Mortgage and landlord possession statistics: January to March 2021, supporting document

Published 13 May 2021

© Crown copyright 2021

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/statistics/mortgage-and-landlord-possession-statistics-january-to-march-2021/mortgage-and-landlord-possession-statistics-january-to-march-2021-supporting-document

1. Introduction

This document aims to provide a guide to the Mortgage and Landlord Possession claims, focusing on concepts and definitions published in Ministry of Justice mortgage and landlord possession statistics. It also covers overall statistical publication strategy, revision policies, data sources, quality and dissemination.

2. Background to Mortgage and Landlord Possession Actions

In England and Wales the process of possessing a property by a landlord or a mortgage lender is carried out by the county courts. This only happens as a last resort after all other options of recovering the money owed have been explored.

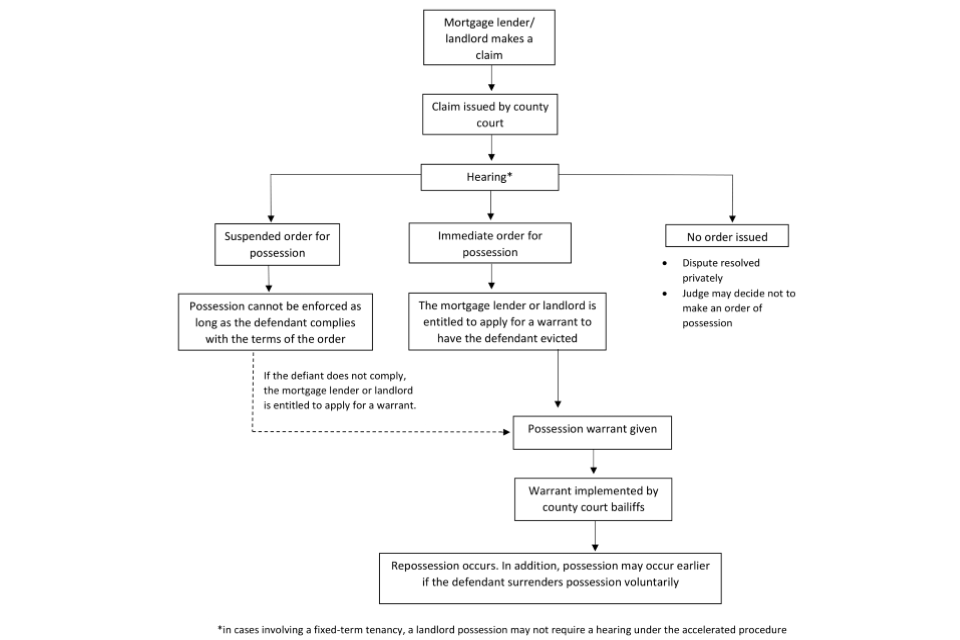

This section describes the court process of possessing a property in detail and Figure 1 provides a summary.

Figure 1: A simplified description of the main court processes for possession cases

To obtain a court order granting the entitlement to take possession of a property, a claimant – a mortgage lender or a landlord – must first make a claim for possession of property which is then issued by a county court. Generally, the issuing process involves the arrangement of an initial hearing before a judge. At such a hearing, a judge may:

- grant an order for outright possession of the property at a date decided by the judge;

-

grant a suspended order for possession of the property; or,

- grant no order for possession (for example, after deciding the claimant has no legal right to take possession of the property).

The suspended order for possession of the property usually requires the defendant to pay the latest mortgage or rent instalment, plus some of the arrears that have built up, within a certain defined period. As long as the defendant complies with the terms of the suspension, the possession order cannot be enforced.

More than one order may be granted during the course of an individual case. For example, it is possible that after an initial possession order is granted, a party may make an application to the court for the order to be varied or set aside, which could then result in another order being made.

The possession order states that that the defendant should vacate the property and that the claimant has entitlement to take possession of the property (and sometimes that costs must be paid). If the defendant will not permit or allow possession, a warrant can then be sought to have the defendant evicted by bailiffs, so taking possession of the property. Only then does a repossession occur, and is carried out in these cases by the county court bailiff.

Throughout the court process, even where a warrant for possession is issued, the claimant and defendant can still negotiate a compromise arrangement to prevent eviction. For background information about other types of civil claims within the County Court and more general information about the county court system, please see Civil Justice Statistics Quarterly.

