Background information: Fraud and error in the benefit system statistics, 2023 to 2024 estimates

Published 16 May 2024

Applies to England, Scotland and Wales

© Crown copyright 2024

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/statistics/fraud-and-error-in-the-benefit-system-financial-year-2023-to-2024-estimates/background-information-fraud-and-error-in-the-benefit-system-statistics-2023-to-2024-estimates

Purpose of the statistics

Context and purpose of the statistics

This document supports our main publication which contains estimates of the level of fraud and error in the benefit system in Financial Year Ending (FYE) 2024.

We measure fraud and error so we can understand the levels, trends, and reasons behind it. This understanding supports decision making on what actions DWP can take to reduce the level of fraud and error in the benefit system. The National Audit Office takes account of the amount of fraud and error when they audit DWP’s accounts each year.

Within DWP these statistics are used to evaluate, develop, and support fraud and error policy, strategy and operational decisions, initiatives, options, and business plans through understanding the causes of fraud and error.

The fraud and error statistics published in May each year feed into the DWP accounts. The FYE 2024 estimates published in May 2024 feed into the FYE 2024 DWP annual report and accounts.

The statistics are also used within the annual HM Revenue and Customs National Insurance Fund accounts. These are available in the National Insurance Fund Accounts section of the HMRC reports page.

The fraud and error estimates are also used to answer Parliamentary Questions and Freedom of Information requests, and to inform DWP Press Office statements on fraud and error.

Limitations of the statistics

The estimates do not include reviews of every benefit each year. This year, Employment and Support Allowance was removed from the measured list of benefits and Disability Living Allowance was measured for the first time since FYE 2005. Also, this year the Pension Age Housing Benefit client groups were measured rather than the Non-passported Working Age Housing Benefit client group that was measured in FYE 2023.

This document includes further information on limitations – for example, on benefits reviewed and changes this year (section 1 and section 2, omissions to the estimates (section 3), and our sampling approach (section 4).

Longer time series comparisons may not be possible for some levels of reporting due to methodology changes. Our main publication and reference tables indicate when comparisons should not be made.

We are unable to provide sub-national estimates of fraud and error as we are unable to break the statistics down to this level.

Comparisons between the statistics

These statistics relate to the levels of fraud and error in the benefit system in Great Britain.

Social Security Scotland report the levels of fraud and error for benefit expenditure devolved to the Scottish Government within their annual report and accounts.

Northern Ireland fraud and error statistics are comparable to the Great Britain statistics within this report as their approach to collecting the measurement survey data, and calculating the estimates and confidence intervals, is very similar. Northern Ireland fraud and error in the benefit system high level statistics are published within the Department for Communities annual reports.

HM Revenue and Customs produce statistics on error and fraud in Tax Credits.

When comparing different time periods within our publication, we recommend comparing percentage rates of fraud and error rather than monetary amounts. This is because the amount of fraud and error in pounds could go up, even if the percentage rate of fraud and error stays the same or goes down, if the amount of benefit we pay out in total goes up compared to the previous year.

Source of the statistics

We take a sample of benefit claims from our administrative systems. DWP’s Performance Measurement (PM) team contact the benefit claimants to arrange a review. The outcomes of these reviews are recorded on a bespoke internal database called FREDA. We use data from here to produce our estimates.

We also use other data to inform our estimates – for example:

- benefit expenditure data (aligning with the Spring Budget published forecasts).

- benefit recovery data (DWP benefits and Housing Benefit) to allow us to calculate estimates of net loss.

- other DWP data sources and models to improve the robustness of, or categorisations within, our estimates – for example, to allow us to see if claimants who leave benefit as a consequence of the fraud and error review process then return to benefit shortly afterwards, and to understand the knock-on effect of fraud and error on disability benefits on other benefits.

Further information on the data we use to produce our estimates is contained within section 4, section 5 and section 6 of this report.

Definitions and terminology within the statistics

The main publication presents estimates of Fraud, Claimant Error, and Official Error. The definitions for these are as follows:

- Fraud: This includes all cases where the following three conditions apply:

- the conditions for receipt of benefit, or the rate of benefit in payment, are not being met

- the claimant can reasonably be expected to be aware of the effect on entitlement

- benefit stops or reduces as a result of the review

- Claimant Error: The claimant has provided inaccurate or incomplete information, failed to report a change in their circumstances, or failed to provide requested evidence, but there is no fraudulent intent on the claimant’s part.

- Official Error: The benefit has been paid incorrectly due to a failure to act, a delay or a mistaken assessment by DWP, a local authority or HMRC, to which no one outside of that department has materially contributed

We report overpayments (where we have paid people too much money), and underpayments (where we have not paid people enough money).

We present these in percentage terms (of expenditure on a benefit) and in monetary terms, in millions of pounds.

We also report a measure on the percentage of cases with Fraud or an overpayment Error calculated as follows:

Proportion of claims with an overpayment or underpayment (reference tables 12 and 13):

Proportion of claims with Fraud or an overpayment error = (number of claims in the sample with at least one Fraud or at least one overpayment error) / (number of claims in the sample)

Proportion of claims with an underpayment error = (number of claims in the sample with at least one underpayment error) / (number of claims in the sample)

Since the same claim can be included in both the proportion of claims with an overpayment error or Fraud and the proportion of claims with an underpayment error, these figures cannot be summed together to obtain the total proportion of claims paid incorrectly.

Proportion of claims paid the incorrect amount (reference table 11):

Proportion of claims overpaid = (number of claims in the sample ultimately overpaid) / (number of claims in the sample)

Proportion of claims underpaid = (number of claims in the sample ultimately underpaid) / (number of claims in the sample)

These figures can be summed together to obtain the total proportion of claims paid incorrectly. Further information about the types of errors we report on, abbreviations commonly used and statistical methodology can be found in the appendices at the end of this document.

Revisions to the statistics

Revisions to our statistics may happen for a number of reasons. When we make methodology changes that impact our estimates, we may revise the estimates for the previous year to allow meaningful comparisons between the two. Where we introduce major changes, we may denote a break in our time series and recommend that comparisons are not made back beyond a certain point.

In our FYE 2024 publication we have revised:

- the monetary value and rates of overpayments across the benefits for FYE 2023

- the proportion of cases overpaid and incorrect across the benefits for FYE 2023

- the proportion of Universal Credit (UC) cases with at least one Fraud overpayment in FYE 2023

For more information and the reason behind the revisions please see section 2.

The National Statistics Code of Practice allows for revisions of figures under controlled circumstances: “Statistics are by their nature subject to error and uncertainty. Initial estimates are often systematically amended to reflect more complete information. Improvements in methodologies and systems can help to make revised series more accurate and more useful.”

Unplanned revisions of figures in reports in this series might be necessary from time to time. Under this Code of Practice, the Department has a responsibility to ensure that any revisions to existing statistics are robust and are freely available, with the same level of supporting information as new statistics.

Status of the statistics

National statistics

National Statistics are accredited official statistics. National Statistics status means that these statistics meet the highest standards of trustworthiness, quality and public value, and there is a responsibility to maintain compliance with these standards.

These official statistics were independently reviewed by the Office for Statistics Regulation in December 2017. They comply with the standards of trustworthiness, quality and value in the Code of Practice for Statistics and should be labelled ‘accredited official statistics’. Our statistical practice is regulated by the Office for Statistics Regulation (OSR).

OSR sets the standards of trustworthiness, quality and value in the Code of Practice for Statistics that all producers of official statistics should adhere to.

You are welcome to contact us directly at enquiries.fema@dwp.gov.uk with any comments about how we meet these standards.

Alternatively, you can contact OSR by emailing regulation@statistics.gov.uk or via the OSR website.

Read further information about National Statistics on the UK Statistics Authority website.

