief paid (£ million, receipts basis) 2014-15 to 2020-21

Figure 9: Number of games and number of claims, 2014-15 to 2020-21

In the year ending March 2021, the majority of claims tend to be for smaller amounts, with 47% of all claims being for £50,000 or less; however, these claims are only responsible for 2% of the total amount paid out. Claims over £500,000 account for 87% of the total amount paid out. This proportion has increased from the previous year.

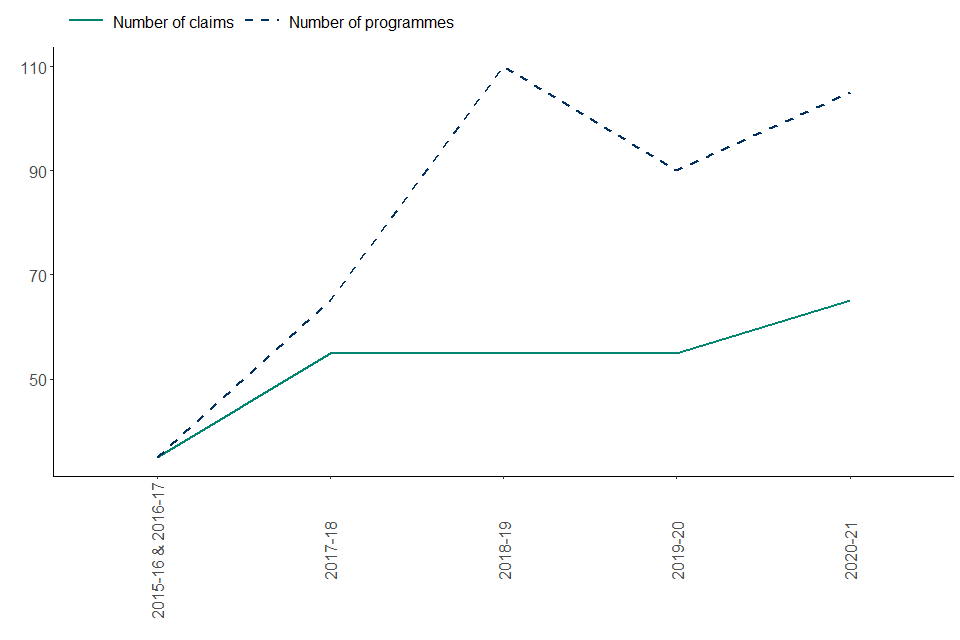

7. Children’s television tax relief

Children’s television tax relief (CTR) allows qualifying companies to make a deduction in their taxable profits or to surrender a loss for a payable tax credit. It is an extension of high-end television tax relief and animation relief, but is specifically aimed at the producers of children’s television programmes. CTR is not subject to the £1 million per slot hour threshold or the 30 minute minimum slot length that applies to high-end television programmes. The measure was announced at Autumn Statement 2014, and took effect for qualifying expenditure incurred on or after 1 April 2015.

Since CTR was introduced in 2015, 340 programmes have made claims, with UK expenditure of £380 million.