3. Methodology

A mortgage or landlord possession action starts when a mortgage lender or landlord completes and submits a claim to the county courts to repossess a property. The court process of possessing a property broadly follows four stages:

-

A claim for a mortgage or landlord possession being issued by a mortgage lender or a landlord;

-

An order being made by the county court. This can either be an outright order that the property is to be recovered by a specific date, or a suspended order that is suspended as long as the defendant complies with conditions specified in the order;

-

If the defendant fails to leave the property by the date given in the order or does not meet the terms of a suspended order, the order may be enforced by a warrant of possession. This authorises the county court bailiff to evict the defendant from the property. The bailiff then arranges a date to execute the eviction; and

-

Repossession by a county court bailiff. Repossessions may occur without county court bailiffs, through less formal procedures, so the actual number of repossessions is usually greater than the number carried out by county court bailiffs.

Figures for each of these four processes are summarised in the Mortgage and Landlord Possession Statistics bulletin, alongside two measures of case timeliness. The first timeliness measure looks at how long it has taken (in weeks) to get to each stage in the relevant court process from the date when the claim was received, whilst the second reports how long it takes, on average, for claims to reach each stage in the process (number of quarters elapsed) alongside the proportion of claims that actually reach each stage.

Supplementary tables and CSV datasets accompany the bulletin, allowing users to analyse the data themselves. The CSV datasets contain local authority and court-level breakdowns of claims, orders, warrants and county court bailiff repossessions for England and Wales, for the full amount of time that data are available.

A CSV is also available with the data used for the maps in the publication. It gives the number of possession claims and repossessions by county court bailiffs per 100,000 households at the local authority level.

This report also includes UK wide total mortgage repossession figures from UK Finance (formally the Council of Mortgage Lenders (CML)). These are not directly comparable to the other figures in this report, which are England and Wales only and only cover county court bailiff repossessions (see Other useful publications and sources of possession statistics).

Information on the representation status of claimants and defendants in repossession cases defended, can be found in Civil Statistics Quarterly at https://www.gov.uk/government/collections/civil-justice-statistics-quarterly

3.1 Statutory time periods

The law requires at least 4 and no more than 8 weeks between claim and court hearing. Possession orders stipulate when a tenant must vacate the property - typically within 4 weeks from the date the order was made. Landlords cannot issue a warrant until after this period (if the tenant has failed to comply).

Minimum reasonable target times are also estimated. These assume the court hearing happens 8 weeks after the claim, with 4 weeks until the landlord can apply for a warrant, 2 weeks for the landlord to receive notice of the warrant’s issue and the court bailiff to schedule the visit, and 1 week’s notice before possession.

3.2 Users of the statistics

These statistics are a leading indicator of the number of properties to be repossessed (by county court bailiffs) and the only source of sub-national possession information. In addition to monitoring court workloads, they are used to assist in the development, monitoring and evaluation of policy both nationally and locally.

The main users of these statistics are Ministers and officials in central government departments, such as the Ministry of Housing, Communities and Local Government and HM Treasury. Other users include non-governmental bodies, including various voluntary organisations, with an interest in housing and homelessness, such as Shelter.

3.3 Data Sources

The figures in the bulletin are based on statistical data extracted from the Case Management Information System (a data warehousing facility drawing data directly from county court-based administrative systems) and data derived from the claims made via Possession Claims Online (PCOL).

3.4 Revisions

The statistics in the latest quarter are provisional, and are therefore liable to revision to take account of any late amendments to the administrative databases from which these statistics are sourced. The standard process for revising the published statistics to account for these late amendments is as follows:

An initial revision to the statistics for the latest quarter may be made when the next edition of this bulletin is published. Further revisions may be made when the figures are reconciled at the end of the year. If revisions are needed in the subsequent year, these will be clearly annotated in the tables.

3.5 Symbols and conventions

The following symbols have been used throughout the tables in the bulletin:

| symbol | description |

|---|---|

| .. | no data available |

| (r) | Revised data |

| (p) | Provisional data |

4. Seasonal Adjustment

The publication includes seasonally adjusted figures for claims, orders, warrants and repossessions, to account for seasonal trends. Seasonal adjustments make it easier to observe the underlying trends, and other non-seasonal movements. Lags in judicial processing caused by events such as Easter or Christmas, can cause distortions to the time series.

