Petrol filling stations

This publication is intended for Valuation Officers. It may contain links to internal resources that are not available through this version.

This guidance applies primarily to Petrol Filling Stations (PFS) but may also be referred to when valuing petrol sales forecourts as part of larger, multi-use hereditaments. Petrol filling stations forming part of a single hereditament with a superstore/hypermarket are dealt with at Rating Manual section 520 - (Hypermarkets and Superstores) and the accompanying Practice Notes. PFS located as part of Motorway Service Areas are considered separately in Rating Manual: section 710 (Motorway Service Areas). Background information on the PFS industry is at Appendix 1.

- Primary Description Code: CG

- List Description: Petrol Filling Station & Premises

- Scat Code: 209

- Suffix G

Responsibility for inspection, survey and valuation rests with Regional Valuation Unit (RVU) referencers and valuers. The National Valuation Unit (NVU) is responsible for providing advice and support to RVUs, as well as the development of each national scheme of valuation when appropriate.

4.1 The PFS class of property sits within the wider Transport CCT (Class Coordination Team). The CCT is responsible for the approach to and accuracy and consistency of PFS valuations. The team will deliver Practice Notes describing the valuation basis for revaluation and provide advice as necessary during the life of the rating lists.

4.2 Valuers have a responsibility to:

- Follow the advice given at all times

- Not depart from the guidance given on appeals or maintenance work, without approval from the co-ordination team .

- seek advice from the co-ordination team before starting any new work

There is no specific legal framework for this class however The Petroleum (Consolidation) Regulations 2014 (PCR) which came into force on 1 October 2014 apply to workplaces that store petrol where petrol is dispensed, i.e. retail and non retail petrol filling stations. From October 2014 the petrol licensing regime is replaced with a petrol certification scheme. An owner of dispensing premises where petrol is kept needs to hold a Petroleum Storage Certificate (known as a ‘storage certificate’) to comply with the regulations.

6.1 Inspections should be carried out in accordance with the Valuation Office Agency Code of Practice with the forecourt shop measured to NIA and other buildings measured to GIA for example workshops.

6.2 A 2 page inspection checklist should be completed (see Appendix 2) for all new properties and updated for maintenance work and stored in the property folder of the Electronic Document Records Management (EDRM) system. It is recommended ELDA is used to produce plans including one of the overall site layout.

Unit of Assessment / identifying the hereditament

6.3 On inspection it is first necessary to consider the Unit of Assessment and to identify the hereditament(s).

6.4 It should be noted at many PFS there can often be more than one rateable occupier and unit of assessment and a separate hereditament may need entering into the list, for example separately operated Electronic Delivery Lockers or hand car washes. Full details should be taken and consideration as to whether more than one unit of assessment is required.

6.5 It should however be noted that often there may be separate stand alone buildings on a forecourt operating under a well known brand name, for example providing hot coffee or fast food. In many of these cases, similar to a Motorway Service Area, the operator of the host i.e. the PFS, remains in paramount control of all parts and simply has franchise arrangements with well known brands. In these cases it is expected only one assessment will exist but clarification should be sought on inspection and full facts obtained. Advice can also be provided by Transport CCT members or the NVU.

After carrying out an inspection the following should take place:

- ELDA site plans saved in the EDRM property folder

- A copy of the inspection checklist saved in the EDRM property folder

- If not done so already, the address should be created in the Non Bulk Server (NBS) with survey information obtained entered on page 2 of the valuation

Valuations of petrol filling stations are made on the direct rentals basis. For each Rating List a national scheme of valuation exists on this basis with full details shown within the appropriate Practice Note. Detailed information on the Valuation Methodology to be followed is at Appendix 3

In accordance with the relevant Practice Note valuations for Petrol Filling Stations should be maintained and stored within the relevant Rating List Non Bulk Server application. Further support is available from:

- RVU Transport CCT members or PFS lead valuers

- National Specialist Unit

- VOA Rating Manual v5 s770

- Non Bulk Server (NBS) Manual

- RSA (Rating Support Application)

1. Market Appraisal

1.1 Leading up to 2021 the roadside retail sector generally outperformed other commercial sectors such as high street shops, hotels, restaurants and pubs. Property asset values increased since 2015 and there were ample signs of market confidence, with banks willing to lend to the Petrol Filling Station (PFS) sector often for new to industry sites, which can cost between two to five million pounds to develop, and also for knock down and rebuild sites. Over the last few years, the industry has seen a number of mergers and acquisitions with larger operators purchasing in a single deal, several sites from a smaller dealer. These larger operators have sought to take over at times struggling, under-performing sites and redevelop them often providing additional retail facilities with various well known franchise partners.

1.2 Expansion from both oil companies and superstores has been limited in recent years with neither sector looking to actively increase their site numbers. In general, most forecourts brought to the market still change hands if priced and marketed sensibly and demand is healthy. The independent sector of the market remains positive with independently run PFS increasing in number since 2015.