7.1 Number and value of claims by date paid (receipts basis)

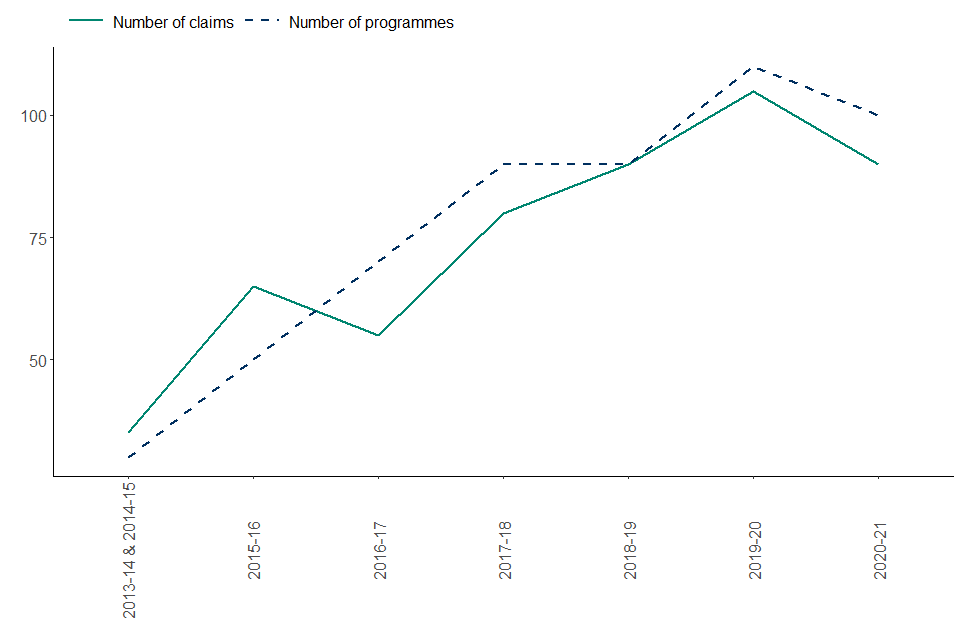

In the year ending March 2021, £19 million of CTR was paid in response to 65 claims, representing 105 programmes. A total of £80 million has been paid since the relief was introduced.

Figure 10: Amount of children’s TV tax relief paid (£ million, receipts basis) 2015-16 to 2020-21

Figure 11: Number of programmes and number of claims, 2015-16 to 2020-21

In the year ending March 2021, only 9% of the claims were for amounts over £500,000, but these account for 63% of the total amount paid out.

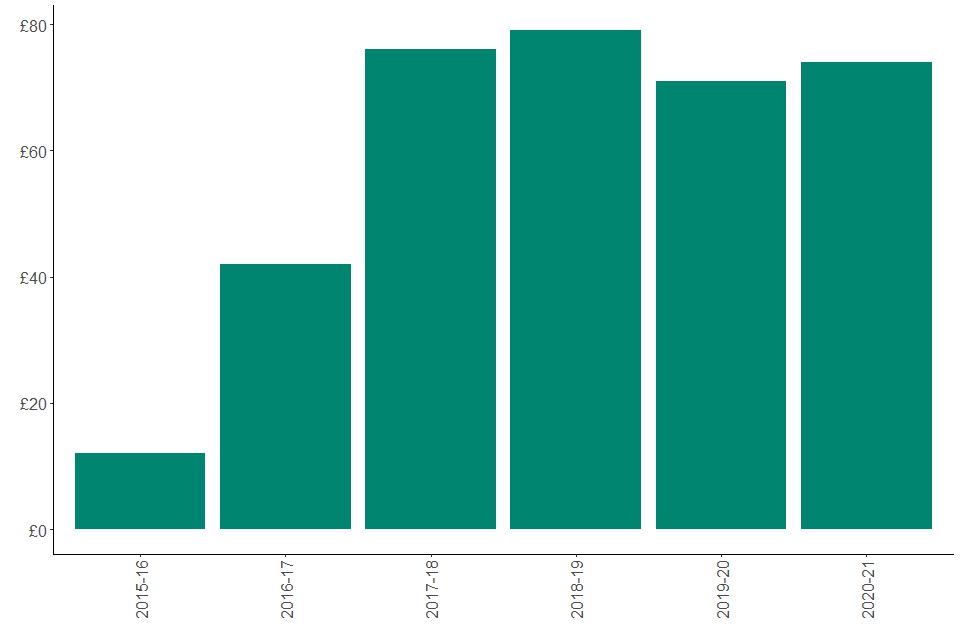

8. Theatre tax relief

Theatre tax relief (TTR) was announced in the Finance Act of 2014 and introduced in September 2014. Theatrical production companies are not required to pass a cultural test to be eligible to claim tax relief. A theatre production company may make several claims during the production process. A claim may cover several productions.

Since TTR was introduced in 2014, £354 million has been paid out relating to 4,710 claims. This represents 15,725 productions.