To seasonally adjust these time series, we use the R package Seasonal, which is an R interface to X-13 ARIMA. X-13-ARIMA is a seasonal adjustment software developed and supported by the United States Census Bureau. The X-13 ARIMA procedure makes additive or multiplicative adjustments to create a seasonally adjusted time series.

The X-13 ARIMA works by modelling the original time series as an autoregressive moving average process (ARIMA) in order to detect and adjust for outliers and other distorting effects. It also detects and estimates for factors such as calendar effects.

The seasonally adjusted figures are bounded by benchmarking against annual figures. This preserves the annual totals in the overall yearly-grouped (quarter 1 to 4) adjusted figures. The Denton method utilised preserves the quarter to quarter difference in the original series, and distributes the seasonal adjustment in this pattern. This method allows the utilisation of the full dataset we possess (maximising the quality of the input data), and preserves the historic output data for past publications (ensuring comparisons can be made).

The output seasonally adjusted figures are tested for quality and seasonality through each run of the model. Where there are limitations with the figures, these are stated in footnotes on the relevant table.

We use seasonally adjusted figures to facilitate quarter on quarter comparisons for each possession action. This gives greater clarity to the changes and trends, allowing relative observed quarter-to-quarter changes to be noted, compared to same-quarter previous-year comparisons.

4.1 Seasonal Adjustment following Covid-19

In this publication, figures for claims, orders and warrants have been seasonally adjusted. This is to remove seasonal effects in the data and enable comparisons between consecutive time periods.

The impact of Covid-19 however is an irregular fluctuation caused by a pandemic. This has caused some degree of random variation in the series very different to the regular behaviour of the seasonal effects. The previous seasonal adjustment methodology gave results which were heavily impacted by the low numbers of actions from Q2 2020 to Q1 2021 (covid-19 period). Following expert advice, we have made changes to the methodology to produce meaningful results as below:

- The data from the Covid-19 period were marked as outliers (AO).

- The transform spec for all seasonal adjustments was set to “log”, in order to prevent negative seasonally adjusted data.

- Forcing of yearly totals was removed -that is the annual totals of seasonally adjusted data are not adjusted to match the yearly totals of the raw data.

The above adjustments ensure that for Q2 2020 to Q1 2021, volumes of possession actions cannot result in negative values following seasonal adjustment, whilst also having minimal impact on the rest of the series. The removal of the “annual forcing” means that the total of seasonally adjusted data for a single year may be different to that of the raw data.

For a fuller explanation on how the X13A program seasonally adjusts time series see: https://www.census.gov/srd/www/x13as/; and https://www.ons.gov.uk/methodology/methodologytopicsandstatisticalconcepts/seasonaladjustment

5. Map information

The local authority level maps used in this publication are based on the defendants’ correspondence address.

Defendant address is used as a proxy for locating possession actions, however this is not a guarantee of true repossession address. Addresses that fall outside of England and Wales are not included in the mapping dataset, and classed as ‘not identified’ within the Local Authority CSV.

Caution is advised when using data calculated for low-population local authorities (i.e. City of London or Isles of Scilly), as small changes in numbers of possession actions can change the rate per 100,000 to a large degree due to low numbers in overall population.

For England, the household projections used to produce the maps are based on the Office for National Statistics 2016-based projections for England:

The last release published in June 2020.

For Wales, StatsWales’ 2014-based projections (which cover all local authorities within Wales):

-

Principle variant used.

-

Last updated: March 2017

(updated with future projection, current projection for 2014-2039)

In addition to this, the boundary lines were drawn using the Great Britain local authority districts (LADs) from the ONS Geoportal:

http://geoportal1-ons.opendata.arcgis.com/datasets/

This contains the digital vector boundaries for LADs in Great Britain as of December 2017. Therefore, the maps created may not reflect any boundary changes that may have occurred since 2018/19.

6. Guide to local authority and court level CSVs

6.1 Background

The accompanying CSVs provide the user with local authority and court-level breakdowns of claims, orders, warrants and county court bailiff repossessions for the full amount of time for which data is available. This is an aim at maximising the usage of data by users so analytical work can be carried out independently.

The data is provided in a comma separated value (CSV) machine-readable format so that it can easily be imported into analytical software packages. These packages include R, Access, SQL, SAS, up-to-date versions of Excel but not versions of Excel prior to 2007 (because of insufficient number of rows). This format enables the user to manipulate and aggregate the published data in different ways.