1.3 Margins on fuel remain unpredictable at times due in part to variations in oil prices over the period since the last Antecedent Valuation Date. An operator will still look for a long-term view of a maintainable margin they can achieve, reflecting times when this may rise or fall. Forecourt shop convenience choices continue to offer a wide variety of recognised brands to attract the customer. These increasingly include well known hot drinks and sandwich options along with fast food and can include separate stand-alone buildings located on the forecourt, some with a drive through option. In most cases these are operated by the PFS on a franchise basis.

1.4 Despite rising in recent years, numbers of non-traditionally fuelled cars for example electric vehicles (EVs), remain relatively minor when comparing with petrol and diesel car numbers. Indeed, the impact on the PFS market of EVs is still considered to be in its infancy and relatively insignificant at this stage. In general terms fuel retailers still demonstrate their commitment to forecourt properties by continuing to sign up to long-term leases. The sector is robust, and it is expected that EV charging will simply be another retail offer that the PFS sector will harness over time as technology progresses.

1.5 Up until 2020 fuel throughputs in many cases have generally remained static whereas forecourt shop turnovers in many cases have risen, reflecting the increased popularity of convenience shopping at forecourts and operator partnerships with popular high street catering brands. Many operators have taken the opportunity to redevelop existing shops by knocking down and re-building to a much larger size or extending. The latter sometimes arises when dated valeting equipment is in need of replacement, allowing an operator to remove the car wash and extend the shop into this space.

Due to lockdowns associated with COVID there were some temporary fluctuations in trading patterns during the 2020/21 year which are not considered as fair or maintainable.

2. Changes from last practice note

The market appraisal section has been updated along with the valuation scheme where appropriate.

3. Ratepayer discussions

3.1 As well as speaking to experts involved in the PFS industry who specialise in valuation and marketing of PFS, discussions have also taken place with representatives of the three main sectors of the PFS market:

- independent retailers

- oil companies

- superstores

3.2 Following these discussions and a review of relevant evidence, a scheme of valuation has been accepted in principle. This has consequently been applied to the valuation of PFS for the 2023 Rating Lists and is reflected in the scheme detailed below.

3.3 When determining a reasonable level of fair maintainable trade (FMT) as at 1/4/21, it has been agreed between the VOA and the PFS industry that simply adopting any trade solely impacted by COVID, as FMT, would be inappropriate. Regard must be had to other years leading up to the Antecedent Valuation Date to help inform a level of FMT that would be agreed between a landlord and tenant as fair, and maintainable, with a forward look and prospects of continuance reflected.

4. Valuation scheme

4.1 Application

4.1.1 The scheme applies to all types of PFS in England & Wales, whether stand alone or part of a larger hereditament such as a superstore or workshop/car showroom. An exception is where the PFS is located at a Motorway Service Area and is ‘blue signed’ from a motorway. A separate scheme applies in these cases.

4.1.2 Valuers undertaking PFS valuations must be trained on the VOA Non Bulk Server and fully conversant with all the instructions relevant to this type of hereditament embodied in the Rating Manual.

4.2 Introduction to the scheme

4.2.1 Valuations of PFS in the 2023 Rating Lists are made on the direct rental basis in which the main elements are:

- the petrol forecourt

- the forecourt shop

- valeting

- non forecourt buildings for example restaurants, takeaways, workshops, showrooms and other sources of income where appropriate

4.2.2 The PFS scheme is developed from the analysis of rental information using fair maintainable trade (FMT) as a measure of the rental value attributed to each element of a PFS.

4.2.3 The practice adopted by the actual occupier in terms of operator’s policy will generally be taken as indicative of that which would be pursued by the hypothetical tenant, who would be seeking to maximise overall profitability from the site taking due account of competition in the locality. However, there may be circumstances where the actual trade is not indicative of the hypothetical fair maintainable trade and some adjustment, for example for over or under trading sites may be required. If this is the case advice from the Transport Class Coordination team must be obtained.

4.3 The petrol forecourt

4.3.1 The petrol forecourt includes the value of the developed forecourt excluding non-rateable plant items.

There are three separate streams of fuel throughput to consider:

- retail

- low Margin fuel cards (LMFC), also known as agency

- bunkered fuel

The value of the petrol forecourt is determined in accordance with nationally applied scales relating rental value to the fair maintainable throughput of these three different streams of fuel volume.

4.3.2 For the avoidance of doubt, throughput data should be recorded on Forms of Return (FOR) as:

- the total gross throughput (all grades) excluding bunkered fuel and

- bunkered fuel throughput

4.3.3 Retail fuel

Retail throughput excludes LMFC and bunkered throughput.