8.1 Number and value of claims by date paid (receipts basis)

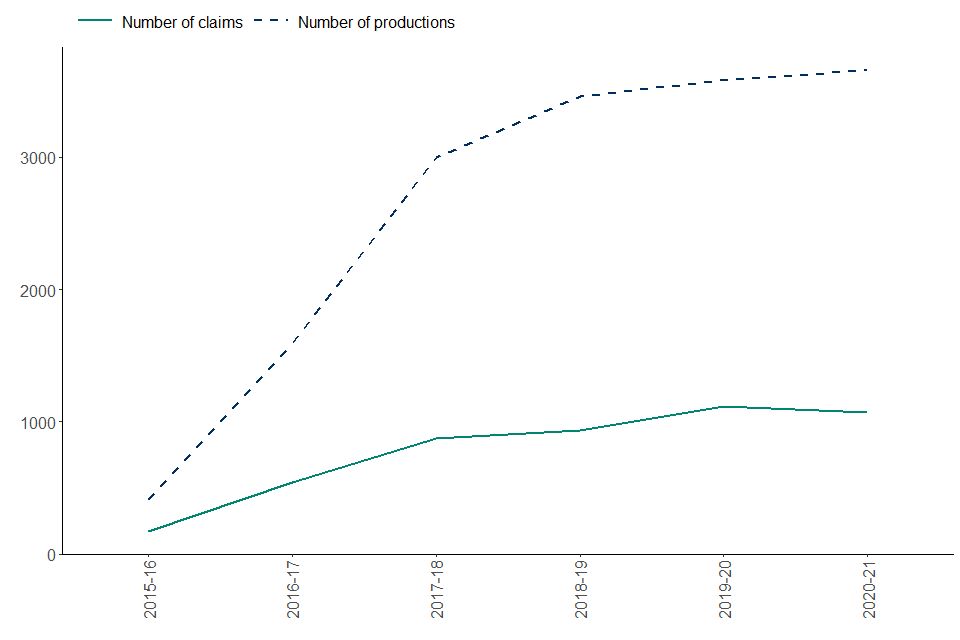

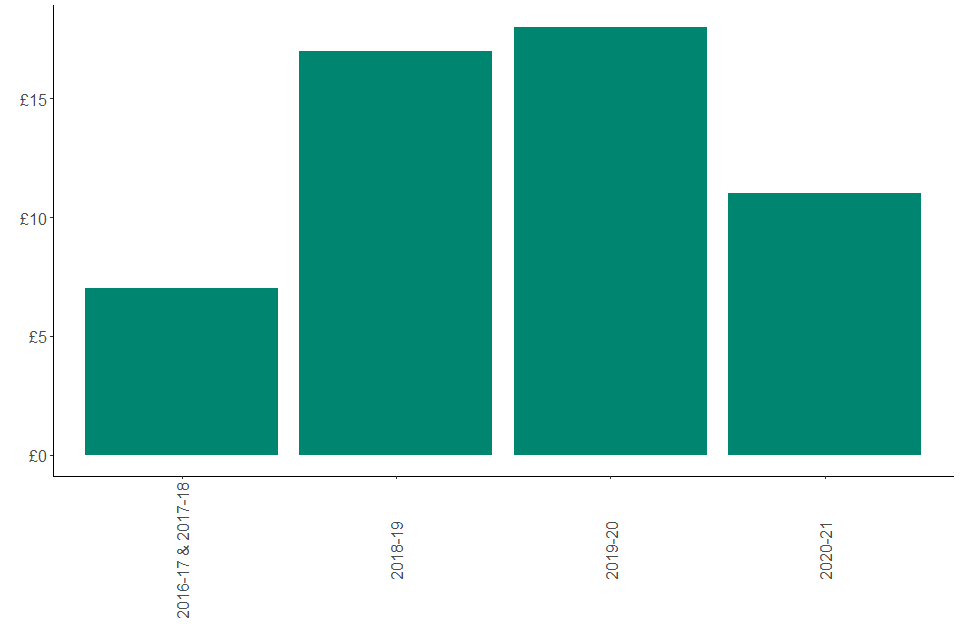

In the year ending March 2021, £74 million of TTR was paid in response to 1,070 claims, representing 3,660 productions. Of the productions, 72% were non-touring.

Figure 12: Amount of theatre tax relief paid (£ million, receipts basis) 2015-16 to 2020-21

Figure 13: Number of productions and number of claims, 2015-16 to 2020-21

The highest proportion of claims are for smaller amounts, with 47% of all claims being for £10,000 or less in the year ending March 2021 whilst claims over £250,000 represented just 6% of the claims made but 58% of the total amount paid out.