The site below is an example of some of the ways that possessions data has been used by customers:

england.shelter.org.uk/professional_resources/housing_databank

This analysis is not a product of the Ministry of Justice and is referenced for illustrative purposes only.

Below there is a full description of the variables and the list of possible values for each dataset provided. At the end there is also a short guide on how to view data through Excel PivotTables.

6.2 Local Authority level data variables

year: This is the year to which the data relates. The earliest year from which any of the data is available is 2003 because of quality concerns around the allocation of claims to a particular local authority prior to that date.

quarter: Each year is divided into four quarters and this is the quarter to which the data relates.

possession_type: This summarises whether the type of claim relates to a landlord or mortgage possession. Landlord possessions are broken down by the type of landlord and the procedure used: social landlord, private landlord, or accelerated procedure.

possession_action: This describes what the number relates to: claims, orders, warrants or repossession by a county court bailiff. Orders, in turn, are broken down by whether they were outright or suspended orders.

la_code: This is a code assigned to each local authority across government. This facilitates the incorporation of data from government departments at the local level that use the same code.

local_authority: This is the local authority of the defendant, derived from the defendant’s address. Local authorities have been re-organised over time, and claims cannot be retrospectively be allocated. This means that the local authority boundaries used are the boundaries used today even for past years. This allows for a like-for-like comparison of claim numbers in an authority over time. The dataset contains 348 local authorities, as well as a ‘not identified’ field.

county_ua: Where a local authority is a district within a county, the county is provided also, to allow county-level aggregation. Where the local authority is unitary in nature, the description in the county variable will be the same as in the local authority variable. The dataset contains 92 counties, as well as a ‘not identified’ field.

region: The region in which the local authority is located is provided, based on the Government Office regional breakdown for local authorities.

There are 10 regions, listed below, as well as a ‘not identified’ field:

| region |

|---|

| East |

| East Midlands |

| London |

| North East |

| North West |

| South East |

| South West |

| Wales |

| West Midlands |

| Yorkshire and the Humber |

| Not Identified |

value: This provides the number e.g. the number of claims that were issued in that local authority during that quarter.

6.3 Court level data

The court data-set consists of seven variables. This is the court where the claim was issued.

year: This is the year to which the data relates. The earliest year from which any of the data is available is 1999 for claims and orders. For warrants and repossessions the earliest year is 2000. This reflects improvements in the data quality over time.

quarter: Each year is divided into four quarters and this is the quarter to which the data relates.

possession_type: This summarises whether the type of claim relates to a landlord or mortgage possession. Landlord possessions are broken down by the type of landlord and the procedure used: social landlord, private landlord, or accelerated procedure.

possession_action: This describes what the number relates to: claims, orders, warrants or repossession by a county court bailiff. Orders, in turn, are broken down by whether they were outright orders or suspended orders.

court: This is the court through which the claim was issued. The dataset contains 216 courts, as well as a ‘not identified’ field.

region: This is the region in which the court lies. The regional breakdown used is from the Court and Tribunal Service (HMCTS) which allocates all courts to an administrative region. This is different from the regional breakdown used in the local authority CSV which is the Government Office regional breakdown for local authorities.

There are 7 regions, listed below, as well as a ‘not identified’ field.

| region |

|---|

| London |

| Midlands |

| North East |

| North West |

| South East |

| South West |

| Wales |

| Not Identified |

value: This provides the number e.g. the number of claims that were issued in that local authority during that quarter.

6.4 Map data

The map csv dataset contains six variables, based on the data used for the four maps produced for the publication. The boundaries on each map are the local authorities in England and Wales.

la_code: This is a code assigned to each local authority across government. This facilitates the incorporation of data from government departments at the local level that use the same code.

local_authority: This is the local authority of the defendant (person having their home repossessed) which is derived from their address. The defendant’s address is extracted through our CaseMan data-base. Therefore, the local authority level data is based on the address of the defendant going through the repossession action. The dataset contains 348 local authorities. (This field does not contain a ‘not identified’ field as in local_authority LA_CSV.csv)

region: The region in which the local authority is located is provided, based on the Government Office regional breakdown for local authorities (as in the LA_CSV).

map_1_mortgage_possession_claims: this is the number of mortgage possessions claims per 100,000 households in each local authority.

map_2_mortgage_repossessions: this is the number of mortgage repossessions per 100,000 households lodged in each local authority.

map_3_landlord_possession_claims: this is the number of landlord possessions claims per 100,000 households lodged in each local authority.

map_4_landlord_repossessions: this is the number of landlord repossessions per 100,000 households lodged in each local authority.