Quality Statement

Quality in statistics is a measure of their ‘fitness for purpose’. The European Statistics System Dimensions of Quality provide a framework in which statisticians can assess the quality of their statistical outputs. These dimensions of quality are relevance, accuracy and reliability, timeliness, accessibility and clarity, and comparability and coherence.

Section 6 gives information on the application of these quality dimensions to our fraud and error statistics.

Feedback

We welcome any feedback on our publication. You can contact us at: enquiries.fema@dwp.gov.uk

Lead Statistician: Adam Pearce

DWP Press Office: 020 3267 5144

Report Benefit Fraud: 0800 854 4400

Useful links

Releases of Fraud and error in the benefit system statistics.

1. Introduction to our measurement system

The main statistical release and reference tables and charts provide estimates of fraud and error for benefit expenditure administered by the Department for Work and Pensions (DWP). This includes a range of benefits for which we derive estimates using different methods, as detailed below. For further details on which benefits are included in the total fraud and error estimates please see Appendix 2. More information can be found on the GOV.UK website about the benefit system and how DWP benefits are administered.

The fraud and error estimates provide estimates for the amount overpaid or underpaid in total and by benefit, broken down into the types of Fraud, Claimant Error and Official Error for benefits reviewed this year.

Estimates of fraud and error for each benefit have been derived using three different methods, depending on the frequency of their review (see section 5 for details):

Benefits reviewed this year

Fraud, Claimant Error and Official Error (see definitions above) have been measured for FYE 2024 for Universal Credit (UC), Housing Benefit (HB), Disability Living Allowance (DLA), Pension Credit (PC), State Pension (SP) and Personal Independence Payment (PIP).

Expenditure on measured benefits accounted for 83% of all benefit expenditure in FYE 2024.

Estimates are produced by statistical analysis of data collected through annual survey exercises, in which independent specially trained staff from the Department’s Performance Measurement (PM) team review a randomly selected sample of cases for benefits reviewed this year. See section 4 for more information on the sampling process.

The review process involves the following activity:

-

previewing the case by collating information from a variety of DWP or Local Authority (LA) systems to develop an initial picture and to identify any discrepancies between information from different sources

-

interviewing the claimant (or a nominated individual where the claimant lacks capacity) using a structured and detailed set of questions about the basis of their claim. The interview is completed as a telephone review in the majority of cases. However, where this is not appropriate, there is usually also the option for a completed review form to be returned by post

-

the interview aims to identify any discrepancies between the claimant’s current circumstances and the circumstances upon which their benefit claim was based

If a suspicion of Fraud is identified, an investigation is undertaken by a trained Fraud Investigator with the aim of resolving the suspicion.

Benefits were measured with different sample periods, although all were contained within the period November 2022 to October 2023, except for PIP and DLA, which ran from November 2022 to August 2023 and Feb 2023 to September 2023 respectively. For more information on the sample period for individual benefits please see Annex 1 of the statistical report. The following number of benefit claims were sampled and reviewed by the PM team:

| Benefit | Sample size | Percentage of claimant population reviewed |

|---|---|---|

| Universal Credit | 3,989 | 0.09% |

| State Pension | 1,557 | 0.01% |

| Housing Benefit | 3,001 | 0.13% |

| Pension Credit | 1,989 | 0.15% |

| Daily Living Allowance | 1,385 | 0.11% |

| Personal Independence Payment | 1,395 | 0.06% |

| Total | 13,313 | 0.06% |

Overall, approximately 0.06% of all benefit claims in payment were reviewed by the PM team.

Read information about the Performance Measurement Team.

Benefits reviewed previously

Since 1995, the Department has carried out reviews for various benefits to estimate the level of fraud and error in a particular financial year following the same process outlined above. In FYE 2024 around 11% of total expenditure related to benefits reviewed in previous years. Please see Appendix 2 for details of benefits reviewed previously.

Benefits never reviewed

The remaining benefits, which account for around 6% of total benefit expenditure, have never been subject to a specific review. These benefits tend to have relatively low expenditure which means it is not cost effective to undertake a review. For these benefits the estimates are based on assumptions about the likely level of fraud and error (for more information please see section 5).

2. Changes to the statistics this year

This section provides detail of changes for the FYE 2024 publication. Any historical changes can be found in Appendix 5.

Changes

Changes to benefits reviewed

Each year we use decision making methodology called multiple-criteria decision analysis (MCDA) to help evaluate which benefits will be reviewed.

For FYE 2024 we have measured DLA for the first time since FYE 2005 and stopped the measurement of ESA.

Unfulfilled Eligibility

From this year onward, estimates that were previously published as Claimant Error underpayments within the fraud and error statistics have been reclassified and are published separately as Estimates of Unfulfilled Eligibility. This follows a planned review of the fraud and error statistics to align the statistics more closely with benefit legislation. The review determined that the estimates previously published as Claimant Error underpayments should not be defined as underpayments. In benefit legislation, claimants are not eligible for increases in their benefit until they accurately report their circumstances to the department.

Unfulfilled eligibility refers to claimants who are already in receipt of a certain benefit but may not be getting the full award they could be eligible for on this benefit. This is not the same as take-up of benefits, which is where people could have claimed certain benefits based on their current circumstances but have not done so. The department also publishes statistics about take-up of benefits. For more information, please go to our publication regarding Estimates of Unfulfilled Eligibility.

Extra check on Failure to provide evidence cases

This relates to cases where the claimant has participated in the benefit review but has then failed to send in the requested evidence and subsequently had their claim to benefit terminated for failing to comply.

There is already an adjustment done on these cases where we look four months after their claim was terminated to see if we can find any evidence that would allow us to reclassify the fraud to a known error reason. This year we expanded this adjustment to see if we can find any evidence that would allow us to remove the fraud entirely on some of these cases (for example if we can see evidence of earnings coming through RTI the month after the benefit was terminated, which would have meant their Universal Credit entitlement went to zero). Applying these extra checks to the FYE 2023 statistics removed just over £100m of the “Failure to Provide Evidence/Engage” Fraud on Universal Credit. All other benefits were unaffected.

Change to the recording of Deemed Errors

In previous years, deemed errors were recorded, which are official errors where evidence that was available to the department when the award of benefit was made has been misplaced or is not available. When this happened, it means that the official error check could not be completed. Any case that had a deemed error raised against it was excluded from the calculation of the official error rate (but may still be counted in the calculation of Claimant Error and Fraud).

This year rather than record a deemed error, an estimated outcome is recorded instead, and the case is retained in the calculation of Official Error. We estimate that had this change been carried out last year it would not have changed the reported figures.

3. Interpretation of the results

Care is required when interpreting the results presented in the main report:

- the estimates are based on a random sample of the total benefit caseload and are therefore subject to statistical uncertainties. This uncertainty is quantified by the estimation of 95% confidence intervals surrounding the estimate. These 95% confidence intervals show the range within which we would expect the true value of fraud and error to lie

- when comparing two estimates, users should take into account the confidence intervals surrounding each of the estimates. The calculation to determine whether the results are significantly different from each other is complicated and takes into account the width of the confidence intervals. We perform this robust calculation in our methodology and state in the report whether any differences between reporting years are significant or not

- unless specifically stated within the commentary in the publication or in the reference tables, none of the changes for benefits reviewed this year are statistically significant at a 95% level of confidence when compared to the previous measurement

As well as sampling variation, there are many factors that may also impact on the reported levels of fraud and error and the time series presented:

- these estimates are subject to statistical sampling uncertainties. All estimates are based on reviews of random samples drawn from the benefit caseloads. In any survey sampling exercise, the estimates derived from the sample may differ from what we would see if we examined the whole caseload. Further uncertainties occur due to the assumptions that have had to be made to account for incomplete or imperfect data or using older measurements