9. Orchestra tax relief

Orchestra tax relief (OTR) was introduced in April 2016. Orchestral production companies are not required to pass a cultural test to be eligible to claim tax relief. An orchestral production company may make a number of claims, receiving payments at stages throughout the production process. A claim may cover several productions. If a company has made an election covering multiple productions, then the series of productions is treated as a single production.

Since OTR was introduced, £52 million has been paid out relating to 515 claims. This represents 2,130 productions.

9.1 Number and value of claims by date paid (receipts basis)

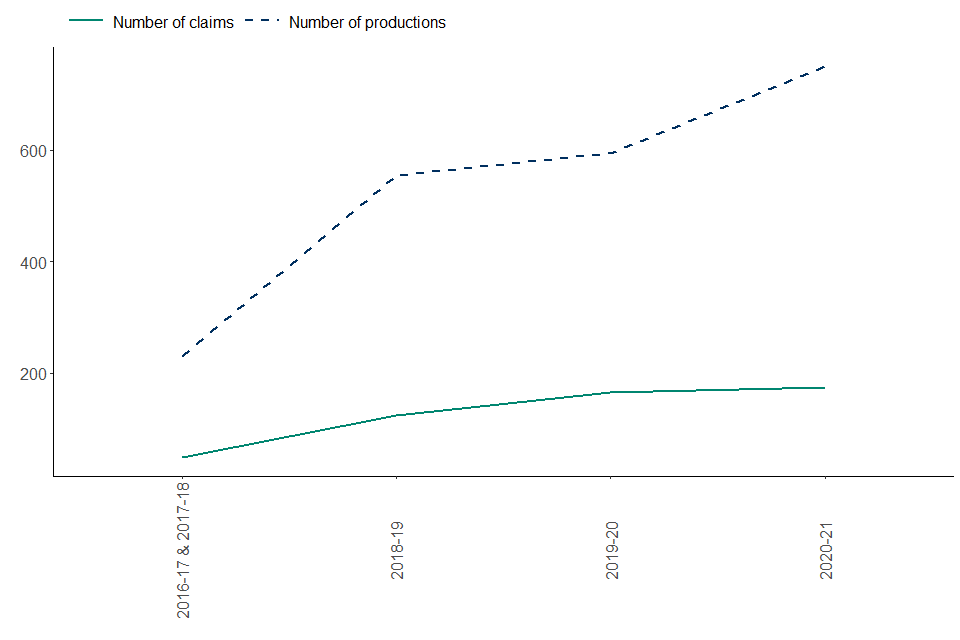

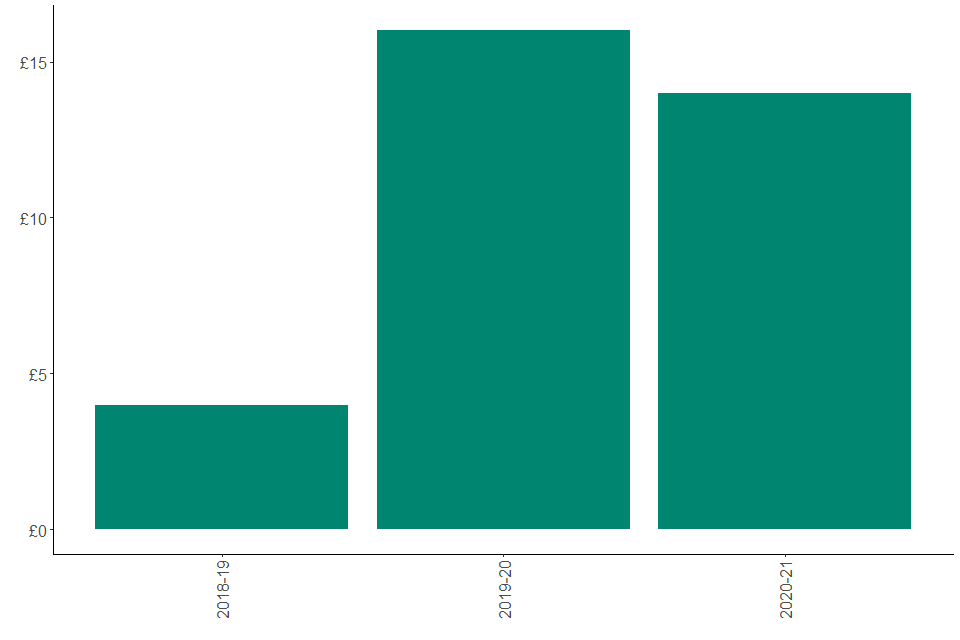

In the year ending March 2021, £11 million of OTR was paid in response to 175 claims, representing 750 productions. Although the number of claims has increased since the previous year, the amount of relief has fallen.