Per household figures: If you wish to calculate possessions figures per 100,000 households for yourself please see the DCLG’s figures for number of households at the local authority level in Table 116 at https://www.gov.uk/government/statistical-data-sets/live-tables-on-dwelling-stock-including-vacants

6.5 Using Excel PivotTables (Excel ver. 2007-2016)

PivotTable is an Excel tool that allows data to be grouped from a csv file, and figures summarised and sorted by their characteristics. They are particularly useful when analysing or extracting data from large detailed datasets.

Example: – to display quarterly data for Social Landlord Repossessions in Wales and London courts

-

Open Court CSV file (Court_CSV.csv)

-

Click on Insert tab. Select PivotTable command.

-

Create PivotTable. In dialog box select data from csv (whole worksheet). Place PivotTable in new worksheet. Click ok

-

Drag and drop; - ‘possession_type’ ‘possession_action’ variables into ‘Filters’ box (top left) - ‘Year’ and ‘Quarter’ into ‘Rows’ box (bottom left) - ‘region’ into ‘Columns’ box (top right) - ‘values’ into ‘Values’ box (bottom right).

-

From ‘possession_type’ field, select/check box for ‘Social Landlords’ From ‘possession_action’8 field, select/check ‘Repossessions’ From *‘region’ field, select/check ‘Wales’ and ‘London’

-

The table should now display number of social landlord repossessions for Wales and London for all years covered broken down by quarter.

-

Data can be manipulated by changing input variables in PivotTable fields (step 4) or selecting different variable breakdowns (step 5).

Note:

-

PivotTables sometimes displays the ‘value’ field as a ‘count’ (when cells are blank or non-numeric), rather than ‘sum’ of the figures (when data is all numeric). If this occurs; click on ‘value’ box drop down menu, change ‘Value Field Settings’ to from ‘count’ to ‘sum’. This can also be changed by individual cell, by right clicking and changing the ‘Value Field Settings’.

-

Excel version prior to 2007 require opening the Data tab rather than Insert at step 2 (see below) a. Step 2: Open Data tab. Select PivotTable and PivotChart command; continue with guide as before.

-

Excel versions prior to 2007 limit number of rows to 65,536 restricting access/analysis when using larger CSV files.

7. Policy changes

7.1 The Coronavirus Act

On 25th March 2020, the Coronavirus Act was passed and the Financial Conduct Authority (FCA) announced that they expected all lenders to cease any mortgage repossession action to help businesses and individuals affected by the coronavirus (Covid-19) pandemic. From 27 March 2020 to 20 Septemer 2020, the court service suspended all ongoing housing possession actions[footnote 1], meaning that all cases either currently in, or about to enter the system cannot progress to the stage where someone could be evicted (later amended to allow exceptional circumstances, including cases where tenants have demonstrated anti-social behaviour or committed fraud). This has resulted in a significant decrease in all types of repossession actions for both mortgages and landlords.

Until 20 September 2020[footnote 2], landlords could not start possession proceedings unless they had given their tenants six-months’ notice (landlords can choose to give more than this six months’ notice.) In addition, bailiffs could not to carry out repossessions in national lockdowns or local lockdown areas in England (Tiers 2 and 3)[footnote 3].

Read more information on the policy and restrictions on possesssion court proceedings in the Annex section of our bulletin.

7.2 New Bailiff Laws

New laws came into effect on 6 April 2014 to bring an end to bad and aggressive bailiff behaviour, while making sure businesses, local authorities and others can still fairly enforce debts owed to them. These reforms are part of a wider package under changes to the Tribunals, Courts & Enforcement Act 2007.

With roughly 4 million debts collected each year, in future only bailiffs who have been trained and received certification will be allowed to practise.

Bailiffs will be banned from entering homes at night and from using physical force against debtors. The changes will also prevent bailiffs from entering properties where only children are at home and includes further measures to protect vulnerable people. Bailiffs will be prevented from taking vital household essentials from debtor’s property, such as a cooker, refrigerator or washing machines.

A new set of fixed fees for debtors has also been introduced, to end the previous situation where bailiffs were setting their own fees – sometimes at very high levels – and adding these to the amount people in debt had to pay.