- the sample year and the financial year do not align. This means that a proportion of expenditure for benefits reviewed this year cannot be captured by the sampling process. This is mainly because of the delay between sample selection and the interview of the claimant, and also the time taken to process new benefit claims, which excludes the newest cases from the review. The estimates in the reference tables in this release have been extrapolated to account for the newest benefit claims which are missed in the benefit reviews and cover all expenditure

- the estimates do not encompass all fraud and error. This is because Fraud is, by its nature, a covert activity, and some suspicions of Fraud on the sample cases cannot be proven. For example, cash in hand earnings are harder to detect than those that get paid via PAYE. Complex official error can also be difficult to identify. More information on omissions can be found later in this section

- some incorrect payments may be unavoidable. The measurement methodology will treat a case as incorrect, even where the claimant has promptly reported a change and there is only a short processing delay

Omissions from the estimates

The fraud and error estimates do not capture every possible element of fraud and error. Some cases are not reviewed due to the constraints of our sampling or reviewing regimes (or it is impractical to do so from a cost or resource perspective), some cases are out of scope of our measurement process, and some elements are very difficult for us to detect during our benefit reviews. The time period that our reviews relate to means that any operational or policy changes in the last five months of the financial year are usually not covered by our measurements.

For most omissions from our estimates, we make adjustments or apply assumptions to those cases. For some omissions we assume that the levels of fraud and error for those cases are the same as for the cases that we do review, and for other omissions we apply specific assumptions where we expect the levels of fraud and error to be different.

This section details the omissions from the estimates as far as possible. The examples that follow are not an exhaustive list but are an attempt at providing further details on known omissions in the estimates.

There are a number of groups of cases that we are unable to review or which we do not review. Some of the main examples of these are as follows:

New and short-term cases

We are unable to review short duration cases (of just a few weeks in duration) due to the time lags involved in accessing data on the benefit caseloads, drawing the samples and preparing these for reviewing. For these cases, we assume the rates of fraud and error are the same as in the rest of the benefit caseloads. We do, however, also make an adjustment using “new cases factors” to try to ensure that the results are representative across the entire distribution of lengths of benefit claims (see section 5 for further details).

It can take time for new cases to be available for sampling, meaning they are potentially under-represented in the sample. Analysis was undertaken to quantify the impact of these potential exclusions.

New cases make up a small proportion of cases for most benefits. The table below shows the yearly average percentage that are less than three months old at a given time.

| Benefit | Average number of cases less than 3 months old | Source |

|---|---|---|

| Pension Credit | 2.5% | Official quarterly data for August 2022 to May 2023 |

| Disability Living Allowance | 1.7% | Official quarterly data for August 2022 to May 2023 |

| Personal Independence Payment | 4.1% | Official monthly data for November 2022 to October 2023 |

| Housing Benefit | 3.9% | Official monthly new case data September 2022 to August 2023 |

| Universal Credit | 7.8% | Official monthly data for December 2022 to November 2023 |

| State Pension | 0.7% | Estimated using quarterly pension data for May 2022 and ONS population data |

To investigate the impact of this exclusion, a simulation of the sampling process was performed and repeated multiple times with these cases included. Sensitivity analysis was then carried out across all benefits to estimate the impact of excluding new cases if the error rate were doubled, halved, or remained the same.

The age of a case when it becomes available for sampling differs by benefit. Based on these timescales, analyses were undertaken using an exclusion period of either 6 weeks or 3 months.

Overall, this analysis showed that, because short term cases make up such a small percentage of total cases at any given time and many are available to be sampled later in the period, the impact on final published figures for all benefits is negligible.

The impact of excluding new cases is no more than 0.2 percentage points difference in the estimated error rate for either underpayment or overpayment across all benefits except UC. For UC overpayments, the scenario of doubling the error rate increases the total overpayment rate by 0.4 percentage points and halving the error rate decreases it by 0.2 percentage points. The higher numbers reflect the fact that UC has a higher proportion of new cases and a higher rate of error than other benefits.

It would be expected that the rate of fraud and error in new cases would typically be lower than the full population of claimants since they have recently been assessed. The outcomes of this analysis fall within the estimated confidence intervals and there is little impact on the published statistics, therefore no adjustment is required.

Unclaimed Benefits

We are only able to sample claimants who are in receipt of a benefit payment. Eligible claimants that have not made a benefit claim are not included in these figures. Find statistics on benefit take-up.

Disallowed claims

Claims which do not receive an award are not included in our sample. These claims may have been disallowed in error, resulting in a possible underpayment.

Using data on the number of disallowed claims and appeal success rates, sensitivity analysis was carried out to investigate the impact of various assumed error rates for disallowed cases.

A summary across benefits for various error rate scenarios is shown below. The worst-case scenario is not plausible and is included to illustrate that even assuming an unrealistic level of error, the adjusted estimate would still fall within or close to the published confidence intervals.

Results show that there is likely to be little to no impact on our estimate of underpayments as a result of not sampling disallowed claims.

Disability Living Allowance

| Level of underpayment in excluded group | Estimated change in underpayment | Impact on DLA underpayment estimate | Impact on global underpayment estimate |

|---|---|---|---|

| Extreme worst case: appeal success rate applied to all disallowed claims | + £44.4m | + 0.7 p.p | + 0.0 p.p |

| Disallowed cases have the same error rate as measured cases | + £2.6m | + 0.0 p.p | + 0.0 p.p |

Personal Independence Payment

| Level of underpayment in excluded group | Estimated change in underpayment | Impact on PIP underpayment estimate | Impact on global underpayment estimate |

|---|---|---|---|

| Extreme worst case: All disallowed cases are appealed with the same success rate | + £238.7m | + 1.1 p.p | + 0.1 p.p |

| Disallowed cases have the same error rate as measured cases | + £11.6m | + 0.1 p.p | + 0.0 p.p |

Note: PIP worst case analysis is slightly different due to its high appeal rate.

Pension Credit

The data on disallowed cases shows a steep increase in the proportion of cases declined with no award which happened in FYE 2021 and is continuing into the current financial year. Rejection rates in FYE 2021 and FYE 2022 have been affected by the financial strain people experienced due to the pandemic, causing more ineligible people to try and claim the benefit. Furthermore, following the recent government campaign published in April 2022, urging eligible pensioners to apply for Pension Credit, there has been an even larger increase in the volume of claims received by Department for Work and Pensions. In the meantime, many financial journalists started encouraging people to apply without checking the eligibility criteria due to the complex nature of the benefit. This meant that many people who were not eligible for Pension Credit tried to claim anyway, naturally increasing the rejection rate throughout FYE 2023 and FYE 2024. Therefore, we were not able to use this year’s and last year’s rejection rate in our sensitivity analysis and the last accurate rejection rate for our sensitivity analysis has been obtained from FYE 2020. If we used the most recent rejection rate, we would be overestimating the impact due to a larger number of ineligible claimants being rejected with no award.

| Level of underpayment in excluded group | Estimated change in underpayment | Impact on PC underpayment estimate | Impact on global underpayment estimate |

|---|---|---|---|

| Extreme worst case: appeal success rate applied to all disallowed claims | + £21.7m | + 0.4 p.p | + 0.0 p.p |

| Disallowed cases have the same error rate as measured cases | + £4.9 m | + 0.1 p.p | + 0.0 p.p |

| Twice as many cases are eligible to be awarded on reconsideration as actually are | + £1.1m | +0.0 p.p | + 0.0 p.p |

Universal Credit

Appeals information was not available for UC therefore the sensitivity analysis could not be carried out fully as in the above tables.

Using numbers of disallowed cases, analysis shows that even if the error rate in disallowed cases was double that found in the sample, the total difference in the UC rate would be around £7.7 million, or 0.0% of expenditure, and therefore well within the confidence interval – no adjustment is appropriate.