To determine the Fair Maintainable Retail Throughput (FMRT), the following adjustments are applied where appropriate:

- Customer Credit Accounts (CCA) – It is understood CCA at PFS are now generally historic and are declining in number. Where they do exist and are a significant part of the trade, to reflect the fact the hypothetical tenant would be unlikely to continue with such arrangements it’s necessary to consider whether an adjustment is needed. Where the CCA represents more than 5% of the retail throughput, the CCA throughput over 5% is reduced by 25%; here the CCA represents 5% or less of the retail throughput, no adjustment should be made

4.3.4 Low Margin Fuel Card (LMFC)

A Low Margin Fuel Card (also known as an Agency scheme), is where a fuel company (mainly oil companies), enter into contracts to supply fuel to vehicles through its filling station network. The card holder will often be a customer with a fleet of vehicles. A contract exists between the oil company who operate the fuel card and the fuel card holder - payment is made directly to the fuel card operator. Once fuel is dispensed at the PFS the card company effectively repurchases the fuel from the retailer at cost price, plus a handling charge for dispensing the fuel and dealing with the paperwork. The handling charge is only a proportion of the notional margin available to the retailer for normal retail throughput.

4.3.5 Bunkered fuel

Bunkered fuel is fuel which is stored and dispensed by a PFS operator, usually on behalf of another operator who actually owns the fuel. For providing this service the PFS operator receives a handling fee/commission. This fee is of a much smaller margin than that achieved for retail fuel or LMFC sales.

4.4 Valuation scheme scales

4.4.1 Retail fuel (FMRT)

The price per 1000 litres (£/000L) to be applied to the FMRT varies, according to the level of total FMRT plus the weighted LMFC trade and the unleaded (UL) price per litre implicit in the retail throughput adopted. This has been developed from the analysis of rental evidence which includes an adjustment for price. Table 1 (PN 2023) sets out the retail fuel scale to be applied.

The national scheme agreed between the VOA and the PFS industry adopts the 2019 unleaded price available for each individual PFS, where a price is supplied by Experian Catalist to the VOA for each site. The UL price per litre adopted is the site’s average Catalist price for 2019 and together with the relevant throughputs, would be the most up to date trade and reliable information available to the hypothetical tenant when determining their rental bid at the Antecedent Valuation Date (AVD) of 1 April 2021. The pricing policy adopted by the actual site is taken as indicative of the policy that would be pursued by the hypothetical tenant in aiming to maximise overall profitability from the site, taking due account of competition in the locality and price sensitivity of the local market.

LMFC throughput is ‘weighted’ so that this element of throughput is considered in terms of FMRT. The following equation illustrates how the LMFC throughput is converted to throughput in terms of FMRT:

LMFC throughput x LMFC margin = Weighted LMFC throughput

Notional Retail margin

This equation calculates the notional profit available from the LMFC throughput and then relates this to the amount of FMRT required to generate the same level of profit. The reason being that the hypothetical tenant would take the LMFC throughput and consider what this equated to in terms of FMRT when making their rental bid.

The weighted LMFC throughput is then added to the FMRT and together with the UL price per litre determines the appropriate price per 1000 litres to be applied.

4.4.2 LMFC

The price per 1000 litres (£/000L) applied to the LMFC varies according to the level of total FMRT plus the weighted LMFC in the same way as retail fuel. The notional margin does not vary and recognises the fact that a limited handling fee is received by the operator for this throughput rather than a full retail margin. Table 2 (PN 2023) sets out the LMFC scale.

4.4.3 Bunkered fuel

The price per 1000 litres to be applied to bunkered fuel throughput is £1.40.

4.4.4 Staffed kiosk adjustment

In a relatively small number of instances (usually a specific superstore operator), a site will have no retail sales from a forecourt shop or the forecourt area itself and will only have a small kiosk. Where this kiosk is permanently staffed during opening hours for the sole purpose of collecting petrol, jet wash and car wash monies, an adjustment of 25% is made to the retail petrol value only. This is supported by rental evidence and reflects what the hypothetical tenant’s approach might be to the fact that all staff costs are covered by the fuel element income and not shared across fuel and a forecourt shop.

4.5 Forecourt shop

4.5.1 Retail trade valuation scales

The value of the forecourt shop, together with any ancillary offices and stores, will be determined in accordance with a nationally applied scale relating rental value to the achievable fair maintainable shop trade (FMST).

The FMST to be adopted is the turnover that a reasonably competent operator would expect the site to achieve from shop sales, excluding VAT. The turnover should also exclude income received from fuel, jet/wash transactions and monies received from both National Lottery Sales and Paypoint/Payzone facilities.

Where a site achieves only comparatively modest petrol sales an adjustment is made to the retail shop value. Forecourt shop overheads are covered jointly by the income from the fuel throughputs and the shop sales. Where the fuel throughputs are considered modest a greater proportion of such overheads fall to be covered by the shop sales, and the hypothetical tenant would adjust their bid accordingly.

This adjustment applies when the total of FMRT plus weighted LMFC throughput is less than 5 million litres.

By way of an adjustment for high turnover shops and following analysis of rental evidence and market knowledge plus industry discussions, the total shop value is capped at £115,500.