7.3 Introduction of Mortgage Pre-Action Protocol

A Mortgage Pre-Action Protocol (MPAP), approved by the Master of the Rolls, for possession claims relating to mortgage or home purchase plan arrears came into effect on 19 November 2008. The protocol applies to mortgage arrears on:

-

First charge residential mortgages and home purchase plans regulated by the Financial Service Authority under the Financial Services and Market Act 2000;

-

Third charge mortgages for residential property and other secured loans regulated under the Consumer Credit Act 1974 on residential property; and,

-

Unregulated residential mortgages.

The Protocol gives clear guidance on what the courts expect lenders and borrowers to have done prior to a claim being issued. The main aims of it were to ensure that the parties act fairly and reasonably with each other in any matters concerning the mortgage arrears, to encourage more pre action contact between lender and borrower and to enable efficient use of the court’s time and resources.

The introduction of the MPAP coincided with a fall of around 50% in the daily and weekly numbers of new mortgage repossession claims being issued in the courts as evidenced from administrative records. As orders are typically made (when deemed necessary by a judge) around 7 weeks (using 2011 data) after claims are issued, the downward impact on the number of mortgage possession orders being made was seen in the first quarter of 2009.

It has not been possible to adequately quantify the long term impact of the MPAP. This reflects the lack of a good comparator (although the MPAP was not introduced in Scotland, the big lenders in Scotland also operate south of the border and so lender behaviour is likely to be the same as in England and Wales), and the existence of other factors such as changing economic conditions, other measures introduced shortly after the MPAP, and lenders desire to minimise their losses. More details about the protocol can be viewed using the link:

http://www.justice.gov.uk/courts/procedure-rules/civil/protocol/prot_mha

8. Additions to publication

From the October to December 2017 publication onwards, a further breakdown of average time taken for possession claims to move through each stage of the court process has been introduced. Average time taken is now broken down by order type (outright or suspended) for Mortgage Possession claims and for Landlord Possession, average time taken is now broken down by tenure (whether it is a private landlord or social landlord claim, or an accelerated claim).

As part of the current publication, average time taken has also been reported using both the mean and median averages. See published Tables 3 and 6 respectively for these new figures, with further insight within the commentary.

9. Other useful publications and sources of possession statistics

The Ministry statistics on court actions cover England and Wales.

Total UK wide repossessions figures are published by UK Finance (formally the Council of Mortgage Lenders (CML)) on the same date as this publication. They cover all actual repossessions across the United Kingdom (including where there is no action by county court bailiffs) and can be found at the following link: https://www.cml.org.uk

The statistics shown for “properties taken into possession” are published figures from UK Finance, which is an industry body representing around 97% of the UK residential lending industry. It should be noted that:

- UK Finance statistics on actual possessions include properties surrendered voluntarily.

- Given the time lags involved, some of the court orders for the possessions shown by UK Finance may have been granted in earlier time periods.

Mortgage possessions counted in the UK Finance statistics mainly relate to the non-repayment of loans which are secured as a “first charge” against the property. The large majority of “second charge” lending (any loan secured on a property where a separate first charge loan already exists) falls outside UK Finance’s membership, therefore any resulting repossessions will not be counted in their figures. A comprehensive review of statistics relating to the housing market has been published by the National Statistician’s Office.

The Bank of England, compile quarterly statistics aggregated from the returns from around 340 regulated mortgage lenders and administrators, providing data on their mortgage lending activities. Figures within Bank of England statistics will differ from the UK Finance estimates, due to reporting numbers of possession actions on second or subsequent charges – not covered by UK Finance membership, which can represent multiple actions against the same borrower.

For the number of repossessions and evictions in Scotland refer to ‘Civil Justice Statistics in Scotland’ publication, found at: https://www.gov.scot/publications/civil-justice-statistics-scotland-2019-20/

For the number of repossessions and evictions in Northern Ireland please see ‘Mortgages: Action for possession’ publication found at the following link: https://www.courtsni.gov.uk/en-GB/Services/Statistics%20and%20Research/Pages/default.aspx

Figures relating to the England household characteristics (such as owner occupier or renting households etc.) can be found in Ministry of Housing, Communities, and Local Government ‘English Housing Survey’, found at the following link: https://www.gov.uk/government/collections/english-housing-survey