State Pension

Recent data was not available on the number of disallowed State Pension claims, however, given the data available it is expected to be very low. For the most recent year for which data on appeal rates was available (November 2022 to October 2023),applying sensitivity analysis based on a series of reasonable worst-case assumption showed that even if the error rate in disallowed cases was double that found in the sample, the total difference in the State Pension rate would be £0.2 million, which is negligible. Looking at the worst-case scenario, where all disallowed claims (even the ones that were not challenged) are reconsidered with the same error rate that was found in the sample, the total difference in the State Pension rate would be £4 million, or 0.0% of the expenditure. Therefore, no adjustment is required.

Housing Benefit

Applications for Housing Benefit are processed by local authorities, not centrally by DWP as with the other benefits reviewed, and it was not possible to obtain numbers of disallowed cases.

Since analyses of other benefits has shown negligible impact in excluding disallowed claims, the assumption is made that the impact on Housing Benefit is also negligible.

In conclusion, no adjustments are required to the estimates to account for the exclusion of disallowed cases from the sample.

Nil payment claims

A case is considered to be nil-payment if there is a claim in place but the total award being paid is zero. These cases are not included when the sample is selected. Some benefits do not allow a nil-award, meaning all active claimants are receiving some payment.

| Nil-award allowed | No nil-award allowed |

|---|---|

| Pension Credit | Housing Benefit |

| Universal Credit | State Pension |

| - | Personal Independence Payment |

Note: For a very small proportion of the PIP caseload (0.2%), the combination of award rates (daily living and mobility) is reported as nil-nil. Investigations suggest that award rates may be temporarily shown as nil for a short period whilst a claim review is in process, after which the new award rate is set. These cases will be monitored.

Nil-payment claims are a potential source of underpayment that is not included in the sample.

Pension Credit

Only a very small percentage of Pension Credit claimants are in nil-payment at any given time. For the most recent year of data available this number was always below one fifth of one percent. Simulating the sampling process shows that over 99.8% of cases sampled would be the same even if the nil-payment cases were included in the group available for sampling. The potential impact of a different error rate in this group thus rounds to zero, even in a worst-case scenario of doubling the error rate in the excluded cases.

Universal Credit

For the year up until August 2023 the most recent year for which data was available for analysis, the number of nil-payment claims ranged from 9.5% to 12.3%, with 11.0% being the average. Simulating the sampling process shows around 11.0% of claims that would otherwise be sampled are missed due to this. The potential impact of a different error rate in this group is a decrease of 0.1 percentage points if the error rate is half the measured rate, and an increase of 0.2 percentage points if the error rate in this group is double the measured rate.

Exclusions specific to PIP

The monthly samples are taken from live PIP claims in advance of the scheduling of the benefit reviews. Any benefit record relating to a claimant who meets specific exclusion criteria (for example, terminally ill, reviewed in the last three months) will not be reviewed. We assume the rates of fraud and error for these cases are the same as the rest of the PIP caseload. The potential impact of each excluded group are summarised below.

Terminally Ill cases

Terminally ill claimants make up a very small percentage of PIP claimants, typically around 1%. Sensitivity analysis was carried out to test the impact of their exclusion if the fraud and error rate on these cases were to differ by as much as double that of the sampled population.

Estimated impact of excluding terminally ill cases on the PIP overpayment rate

| Level of overpayment in excluded group | Estimated change in overpayments | Impact on PIP overpayment estimate | Impact on global overpayment estimate |

|---|---|---|---|

| Double the published rate | + £0.8m | 0.0 p.p | 0.0 p.p |

| Half the published rate | - £0.4m | 0.0 p.p | 0.0 p.p |

Estimated impact of excluding terminally ill cases on the PIP underpayment rate

| Level of underpayment in excluded group | Estimated change in underpayments | Impact on PIP underpayment estimate | Impact on global underpayment estimate |

|---|---|---|---|

| Double the published rate | £0.0m | 0.0 p.p | 0.0 p.p |

| Half the published rate | £0.0m | 0.0 p.p | 0.0 p.p |

Note that the PIP underpayment analysis applies to cases that are not on the highest award (enhanced mobility with enhanced daily living) as the estimates are already adjusted to account for this exclusion. See the Benefit-specific adjustments section for more details.

The above analysis demonstrates that any additional fraud or error that may exist in the excluded PIP terminally ill cases is extremely small. The total estimated levels of fraud and error would have a negligible difference for the above scenarios if terminally ill cases were included in the sample. Therefore, no adjustment has been made to the statistics because of this exclusion.

Scheduled reviews

PIP awards are reviewed regularly. The period between reviews is set on an individual basis and ranges from 9 months to 10 years, with the majority of claimants having a short-term award of 0-2 years. If a claim has had a planned award review in the last 92 days, has a review ongoing or a review due in the next six weeks then it is not eligible to be sampled.

A simulation of the sampling process was performed and repeated multiple times to investigate the impact of this exclusion.

Cases with an upcoming review would be expected to have a higher propensity for Fraud or Error due to the length of time since their last review. By the same reasoning cases that have had a review completed recently would be expected to have a lower propensity for Fraud or Error.

In our statistics an assumption is made that the excluded cases are similar to those sampled and so no adjustments are made. We investigated the impact of alternative assumptions on our estimates and results are shown in the table below.

In these scenarios it was assumed that an award that was increased after a planned review would have an underpayment had we reviewed it, and cases that were decreased or reviewed before being disallowed would have an overpayment. For overpayments, these proportions were taken from PIP data published via StatXplore and fed into the results below.

Estimated impact of excluding cases with a review that is due, ongoing, or recently completed using review outcomes to estimate fraud and error rates

For PIP overpayments, the vast majority of error was Claimant Error. Therefore, for this analysis we assumed zero error on the recently reviewed claims that were excluded from the sample, given that a recent review would resolve potential Claimant Error. A worst-case scenario of half the sampled error existing in the excluded recently reviewed cases was also estimated.

Therefore, for overpayments two assumptions were tested for recently reviewed cases: that they have no errors, and that they have half the error rate as our sample. The table below shows these assumptions and their estimated difference to the published amounts and rates.

Overpayments

| Estimated difference from published | Impact on PIP estimate | Impact on global estimate | |

|---|---|---|---|

| Assumption of zero error on excluded recently reviewed cases | £7.0m | 0.3 p.p | 0.0 p.p |

| Assumption of half the sampled error on excluded recently reviewed cases | £14.7m | 0.3 p.p | 0.0 p.p |

As this publication focuses on Official Error underpayments only, a different method of analysis on excluded cases was applied for underpayments. We were unable to split the available review outcome data down into type of error, therefore applied a simplified calculation based on the sampled Official Error estimates for underpayments.

For underpayments, we assumed that Official Error is likely to occur in the excluded recently reviewed cases in the same way as for our sampled cases. Therefore, we have estimated the impact of the excluded cases having half the error as the sample, and as a worst-case scenario having double the error as the sampled cases.

Therefore, for underpayments two assumptions were tested for recently reviewed cases: that they have half the sampled error, and that they have double the error as our sample. The table below shows these assumptions and their estimated difference to the published amounts and rates.

Underpayments

| Estimated difference from published | Impact on PIP estimate | Impact on global estimate | |

|---|---|---|---|

| Assumption of half the sampled error on excluded recently reviewed cases | -£8.0m | 0.0 p.p | 0.0 p.p |

| Assumption of double the error on excluded recently reviewed cases | £16.2m | 0.1 p.p | 0.0 p.p |

These differences all fall within the published confidence intervals for the rates of overpayment and underpayment for PIP in FYE 2024, and the conclusion therefore is no adjustment is needed.