This method of valuation is applied to both forecourts where shop sales are generated primarily from motorist trade as well as the increasing number of sites trading as a destination shopping venue or convenience store. It is not considered appropriate to compare the values attributed to standalone convenience stores with those forming part of a petrol filling station. Rental evidence and market knowledge suggest that there is no direct comparison between the two types of stores and would not be comparing like with like. Furthermore a convenience store is not within the same mode and category of use as a PFS.

Table 3 (PN 2023) sets out the forecourt shop scale of values by reference to turnover and throughput.

4.5.2 Lottery, Paypoint and Payzone

A relatively low commission is received for National Lottery sales and Paypoint/Payzone facilities compared with the average level of gross profitability achieved on general forecourt shop sales and therefore monies received from operating these facilities are excluded from the FMST. However, the income available would be in the mind of the hypothetical tenant when making their rental bid and should not be completely ignored when arriving at a valuation.

Conversion to Rent Factors (CRF) are therefore applied separately as follows:

Lottery – CRF 1%

Paypoint and Payzone – CRF 0.25%

4.6 Valeting

The value of any valeting services is derived from two elements: car washes and jet washes.

Like forecourt shops the valuation of valeting services for a PFS are based on the level of fair maintainable turnover generated.

4.6.1 Car washes

Table 4 (PN 2023) sets out the Conversion to Rent Factor (CRF) and value to be attributed to total fair maintainable turnover generated by automated car washing facilities on site. Where this turnover is generated by more than one machine a single 10% reduction is applied to the car wash value.

4.6.2 Jet washes

A CRF of 17.5% is applied to the total turnover generated by jet washes.

There is no reduction for more than one machine.

4.7 Non-forecourt buildings and other sources of income

4.7.1 Stand-alone catering buildings

As stated previously, over the last few years it has become common place for certain PFS operators to add stand-alone detached buildings to a forecourt, usually in partnership with well-known catering brands. Whilst these can have an impact on sales from the existing forecourt shop, the extra footfall they bring make them a valuable addition to the site. They can range in size from a small pod type unit to a large restaurant style unit with a drive through.

Where these are in rateable occupation of the PFS operator (as it is expected that most will be), they should be valued on the basis of local comparable evidence using a rental price per square metre approach.

Other non-forecourt buildings and land may fall to be included in the hereditament on the basis that they are in the rateable occupation of the PFS operator – these may include workshops and showrooms, and other sources of income such as land used as car sales or hand car washes. The elements should be valued on the basis of local comparable evidence and included in the valuation. It should be noted however that a PFS with (for example) an ancillary workshop is a different mode and category of use compared with a stand-alone workshop. Therefore some adjustment to the rate per sq m adopted may be required when considering appropriate comparative values.

If in doubt contact your RVU Transport CCT representative, PFS lead, or the NVU.

1. Market appraisal

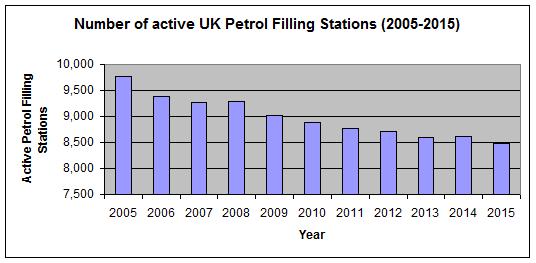

Continuing the trend of previous years the number of active UK petrol filling stations (PFS) fell between 2008 and 2015, but at a much slower rate than before. As at 2015 approx. 8,490 active UK PFS were in operation compared with 9,283 in 2008. Statistics from Experian Catalist show the 2015 level of 8,490 has approx. 64% operated by independent dealers, 19% by oil companies & 17% by superstores. Whilst the number of active PFS is expected to continue to fall, the creation of many new to industry sites suggests the number of active sites may soon reach a plateau. Expansion of the market by the superstore operators has slowed since 2008 but the likes of Asda are still seeking opportunities to increase their PFS numbers, but seeking to refurbish existing sites also. BP with their M&S partnership are also actively looking for sites.

Changes throughout 2014/2015 saw a continuing retreat of certain oil companies from front line retailing. The likes of Shell and Esso were able to sell off tranches of sites which have been eagerly snapped up by independent dealers. The dealer sector of the market has risen in recent years with a market share of circa 70% expected by the end of 2015. Most of the former oil company sites have been acquired by larger well known independent dealers, but other smaller independent dealers have taken this opportunity to increase their numbers also.

Since 2008 margins achieved on fuel continue to be unpredictable at times due in part to fluctuating prices of oil. Many PFS have evolved and maintained or even enhanced levels of overall profitability, by developing their forecourt shops with recognised brands. Despite the economic downturn post 2008, many PFS have been able to increase their shop turnovers as UK shopping habits have changed and ‘convenience’ has become more important. Indeed PFS forecourt shop sales now exceed £4.2bn per year.