Figure 14: Amount of Orchestra tax relief paid (£ million, receipts basis) 2016-17 to 2020-21

Figure 15: Number of productions and number of claims, 2016-17 to 2020-21

The highest proportion of claims are for smaller amounts. Claims of £5,000 or less represented 47% of the claims in the year ending March 2021. While only 7% of all claims were for amounts over £250,000, they represented 68% of the amount paid.

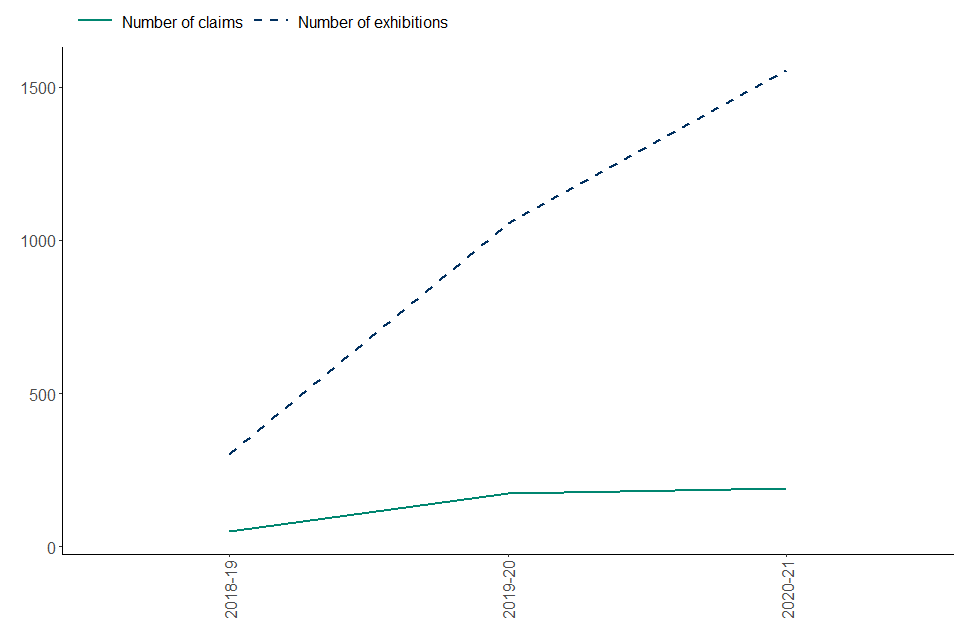

10. Museums and galleries exhibition tax relief

Museums and galleries exhibition tax relief (MGETR) was introduced in April 2017. Exhibition companies are not required to pass a cultural test to be eligible to claim tax relief. Relief is only available to charitable companies, and to subsidiaries of charities and local authorities. Tax credits are capped per exhibition at a maximum of £100,000 (touring) or £80,000 (non-touring). A museum or gallery may make a number of claims, receiving payments at stages throughout the exhibition process. A claim may cover several exhibitions.

Since MGETR was introduced, £34 million has been paid out relating to 415 claims. This represents 2,910 exhibitions.

10.1 Number and value of claims by date paid (receipts basis)

In the year ending March 2021, £14 million of MGETR was paid in response to 190 claims, representing 1,555 exhibitions.

Figure 16: Amount of museums and galleries tax relief paid (£ million, receipts basis) 2018-19 to 2020-21

Figure 17: Number of exhibitions and number of claims, 2018-19 to 2020-21

The highest proportion of claims are for smaller amounts, with 49% of all claims being for £25,000 or less in the year ending March 2021. Only 19% of claims were over £100,000 but they accounted for 72% of the total amount paid out.