Exclusions specific to DLA

The monthly samples are taken from live DLA claims in advance of the scheduling of the benefit reviews. Any benefit record relating to a claimant who meets specific exclusion criteria (e.g., terminally ill, reviewed in the last three months) will not be reviewed. We assume the rates of fraud and error for these cases are the same as the rest of the DLA caseload. The potential impacts of each excluded group are summarised below.

Working age cases

DLA is being replaced by other benefits. New claims to DLA can only be made for children.

Adults of working age and pensioners aged 65 or over prior to 8 April 2013 (DLA 65+), already in receipt of DLA, will continue to get DLA as long as they remain eligible for it.

We have reviewed claims for children and DLA 65+ only. Working age cases are not being reviewed due to being unable to measure a change in rate – DLA working age cases with a change in circumstances have their DLA payments ended and must claim PIP instead. We exclude current pensioners who were under 65 on 8th April 2013 who would also have their DLA payment ended if a change of circumstances was found and they would have to claim PIP. Working age cases account for about 15% of all DLA cases. We considered what proxy to use for the unmeasured working age element of DLA. Analysis of rate combinations of each client group suggests that a combination of Children and 65+ rates, weighted by population factor, best match the working age claimants’ rate. However, lack of review for those cases prevents a more accurate assessment.

As DLA working age claims with a change in circumstances cannot be measured, we have excluded them from our sensitivity analyses and adjustments.

Terminally ill cases

Terminally ill claimants make up a very small percentage of DLA claimants, typically less than 1%.

Sensitivity analysis was carried out to test the impact of their exclusion if the fraud and error rate on these cases were to differ by as much as double that of the sampled population.

Estimated impact of excluding terminally ill cases on the DLA overpayment rate

| Level of overpayment in excluded group | Estimated change in overpayments | Impact on DLA overpayment estimate | Impact on global overpayment estimate |

|---|---|---|---|

| Double the published rate | £0.1m | 0.0 p.p | 0.0 p.p |

| Half the published rate | £0.0m | 0.0 p.p | 0.0 p.p |

Estimated impact of excluding terminally ill cases on the DLA underpayment rate

| Level of underpayment in excluded group | Estimated change in underpayments | Impact on DLA underpayment estimate | Impact on global underpayment estimate |

|---|---|---|---|

| Double the published rate | £0.0m | 0.0 p.p | 0.0 p.p |

| Half the published rate | £0.0m | 0.0 p.p | 0.0 p.p |

Note that DLA claims on the highest rate award (higher rate mobility and high care) have been excluded from this analysis as they can’t be underpaid.

The above analysis demonstrates that any additional fraud or error that may exist in the excluded DLA terminally ill cases is extremely small. The total estimated levels of fraud and error would have a negligible difference for the above scenarios if terminally ill cases were included in the sample. Therefore, no adjustment has been made to the statistics because of this exclusion.

Scheduled reviews

DLA claims for children are reviewed on renewal, however DLA 65+ awards are not routinely reviewed. Around 18% of the sample was abandoned due to cases having a scheduled review or a recent review, and they were therefore excluded from the sample estimates.

In our statistics an assumption is made that the excluded cases are similar to those sampled and so no adjustments are made. We investigated the impact of alternative assumptions on our estimates and results are shown in the table below.

Estimated impact of excluding cases with a review that is due, ongoing, or recently completed using review outcomes to estimate fraud and error rates

Overpayments

For DLA overpayments two assumptions were tested for cases excluded as recently reviewed or having a scheduled review. We have estimated the impact of the excluded cases having half the error as the sample, and as a worst-case scenario having double the error as the sampled cases. The table below shows these assumptions and their estimated difference to the published amounts and rates.

| Estimated difference from published | Impact on DLA estimate | Impact on global estimate | |

|---|---|---|---|

| Assumption of double the sampled error on excluded recently reviewed cases | £5.3m | 0.1 p.p | 0.0 p.p |

| Assumption of half the sampled error on excluded recently reviewed cases | -£2.6m | 0.0 p.p | 0.0 p.p |

Cases with an upcoming review would be expected to have a higher propensity for Fraud or Claimant Error due to the length of time since their last review. By the same reasoning, cases that have had a review completed recently would be expected to have a lower propensity for Fraud or Claimant Error. Official Error is assumed to be the same regardless of recent or scheduled reviews.

Given these assumptions, and the fact that both types of reviews are present in the excluded proportion, the impact of double the sample estimate occurring in the excluded proportion is extremely unlikely and a worst-case scenario.

Underpayments

For DLA underpayments two assumptions were tested for cases excluded as recently reviewed or having a scheduled review. We have estimated the impact of the excluded cases having half the error as the sample, and as a worst-case scenario having double the error as the sampled cases. The table below shows these assumptions and their estimated difference to the published amounts and rates.

| Estimated difference from published | Impact on DLA estimate | Impact on global estimate | |

|---|---|---|---|

| Assumption of double the sampled error on excluded recently reviewed cases | £12.3m | 0.2 p.p | 0.0 p.p |

| Assumption of half the sampled error on excluded recently reviewed cases | -£6.2m | - 0.1 p.p | 0.0 p.p |

These differences all fall within the published confidence intervals for the rates of overpayment and underpayment for PIP in FYE 2024, and the conclusion therefore is no adjustment is needed.

Fraud and error occurring directly on Cost of Living Payments

The estimate for Cost of Living Payments only includes fraud and error on the payments where the qualifying benefit was incorrectly paid. This means that we are omitting a small amount of fraud and error that can occur on the payment themselves. These include:

- a small number of Cost of Living Payments which were paid in error to the wrong person

- a number of claims that were incorrectly not paid Cost of Living Payments

The department estimates that the amount overpaid directly on Cost of Living Payments was small and well within the confidence intervals in FYE 2024. The amount underpaid directly on Cost of Living Payments would be negligible. Mop-up exercises are carried out on the cases incorrectly not paid, as soon as they are identified, and these cases are then paid at a later date.

Time Lags

The time lags involved in the fraud and error measurement process mean that further omissions are possible. Any policy or operational changes in the last five months of the financial year will not usually be covered by the reviews feeding into the publication, as the reviews tend to finish in the October of that financial year. In addition, some cases do not have a categorisation by the time the estimates are put together, often due to an ongoing fraud investigation. “Estimated outcomes” are generated for these cases for the purposes of the statistics, made by the review officer estimating the most likely outcome of the case, or based on the results from the reviews of similar cases that have been completed.

For all benefits we carried out additional work to better understand any implications of major policy/operational changes within the financial year. The conclusion was that we felt the sample period was representative of the financial year. See section 5 for further details.

Work Capability Assessment

When ESA was measured between FYE 2014 and FYE 2023, the measurement of ESA did not include a review of the Work Capability Assessment; this is also the case for the Work Capability Assessment for claimants on UC.

Universal Credit Transitional Protection

Universal Credit (UC) was introduced to replace older (legacy) benefits, including tax credits. Benefit claimants have gradually moved onto UC through:

- natural migration – when the claimant experiences a change in circumstances, and they need to make a new claim for a benefit that UC has replaced

- voluntary migration – when the claimant voluntarily moves to UC from their existing benefit

- managed migration – when the claimant does not choose to migrate voluntarily and has not migrated naturally

Transitional protection can be applied to claimants who are moved onto UC through the managed migration process. A transitional protection element is applied to ensure that eligible households, with a lower calculated award in UC than their legacy benefit awards, will see no difference in their entitlement at the time they are moved to UC, providing that there is no change in their circumstances during the migration process.

The transitional protection element is calculated during the managed migration process. It is based on the circumstances for the eligible household and their legacy benefits in payment that are being replaced by UC. There is potential for the transitional protection element to be paid incorrectly if the calculation is made incorrectly and/or the legacy benefit awards in payment are incorrect based on the claimant’s circumstances. We are unable to review the transitional protection element calculation or the legacy benefit awards because these can be derived from benefits not administered by DWP. Consequently, fraud and error on this element of UC is omitted from the estimates.