Despite the recession from late 2008 the PFS industry is considered to have held up relatively well, remained robust and generally positive with values having held up well compared to many other sectors.

In terms of fuel volumes the majority of oil company and independent sites saw falls of approx. 10-20% post 1/4/08, in many cases affected by the recession, as motorists sought to conserve funds as well as shop around for the cheapest fuel. However most retailers have seen increases in volumes since 2012/13 due in part to the fall in fuel prices since the peak at that time.

Since 1/4/08 car/jet wash turnover levels at certain PFS have been affected by the large proliferation of stand-alone hand car washes in the UK. Statistics from the Car Wash Association state approx. 10,000 are thought to exist currently in the UK, with many newly created hand car wash sites located close to existing PFS.

2. Changes from the last Practice Note

For the 2017 Revaluation the methodology of valuation for PFS is in line with the 2010 national scheme of valuation and associated Practice Note, and also with how the market operates in terms of assessing the rental value of PFS having regard to trading performance.

Therefore the format of this Practice Note is similar to the 2010 version, with updated values where appropriate.

3. Ratepayer Discussions

Since 2008/2010 the VOA has held regular discussions with industry experts to monitor the state of the market, attended industry events, and kept up to date with market reports and rental transactions.

In relation to the 2017 Revaluation, discussions began in earnest with the VOA / SAA (Scottish Assessors Association) and the PFS industry during 2014. Industry representatives included those acting for the PRA (Petrol Retailers Association), UKPIA (UK Petroleum Industry Association), Car Wash Association plus Superstores & Oil Companies.

Following these discussions the VOA/SAA proposed a scheme of valuation to the PFS industry which was agreed and accepted. This was consequently applied to all petrol filling stations throughout England, Wales & Scotland.

4. Valuation Scheme

4.1 Application

4.1.1 The scheme applies to all types of PFS, whether stand alone or part of a larger hereditament such as a superstore. An exception is where the PFS forms part of a Motorway Service Area and is ‘blue signed’ from a motorway. A separate scheme applies in these cases.

4.1.2 The 2017 petrol filling station valuation scheme has been developed jointly with the Scottish Assessors Association (SAA) and therefore applies in England, Wales and Scotland.

4.1.3 The PFS market is extremely complex and it is therefore important that VOA caseworkers have a knowledge and understanding of the PFS market together with an understanding of the operating practices of all the sites within their locality.

4.1.4 It is expected that VOA caseworkers undertaking PFS valuations are fully trained on the VOA Non Bulk Server and are fully conversant with this and previous Practice Notes and the PFS Rating Manual. Additional support should first be obtained if necessary from the PFS Class Coordination Team see here. The National Specialist Unit can also provide assistance if required.

4.2 Introduction to the scheme

4.2.1 Valuations of PFS in the 2017 Rating Lists are made on the direct rental basis in which the main elements are:

- The petrol forecourt

- The forecourt shop

- Valeting

- Non forecourt buildings e.g. workshops, showrooms and other sources of income where appropriate.

4.2.2 The PFS scheme is developed from the analysis of rental information using fair maintainable trade (FMT) as a measure of the rental value attributed to each element of a PFS.

4.2.3 The practice adopted by the actual occupier in terms of operator’s policy, will generally be taken as indicative of that which would be pursued by the hypothetical tenant in seeking to maximise overall profitability from the site taking due account of competition in the locality. However there may be circumstances where the actual trade is not indicative of the hypothetical fair maintainable trade and some adjustment, e.g. for over or under trading sites may be required. If this is the case discussion with the relevant NDR unit CCT/NSU contact is required.

4.3 The Petrol Forecourt

4.3.1 The petrol forecourt includes the value of the developed forecourt excluding non-rateable plant items.

There are three separate streams of fuel throughput to consider:

- Retail

- Low Margin Fuel Cards (LMFC), also known as Agency

- Bunkered Fuel

The value of the petrol forecourt is determined in accordance with nationally applied scales relating rental value to the fair maintainable throughput of these three different streams of fuel volume.

4.3.2 For the avoidance of doubt, throughput data should be recorded on Forms of Return (FOR) as:

- The total gross throughput (all grades) excluding bunkered fuel and

- Bunkered fuel throughput

4.3.3 Retail Fuel

Retail throughput excludes LMFC and bunkered throughput.

To determine the Fair Maintainable Retail Throughput (FMRT), the following adjustments are applied where appropriate:

- Customer Credit Accounts (CCA) – It is understood CCA at PFS are now generally historic and are declining in number. Where they do exist and are a significant part of the trade, to reflect the fact the hypothetical tenant would be unlikely to continue with such arrangements, where the CCA represents more than 5% of the retail throughput, the CCA throughput over 5% is reduced by 25%. Where the CCA represents 5% or less of the retail throughput, no adjustment will be made.