10. Glossary

| word | definition |

|---|---|

| Accelerated Possession | Landlords can sometimes evict tenants using ‘accelerated possession’. This is quicker than a normal eviction and doesn’t usually need a court hearing. |

| Actual repossession | Includes repossessions carried out by county court bailiffs, but also includes other repossessions. |

| Civil Cases | Cases that do not involve family matters or failure to pay council tax. These cases are mainly dealt with by county courts and typically relate to debt, the repossession of property, personal injury, the return of goods and insolvency. Particularly important, complex or substantial cases are instead dealt with in the high court. |

| Claims for recovery of land | Include claims for the repossession of property by a mortgage lender, social or private landlord for example, where the mortgagee or tenant fails to keep up with mortgage or rental payments. |

| Possession Order (Social Landlord) | The court, following a judicial hearing may grant an order for outright possession of land. This entitles the claimant to apply for a warrant to have the defendant evicted, except in the case of suspended orders. Claims can be in relation to mortgages or landlords. A Social Landlord order is used for standard claims that relate to social landlords, this includes local authorities and housing associations. |

| Repossessions by county court bailiffs: | Once a warrant has been issued county court bailiffs can repossess the property on behalf of the claimant |

| Suspended Orders | A mortgage possession action which has been suspended as a resulted of an agreed payment plan between the borrower and lender. |

| Warrant of possession | To enforce a court order for the possession of property or land. |

11. Data Visualisation Tool

11.1 Introduction

As part of our wider work on improving data visualisation and accessibility, we have developed a data visualisation tool which sits on top of the data underlying the publication and its associated csv files - the tool provides users with the capability to:

- interrogate the published information easily at a lower level of detail, e.g. by local authority; and

- access and produce a range of charts specific to their user requirements.

11.2 Guide to the tool

The tool displays the latest published statistics on possession actions by county courts and repossessions by county court bailiffs in England and Wales.

It allows users to investigate aspects of Mortgage and Landlord possession actions, such as:

- Workload in the county courts of England and Wales by possession type and possession action

The tool also allows data to be interrogated at a lower level than is presented within the publication e.g.

- Regional breakdown of figures for possession type/action.

- Local Authority breakdown of figures for possession type/action.

- Court breakdown of figures for possession type/action.

To help understand the terminology, a glossary is available alongside a notes and context page which provides extra information, accessible all areas of the tool.

Data

The data within the tool are sourced from the accompanying csv files published alongside Mortgage and Landlord Possession Statistics Quarterly (see link above), with the exception of the geolocation data for courts and local authority household projections, which are publicly available (see section 5).

How to use the tool

The tool allows you to explore and focus down on the available data in a dynamic way. To do this, each page has a set of filters on the right hand side. The exact filters vary from page to page, but some examples are:

- Possession Type (Mortgage or Landlord, and the sub-set of Social, Private and Accelerated landlord actions)

- Possession Action: filter by possession actions, i.e. Claims, Orders (outright or suspended), Warrants, or Repossession by County Court bailiff

- Date range: allows you to choose a range of quarters for which you want to see the data

- Geographical area: England and Wales, Regional, or Local Authority

Each table and chart is set up to allow you to either hover, select, filter or highlight relevant data. Descriptions of how to interact with the chart are provided in the chart title.

To navigate around the tool, choose the tabs at the top of the screen.

How to send us your feedback

We welcome any comments you have about the data visualisation tool, including your views on how the tool can be improved, e.g. are there better ways of presenting the information or certain aspects of it?

Enquiries and feedback should be directed to Civil and Administrative Justice Statistics using the details below:

Email: CAJS@justice.gov.uk

or

Carly Gray, Head of Civil, Family and Administrative Statistics Access to Justice Statistics, Data and Evidence as a Service

Ministry of Justice 3rd Floor

10 South Colonnade

London

E14 4QQ

© Crown copyright Produced by the Ministry of Justice Alternative formats are available on request from ESD@justice.gov.uk

-

Though possession proceedings were suspended by the Civil Procedure Rules - Practice Direction 51Z, amendments have been made to allow exceptions for the stay, such as in Civil Procedure (Amendment No. 2) where claims against trespassers to which rule 55.6 applies, applications for case management directions which are agreed to by all parties and claims for injunctive relief were exempt from the stay. All updates to the Civil Procedure rules and amendments can be found here. ↩

-

https://www.legislation.gov.uk/uksi/2020/889/article/2/made ↩

-

https://www.legislation.gov.uk/uksi/2020/1290/contents/made ↩