Latest figures on UC Transitional Protection seem to show there are around 85,000 UC cases with this element. For these cases the transitional protection only accounts for a small fraction of the total UC award in payment. Expenditure on the transitional protection element was low in FYE 2024 compared to the total UC expenditure. Therefore, the omission was taken to be negligible, and no adjustment was made to the UC fraud and error estimates.

Knock-on impact on other benefits

We only review the benefit that has been selected for a review, and do not assess any consequential impacts on other benefits. However, in certain circumstances, for some benefits, there may be a knock-on impact on other benefits. An example of this is how changes in entitlement to DLA or PIP affects disability and carer premiums on income-related benefits (specifically IS, PC and HB), as well as CA. We account for this in our estimates by using DWP’s Policy Simulation Model to assess the impact. The Policy Simulation Model is the main micro-simulation model used by DWP to analyse policy changes and is based on the annual Family Resources Survey. However, there are other knock-on impacts which we do not cover. For example, any benefit which considers another benefit as an income. If that other benefit is incorrect then only its impact on the benefit we measured is captured. This means that potentially the global figure is an overestimation as in these scenarios the overpayment on the benefit measured would be offset by an uncaptured underpayment on the other benefit.

Third party deductions

The accuracy of third party deductions is not measured (i.e. whether the deduction is at the correct amount and is still appropriate). Third party deductions can take place to cover arrears for things like housing charges, fuel and water bills, Council Tax and child maintenance. The rate of benefit is not impacted by any third party deductions, and the amount of any Fraud or Error is based on the “gross” amount of benefit in pay.

UC sanctions

For UC, we do not assess whether the Department follows correct “labour market” procedures and takes any necessary follow up action for non-compliance by claimants (i.e. considers whether a sanction should apply if a claimant fails to apply for a job or leaves a job voluntarily). However, if a sanction decision has already been made when we review a case, then we do assess whether the impact this has on the benefit award is correct.

UC surplus self-employed profit/loss

For UC, we only measure income in the assessment period we are checking. Self-employed people must report their income on a monthly basis. If they receive income that removes their entitlement to UC in one month, and this is above the surplus earnings threshold, then any extra income is carried forward into the next month (the surplus earnings threshold is defined as £2,500 above the amount that removes their entitlement to UC in that month). If a self-employed claimant incurs a loss of any amount within an assessment period, this loss is also rolled forward to the next assessment period. When reviewing the benefit, any rolled forward income or loss is assumed to be correct.

Earnings from the hidden economy

These are claimants who are working but are not declaring those earnings to the government. For every means tested benefit, where capital and earnings affect the award, we require bank statements for all the claimant’s accounts that cover the period of the payment we are checking. This means that any earnings which goes through the claimant’s bank are likely to be picked up when those bank statements are checked.

Although we think we capture most of the Fraud related to hidden economy earnings, it is likely that not all of this would end up under the “Earnings/Employment” error reason. If the claimant fails to send in bank statements after multiple prompts, then their benefit is suspended and ultimately terminated. In these circumstances a whole award Fraud would be recorded (see Causal Link part of section 5 for more information). However, given they were hiding their earnings from the Government it is likely we would not know the underlying reason so the Fraud would be categorised as “Failure to provide evidence/engage”.

This means that the only earnings we would not pick up are those which are only “cash in hand” and are not being deposited into a bank account. We expect the impact of this to be minimal, particularly since COVID-19, many cash only businesses have diversified into accepting bank transfers/card which further reduces this omission.

Cyber-crime

We do find errors relating to this and they would be included within the “Conditions of Entitlement” error reason. The benefit reviews that underpin the statistics are very robust and encompass not only a lengthy interview with the claimant but also evidence to verify all their circumstances. Therefore, it would be very difficult for a fraudulent claimant to meet all these requirements without alerting the suspicions of the reviewing officer.

Similar to hidden economy earnings, we think we capture most of the Fraud related to cyber-crime, but it is likely that not all of this would end up under the “Conditions of Entitlement” error reason. If a claim is fraudulent then they are likely to either not attempt the interview or not provide the requested evidence, in which case a whole award Fraud would be recorded (see Causal Link part of section 5 for more information). However, it is likely that we would have no evidence as to why they did this so the Fraud would be categorised as “Failure to provide evidence/engage”.

Benefit Advances

One of the largest current omissions from our estimates is benefit advances, which are out of scope of our measurement.

UC supports those who are on a low income or out of work. It includes a monthly payment to help with living costs. If a claim is made to UC but the claimant is unable to manage financially until their first payment, they may be able to get a UC Advance, which is then deducted a bit at a time from future payments of the benefit.

The benefit review process for the fraud and error statistics examines cases where benefit is in payment. A benefit advance is not a benefit payment and is not included in the DWP expenditure figures or in our measurement process. Claimants who progress to receive payment of a benefit will be included within the scope of our measurement, but we will only review the existing benefit payment. This will not examine Fraud or Error that may have existed in any prior benefit advance payment. Claimants who only receive a benefit advance, but do not go on to receive a subsequent benefit payment, will not be included within the measurement. Advances are available for a number of benefits but, for FYE 2024, advances for UC constituted the vast majority of expenditure on benefit advances.

We estimate that for FYE 2024 the monetary value of fraud and error on UC advances lies between £0m and £60m.

Rounding policy

In the publication and reference tables, the following rounding conventions have been applied:

- percentages are rounded to the nearest 0.1%

- expenditure values are rounded to the nearest £100 million

- headline monetary estimates are rounded to the nearest £10 million

- monetary estimates for error reasons are rounded to the nearest £1 million

The proportion of claims paid incorrectly is rounded to the nearest 1% in the publication and expressed in the format “n in 100 cases”. The reference tables present the same values as a percentage rounded to the nearest 0.1%.

Individual figures have been rounded independently, so the sum of component items do not necessarily equal the totals shown.

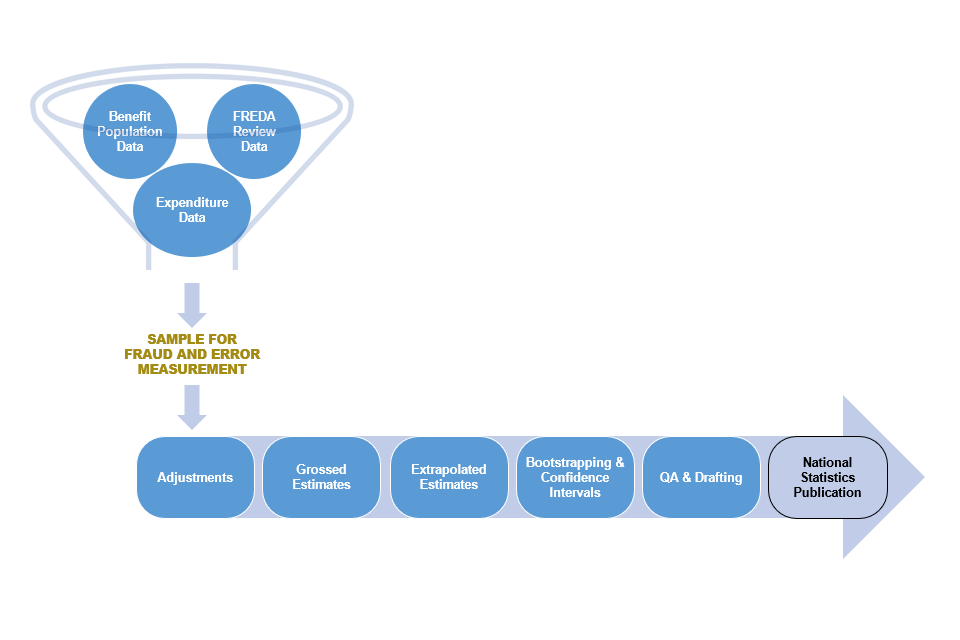

4. Sampling and Data Collection

The fraud and error statistics are determined using a sample of benefit records, since is it not possible to review every benefit record. The sample of benefit records provide data from which inferences are made about the fraud and error levels in the whole benefit claimant population.