4.3.4 Low Margin Fuel Card (LMFC)

A Low Margin Fuel Card (also known as an Agency scheme), is where a fuel company (mainly oil companies), enter into contracts to supply fuel to vehicles through its filling station network. The card holder will often be a customer with a fleet of vehicles. A contract exists between the oil company who operate the fuel card, and the fuel card holder and payment is made directly to the fuel card operator. Once fuel is dispensed at the PFS the card company effectively repurchases the fuel from the retailer at cost price, plus a handling charge for dispensing the fuel and dealing with the paperwork. The handling charge is only a proportion of the notional margin available to the retailer for normal retail throughput.

4.3.5 Bunkered Fuel

Bunkered fuel is fuel which is stored and dispensed by a PFS operator, usually on behalf of another operator who actually owns the fuel. For providing this service the PFS operator receives a handling fee/commission. This fee is of a much smaller margin than that achieved for retail fuel or LMFC sales.

4.4 Valuation Scheme Scales

4.4.1 Retail Fuel (FMRT)

The price per 1000 litres (£/000L) to be applied to the FMRT varies, according to the level of total FMRT plus the weighted LMFC trade and the unleaded (UL) price per litre implicit in the retail throughput adopted. This has been developed from the analysis of rental evidence which includes an adjustment for price. Table 1 sets out the retail fuel scale to be applied.

As part of the agreed scheme of valuation the UL price per litre adopted is the site’s average Catalist price for 2014 and together with the throughputs for that year would be the most up to date trade information available to the hypothetical tenant when determining their rental bid at the Antecedent Valuation Date (AVD) of 1st April 2015. The national scheme agreed between the VOA and PFS industry adopts the relevant Catalist price, which is taken as indicative pricing of the policy that would be pursued by the hypothetical tenant, in aiming to maximise overall profitability from the site, taking due account of competition in the locality and price sensitivity of the local market. This approach is well established with large numbers of cases settled on this basis.

LMFC throughput is ‘weighted’ so that this element of throughput is considered in terms of FMRT. The following equation illustrates how the LMFC throughput is converted to throughput in terms of FMRT:

LMFC throughput x LMFC margin = Weighted LMFC throughput

Notional Retail margin

This equation calculates the notional profit available from the LMFC throughput and then relates this to the amount of FMRT required to generate the same level of profit. The reason being that the hypothetical tenant would take the LMFC throughput and consider what this equated to in terms of FMRT when making their rental bid.

The weighted LMFC throughput is then added to the FMRT and together with the UL price per litre determines the appropriate price per 1000 litres to be applied.

4.4.2 LMFC

The price per 1000 litres (£/000L) applied to the LMFC varies according to the level of total FMRT plus the weighted LMFC in the same way as retail fuel. The notional margin does not vary and recognises the fact that a limited handling fee is received by the operator for this throughput rather than a full retail margin. Table 2 sets out the LMFC scale.

4.4.3 Bunkered Fuel

The price per 1000 litres to be applied to bunkered fuel throughput is £1.40.

4.4.4 Staffed Kiosk Adjustment

In a relatively small number of instances a site will have no retail sales from a forecourt shop or the forecourt area itself and will only have a small kiosk. Where this kiosk is permanently staffed during opening hours for the sole purpose of collection of petrol, jet wash and car wash monies, an adjustment of 25% is made to the retail petrol value only. This is supported by rental evidence and reflects what the hypothetical tenants approach might be to the fact that all staff costs are covered by the fuel element income and not shared across fuel and a forecourt shop.

4.5 Forecourt Shop

4.5.1 Retail Trade Valuation Scales

The value of the forecourt shop, together with any ancillary offices and stores, will be determined in accordance with a nationally applied scale relating rental value to the achievable fair maintainable shop trade (FMST).

The FMST to be adopted is the turnover that a reasonably competent operator would expect the site to achieve from shop sales, excluding VAT. The turnover should also exclude income received from fuel, jet/wash transactions and monies received from both National Lottery Sales and Paypoint/Payzone facilities.

Where a site achieves only comparatively modest petrol sales an adjustment is made to the retail shop value. The overheads of running the forecourt shop are covered jointly by the income from the fuel throughputs and the shop sales, and where the fuel throughputs are considered modest, a greater proportion of the overheads fall to be covered by the shop sales, and the hypothetical tenant would adjust their bid accordingly.

This adjustment applies when the total of FMRT plus weighted LMFC throughput is less than 5 million litres.

By way of an adjustment for high turnover shops and following analysis of rental evidence and market knowledge/industry discussions, the total shop value is capped at £110,000.

This method of valuation is applied to both forecourts where shop sales are generated primarily from motorist trade as well as the increasing number of sites trading as a destination shopping venue or convenience store. It is not considered appropriate to compare the values attributed to standalone convenience stores with those forming part of a petrol filling station. Rental evidence and general market approaches suggest that there is no direct comparison between the two types of stores and would not be comparing like with like. Furthermore a convenience store is not within the same mode and category of use as a PFS.

Table 3 sets out the forecourt shop scale of values by reference to turnover and throughput.

4.5.2 Lottery, Paypoint and Payzone

A relatively low commission is received for National Lottery sales and Paypoint/Payzone facilities compared with the average level of gross profitability achieved on general forecourt shop sales and therefore monies received from operating these facilities are excluded from the FMST. However, the income available would be in the mind of the hypothetical tenant when making their rental bid and should not be completely ignored when arriving at a valuation. Conversion to Rent Factors (CRF) are therefore applied separately and as following:

| CRF | |

| Lottery | 1% |

| Paypoint & Payzone | 0.25% |

4.6 Valeting

The value of any valeting services is derived from two elements: car washes and jet washes.

Like forecourt shops the valuation of valeting services for a PFS are based on the level of fair maintainable turnover generated.

4.6.1 Car Washes Table 4 sets out the Conversion to Rent Factor (CRF) and value to be attributed to total fair maintainable turnover generated by automated car washing facilities on site. Where this turnover is generated by more than one machine a single 10% reduction is applied to the car wash value.

4.6.2 Jet Washes

A CRF of 17.5% is applied to the total turnover generated by jet washes.

There is no reduction for more than one machine.

4.7. Non-forecourt Buildings and Other Sources of Income

Non-forecourt buildings other than the shop, such as workshops and showrooms and other sources of income, such as land used as car sales or hand car washes, which are not separately assessed and which are considered subsidiary to the PFS use, should be valued on the basis of local comparable evidence and included in the valuation. It should be noted however that a PFS with say an ancillary workshop is a different mode & category of use compared with a stand-alone workshop. Therefore some adjustment may be required when considering appropriate comparative values.

1. Introduction

After initial publication of the 2010 rating list, the VOA and SAA (Scottish Assessors Association) held discussions with PFS industry representatives over the PFS 2010 valuation scheme. Representatives included agents acting for the RMI (Retail Motor Industry), UKPIA (UK Petrol Industry Association), Association of Convenience Stores, Car Wash Association plus Superstores and Oil Companies.

Following these discussions a revised scheme of valuation for Petrol Filling Stations was applied to all relevant petrol stations throughout England & Wales. To a large extent this has now been accepted by the industry and is considered to be extremely well established.

The Petrol Filling Station valuation scheme is applied to all petrol filling stations, whether or not they are stand alone, or part of a larger hereditament, such as a superstore/hypermarket or car showroom etc. with the exception of those that are situated on motorways or at Major Road Service Areas (including those ‘blue’ signed from motorways) where a separate scheme applies.

Valuations of Petrol Filling Stations (PFS) in 2010 lists are made on the direct rental basis in which the main elements are:

(a) The petrol forecourt

(b) The forecourt shop

(c) Valeting

(d) Non-forecourt buildings (e.g. workshops, showrooms, etc) and other sources of income

The PFS scheme is developed from the analysis of rental evidence using fair maintainable trade as a measure of the value attributed to each element of a PFS.

The practice adopted by the actual occupier in terms of operator’s policy, will generally be taken as indicative of that which would be pursued by the hypothetical tenant in seeking to maximise overall profitability from the site taking due account of competition in the locality.

2. Petrol Forecourt

The petrol forecourt includes the value of the developed forecourt excluding non-rateable plant items.

There are three streams of fuel throughput to consider – Retail, Low Margin Fuel Cards (LMFC) and Bunkered Fuel. The value of the petrol forecourt is determined in accordance with nationally applied scales relating rental value to the fair maintainable throughput of these three streams of throughput.

2.1 Fair Maintainable Throughputs

For the avoidance of doubt, throughput data is provided on Forms of Return (FOR) as:

i) the gross throughput (excluding bunkered fuel), and

ii) the bunkered fuel.

2.1.1 Retail Fuel

Retail throughput excludes LMFC and bunkered fuel throughput.

To determine the Fair Maintainable Retail Throughput (FMRT) the following adjustments are applied where appropriate:

i) Customer Credit Accounts (CCA)

It is understood that customer credit accounts at petrol filling stations are now generally historic, and are declining in number. Where they do exist and are a significant part of the trade, to reflect the fact that the hypothetical tenant would be unlikely to continue with such arrangements, where the CCA represents more than 5% of the retail throughput, the CCA throughput over 5% is reduced by 25%.

Where CCA represents 5% or less of the gross throughput (excluding bunkered fuel), no adjustment is made.

ii) The FMRT should be based on a site with manned opening hours of up to 18 hours per day. Where the site is open and manned in excess of 18 hours a 5% reduction is applied.

Although it may be possible to purchase fuel from the site in excess of 18 hours, and up to 24 hours a day, using automatic pumps, no allowance is applied if the site is not actually manned in excess of 18 hours.