The number of benefit records to be reviewed is determined by a sample size calculation. The sample size calculation is used to ensure that a sufficient number of benefit records are sampled, which allows meaningful changes in the levels of fraud and error to be detected for the whole benefit claimant population.

Benefit records are selected on a monthly basis from data extracts of the administrative systems. The population from which the samples are drawn are the benefit records that are in payment in a particular assessment period, that is where there is evidence of a payment relating to the previous month. This is known as the liveload.

The monthly samples are taken from the liveload in advance of the scheduling of the benefit reviews, to give time for the sample to be checked and for background information to be gathered on each benefit record sampled. Any benefit record relating to a claimant who has been previously sampled in the last 6 months, or meets specific exclusion criteria (e.g. terminally ill) will not be reviewed.

We use Simple Random Sampling to select the sample of benefit records for each benefit that is reviewed in the current year. Benefit records are sampled randomly to ensure an equal chance of being selected for the sample. The sampling methodology is used to attempt to minimise selection bias in the sample and aims to select a sample that is representative of the entire benefit claimant case population.

The benefits sampled for this year and the methodologies applied are as follows:

Simple random sample:

- Disability Living Allowance

- Pension Credit

- Universal Credit

- State Pension

- Personal Independence Payment

Housing benefit methodology uses simple random sampling stratified by Primary Sampling Unit (PSU) and four different client groups:

- Working Age in receipt of IS, JSA, ESA, PC or UC

- Working Age not in receipt of IS, JSA, ESA, PC or UC

- Pensioners in receipt of IS, JSA, ESA, PC or UC

- Pensioners not in receipt of IS, JSA, ESA, PC or UC

Note: for HB only the client groups “Pensioners in receipt of IS, JSA, ESA, PC or UC” and “Pensioners not in receipt of IS, JSA, ESA, PC or UC” were reviewed in FYE 2024.

Abandoned Cases

Of the benefit records sampled, there are some that are not eligible for a review according to strictly defined criteria for abandonment. Benefit records that fall into this category could include:

- the claimant has a change of circumstances that ends their award before the interview can take place

- the claimant has had a benefit reviewed in the last six months

- if the claimant or their partner is terminally ill

When such cases occur in the sample, they are replaced by another case from a reserve list. However, for a small number of abandoned cases replacement is not possible for practical reasons. This occurs when cases are abandoned towards the end of the review year, which means that there is not enough time for a replacement case to complete the full process.

Abandoned Cases FYE 2024

It is the decision of the Performance Measurement (PM) team, during the preview stage of a case, if a case should be abandoned.

Table showing the main reason for cases abandoned for each benefit

| Abandonment Reason / Benefit | DLA | HB | PC | PIP | SP | UC | Total |

|---|---|---|---|---|---|---|---|

| Benefit not in payment/ceased or suspended | 17 | 145 | 69 | 20 | 8 | 344 | 603 |

| New activity within 6 months of the start of the sample | 320 | – | – | 122 | – | – | 442 |

| Sensitive issues | 39 | 25 | 65 | 16 | 16 | 25 | 186 |

| Allowable Absence | 12 | 30 | 12 | 5 | 4 | 24 | 87 |

| Corporate appointee with no named contact | 6 | 4 | 18 | 34 | 1 | 8 | 71 |

| Miscellaneous | 38 | 71 | 31 | 60 | 59 | 138 | 397 |

| Total cases abandoned by benefit | 432 | 275 | 195 | 257 | 88 | 539 | 1,786 |

| Total cases reviewed | 1,385 | 3,001 | 1,989 | 1,395 | 1,557 | 3,986 | 13,313 |

| Abandonment rate per benefit | 31% | 9% | 10% | 18% | 6% | 14% | 13% |

| Percentage point change from previous year | – | -24 | 2 | 5 | 0 | -1 | -3 |

For FYE 2024, the abandonment reasons ‘Operational Issues’ & ‘Incorrectly Sampled’ have been added to the category ‘Miscellaneous’. This is due to other abandonment reasons accounting for a greater proportion of cases abandoned.

The five reasons listed (excluding ‘miscellaneous’) accounted for around 78% of total abandonment, a reduction in total proportion from FYE 2023. This is mainly due to less cases being abandoned within the ‘Benefit not in payment/ceased’ category accounted for 33% of the total abandonments in FYE 2024, compared with 62% in FYE 2023. This difference mainly comes from the change in HB client group measured between years.

DLA has been reviewed for the first time this year, as such there is no previous comparison to be made for abandonments.

For HB, FYE 2024 reviewed the pension age client groups for HB as opposed to the non passported working age client group in FYE 2023. Different client groups have variation in the rate of abandonment due to the nature of the benefits with non passported working age claimants most likely to move off benefit with earnings increasing.

Below are updated descriptions for the top five abandonment reasons for FYE 2024:

- Benefit not in Payment/ceased or suspended – this remains the largest cause of abandonment, with almost 60% of these abandonments being on UC claims. These are claims no longer in payment either because the claimant is no longer entitled to the benefit or because they are now claiming another benefit. This is primarily related to the time lag of benefit reviews commencing from sample selection period

- New activity within 6 months of the start of the sample – This reason is solely linked to the disability benefits. This is due to actions previously done or planned to be done on claimant’s case such as renewal of the claim to DLA or the claimant notifying a change to the department before the review process has started. For PIP, this could be appeals or interventions made on their claim

- Sensitive Issues – this is a reason that affects all benefits reviewed. The claimant/partner being terminally ill or finding out they recently became deceased or bereaved are the main causes for the usage of this reason

- Allowable Absence – This reason is when the claimant is under hospital care during the review week, with no known indication of when they would be able to complete the review or being out of the country

- Cooperate Appointee with no named contact – This reason has previously been included within ‘Miscellaneous’ in previous years. These claims relate to when the review has been planned and are unable to find the correct official to deal with the review on the claimant’s behalf

- Miscellaneous – this category covers all remaining categories of abandonment used. These reasons are within the pre-defined criteria for abandonment. All the reasons here are unavoidable, out of our control or can’t be identified at the sample production stage of the process

Official Error Checking

For all benefits that are not UC the week of the official error check is changeable and is decided by either the day the claimant is notified of the review or the date the review takes place. For UC, the check is usually for the last Assessment Period (of one month) prior to the date the review takes place.

Specially trained DWP benefit review officers carry out the checks. The claimant’s case papers and DWP computer systems are checked to determine whether the claimant is receiving the correct amount of benefit according to their presented circumstances. This identifies any errors made by DWP officials in processing the claim and helps prepare for the next stage: a telephone review of circumstances with the claimant.

Claimant Error and Fraud Reviews

For all benefits, benefit review officers normally check for Claimant Error (CE) or Fraud by comparing the evidence obtained from the review to that held by the Department. The claimant may not be interviewed if:

- the case is already under an ongoing fraud investigation

- a suspicion of Fraud arises while trying to secure an interview

When such cases occur in the sample, the outcome of the fraud investigation is used to determine the review outcome.

Where, following receipt of a letter informing them of a review, the claimant reports a change of circumstances that results in entitlement to that benefit ending before the review takes place, an outcome of Causal Link would be considered without the claimant being interviewed. See section 5 for information on Causal Link errors.

Types of errors excluded from our estimates

Types of errors:

- Some failures by DWP staff to follow procedures are not counted as official errors; where the failure does not have a financial impact on the benefit award or where the office have failed to take action which could have prevented a claimant error from occurring. These are called procedural errors

- Accounting errors are errors where, despite an error in the claimant’s benefit, an overpayment (or underpayment) of the benefit undergoing a check could be offset against any corresponding underpayment (or overpayment) on the same benefit or in the case of State Pension and Pension Credit each other. For State Pension and Pension Credit these errors are excluded from the monetary estimates but are included in estimates of the proportion of claims paid incorrectly. For errors where the offset is on the same benefit they are excluded completely

- A notional error is one where, following PM intervention, the claimant is advised to apply for State Pension or an occupational pension, but the claimant does not apply for it so the DWP decision maker assumes a ‘notional’ amount for this income based on the amount the claimant could receive if they apply for it. These notional amounts are taken into account from a future date so are excluded from our estimates

Recording Information

Case details relating to the fraud and error reviews are recorded on internal bespoke ‘fraud and error’ software (the system is known as FREDA), to create a centrally held data source. This can then be matched against our original sample population to produce a complete picture of fraud and error against review cases across our sample.

5. Measurement Calculation Methodology

Fraud and error measurement relies on three data sources:

- Raw Sample held on ‘FREDA’ (the database on which the review outcomes are recorded), is used to identify the Monetary Value of Fraud and Error (MVFE) for individual cases, categorise its cause and quantify it as a proportion of the sample

- Benefit Population data to estimate the extent of fraud and error across the whole claimant caseload from the sample data

- Expenditure data to estimate the total MVFE to the Department

Estimates are categorised into overpayments (OP) and underpayments (UP) and one of three incorrectness types: Claimant Fraud (CF), Claimant Error (CE) or Official Error (OE). Further sub-categories of error reasons are used to provide more details about the nature of the Fraud or Error. Details on error classifications can be found in the glossary at Appendix 3.

Detailed below are the main calculation steps that the Fraud & Error Measurement and Analysis (FEMA) team carry out to produce the final Fraud and Error estimates.

Methodology for Benefits reviewed this year

Benefits that have been reviewed this year account for 83% of the total benefit expenditure. For each of the benefits reviewed this year a random sample of cases was taken. See section 4 for further details.

An Official Error check is carried out; see Official Error Checking part of section 4. The claimant is then contacted, and a review carried out with evidence requested to verify their circumstances as outlined in Claimant Error and Fraud Reviews part of section 4.

Finally, a case is categorised as Benefit Correct, Official Error, Claimant Error or Fraud (or a combination of the last three).

There are specific scenarios and adjustments that we then take into account. These are detailed below:

Causal Link

Cases where there is a change to the claimant’s award as a result of the review activity or, after initial contact, the claimant subsequently fails to engage in the review process, are categorised as Claimant Fraud with causal link. Action is taken to suspend their payment and subsequently terminate their claim.

Examples of behaviours that can trigger cases to be categorised as Causal Link include:

- the claimant receives notification of the review and subsequently contacts the department to report an immediate change e.g. living with a partner, starting work, self-employment or capital changes. Then supporting evidence needed to verify the change is not provided, resulting in claim suspension and termination

- the claimant completes the review but subsequently declares that a change has happened shortly following the period of the review

- the claimant receives notification of the review and does not engage in the review process or contacts the department with a request to withdraw their claim

- the claimant completes a review and declares a change, however supporting evidence needed to verify the change is not returned, resulting in claim suspension and termination

For UC there are cases where the claimant fails to engage in the review process, but there is supporting evidence that a change is not due to the review. These are categorised as ‘mitigating circumstances’. For these cases, information is available on our systems to indicate why the person may not have engaged. In most cases, they have moved into paid work following the Assessment Period under review.

For all benefits post-review, every Causal Link error is categorised as either high suspicion or low suspicion. This categorisation is used in the netting and capping procedure (see below section Netting and Capping) to help attribute losses to the error reasons we are most confident about. Any losses attributed to low suspicion Causal Link after netting and capping will have their error reason changed to “Failure to provide evidence/fully engage in the process”.

Examples of high suspicion Causal Link errors include:

- shortly after review the claimant terminates their claim (rather than send in evidence)

- the claimant told us at the review of a change of circumstances, but we cannot confirm that the change occurred prior to (or in) the assessment period checked

- post-review, the claimant made a change of circumstances that cannot be confirmed as starting after the assessment period checked

- when asked to send in more information or to clarify further queries on evidence sent in, the claimant stops engaging

The main reason that we would class a case as low suspicion is where the claimant fails to send in evidence, but we have no prior suspicions of fraudulent intent.

Adjustments

A series of adjustments are made to the sample data, to allow for various characteristics of the benefits and how their data is collected and recorded.

The following table highlights which adjustments apply to each of the benefits reviewed in FYE 2024.

| SP | DLA | PC | HB | UC | PIP | |

|---|---|---|---|---|---|---|

| Netting and Capping | Y | Y | Y | Y | Y | Y |

| Estimated Outcomes | Y | Y | Y | Y | Y | Y |

| New Cases Factor | N | N | Y | Y | N | N |

| Underlying Entitlement | N | N | N | Y | N | N |

| Cannot Review Cases | Y | Y | Y | Y | Y | Y |

| Reasonably Expected to know | N | Y | N | N | N | Y |

Netting and Capping

Where a case has more than one error, these errors can be “netted off” against one another to produce a total value. For example, if a case is found to have two different OEs, one leading to an UP and one leading to an OP, then these are “netted off” to produce a single OP or UP. This is done to better represent the total monetary loss to the public purse (via OPs) or to the claimant (via UPs).

The monetary loss on each case is the difference between the case award paid at the review/assessment period, and the correct award calculated following the review – the “award difference”.

A case may have OPs of more than one ‘type’ which sum to a total greater than the award difference. To ensure that the total OP does not exceed the total award difference, we ‘cap’ the OP amount using a hierarchy order of actual CF, Causal Link (high suspicion) CF, Causal Link (low suspicion) CF, CE then OE. This capping process means that a small proportion of CE and OE found during the survey is not included in the estimates, and therefore the final estimates may actually be under-reporting CE and OE in the benefit system, but the total amount of fraud and error is correctly reported.

Estimated outcomes

For a number of cases reviewed this year, the review process had not been completed at the time of the analysis and production of results, often due to incomplete fraud investigations. As a result, predictions for the final outcomes for these cases have been made in the analysis using either the review officer (RO) estimation of the most likely outcome, or the results from the reviews of similar cases that had been completed.

New Cases Factors

New Cases Factors are an adjustment applied to help ensure that the durations on the sample accurately reflect the duration on benefit within the population.

As a result of the time required to collect the information needed to review a case, as well as other operational considerations, there is an unavoidable delay between sample selection and case review. This delay means that fewer low duration claims will be represented in the sample of cases, which artificially introduces a bias around claim durations at the point of interview.

Cannot Review

Cases that cannot be reviewed, primarily due to the claimant not engaging in the review process resulting in their benefit claim being suspended and later terminated, are initially recorded as Fraud. These cases are referred to as ‘Cannot Review’ and for most cases the Department holds very little evidence of their current circumstances and their reasons for failing to engage.

Not all of these cases will be Fraud so for cases where there is a lack of evidence available, additional checks are conducted at a later date. These checks are to determine if the individuals have reclaimed benefit and if there was a suspicion of Fraud recorded on the case at the initial preview. The outcome of these checks will result in these cases being re-categorised for reporting purposes. 0.8% of sampled cases in FYE 2024 did not have an effective review and we had no evidence as to why.

There are three different categories that are applied to cannot review cases for reporting purposes:

- Not Fraud – If the individual reclaims benefit within 4 months, with the same circumstances and at a similar rate they were receiving prior to review, then the Fraud is removed

- Fraud remains – If an individual does not reclaim benefit and there was a suspicion of Fraud raised at the preview stage of the review then the case remains as Fraud