2.1.2 Low Margin Fuel Card (LMFC)

A Low Margin Fuel Card, or Agency scheme, is where a fuel company (mainly oil companies) will enter into contracts to supply fuel to vehicles through the filling station network. The contract is between the fuel card company and the card holder and payment for fuel is made direct to the card company. Once fuel is dispensed at the PFS the card company effectively repurchases the fuel from the retailer at cost price plus a handling charge for dispensing the fuel and dealing with the paperwork. The handling charge is only a proportion of the notional margin available to the retailer for normal retail throughput.

There is no adjustment for opening hours.

2.1.3 Bunkered Fuel

Bunkered fuel is fuel which is stored and dispensed by a forecourt operator, generally on behalf of another operator, for which the forecourt operator receives a handling charge. This handling charge is a much smaller margin than that achieved for retail fuel, or received for LMFC fuel.

There is no adjustment for opening hours.

2.2 Valuation Scales

2.2.1 Retail Fuel (FMRT)

The price per 1,000 Litres (£/000l) to be applied to the FMRT varies according to the level of total FMRT plus the weighted LMFC and the unleaded (UL) price per litre implicit in the retail throughput adopted. This has been developed from the analysis of rental evidence which includes an adjustment for price. Table 1: 2010 sets out the retail fuel scale.

The UL price per litre adopted is the site’s average Catalist price for 2007 and together with the throughputs for that year would be the most up to date trade information available to the hypothetical tenant when determining his rental bid at the Antecedent Valuation Date (AVD) of 1st April 2008. The national average Catalist UL price per litre for 2007 was 94.99p. The pricing policy adopted by the actual site is generally taken as indicative of the policy that would be pursued by the hypothetical tenant in seeking to maximise overall profitability from the site, taking due account of competition in the locality and the price sensitivity of the local market.

LMFC throughput is weighted so that this element of throughput is considered in terms of FMRT. The following equation illustrates how the LMFC throughput is converted to throughput in terms of FMRT:

LMFC throughput x LMFC margin = Weighted LMFC throughput

Notional retail margin

This equation calculates the notional profit available from the LMFC throughput and then relates this to the amount of FMRT required to generate the same level of profit. As the hypothetical tenant would take the LMFC throughput and consider what this equated to in terms of FMRT when making his rental bid.

The weighted LMFC throughput is then added to the FMRT and together with the (UL) price per litre determines the price/000l to be applied.

2.2.2 LMFC

The price per 1,000 Litres (£/000l) applied to LMFC varies according to the level of total FMRT plus the weighted LMFC in the same way as retail fuel. The notional margin does not vary and recognises the fact that a limited handling fee is received for this throughput rather than the full retail margin. Table 2: 2010 sets out the LMFC scale.

2.2.3 Bunkered Fuel

The price per 1,000 Litres (£/000l) to be applied to bunkered fuel throughput is £1.40.

2.3 Manned Kiosk Adjustment

In a relatively small number of instances, a site will have no retail sales from a forecourt shop or the forecourt area itself and will only have a kiosk. Where this kiosk is permanently manned during the site opening hours for the sole purpose of collection of petrol, jet wash and car wash monies, an allowance of 25% is made to the retail petrol value only. This is supported by rental evidence and reflects what the hypothetical tenants approach might be to the fact that all staff costs are covered by the fuel element income and not shared across fuel and a forecourt shop.

3. Forecourt Shop

3.1 Retail Trade Valuation Scales

The value of the forecourt shop, together with any ancillary offices and stores, will be determined in accordance with nationally applied scales relating value to the achievable fair maintainable shop trade (FMST).

The FMST to be adopted is the turnover that a reasonably competent operator would expect the site to achieve from shop sales, excluding VAT. The turnover should also exclude income received from fuel, jet/car wash transactions and monies received from both National Lottery Sales and Paypoint/Payzone facilities.

Where a site achieves only comparatively modest petrol sales an adjustment is made to the retail shop value. The overheads of running the forecourt shop are covered jointly by the income from the fuel throughputs and the shop sales, and where the fuel throughputs are modest, a greater proportion of the overheads fall to be covered by the shop sales, and the hypothetical tenant would adjust his bid accordingly.

This adjustment applies when the total of FMRT plus weighted LMFC throughput is less than 5 million litres.

By way of an adjustment for high turnover shops and following rental evidence, the total shop value is capped at £110,000.

This method of valuation is intended to apply to both forecourts where sales are generated primarily from motorist trade as well as the increasing number of sites trading as a destination shopping venue or convenience store. It is not considered helpful to compare the values attributed to standalone convenience stores with those forming part of a petrol filling station. The rental evidence suggests that there is no direct comparison between the two types of stores and would not be comparing like with like.

Table 3: 2010 sets out the forecourt shop scale of values by reference to turnover and throughput.

3.2 Lottery, Paypoint and Payzone

A relatively low commission is received for National Lottery sales and Paypoint/Payzone facilities compared with the average level of gross profitability achieved on general forecourt shop sales and therefore monies received from operating these facilities are excluded from the FMST. However, the income available would be in the mind of the hypothetical tenant when making his rental bid and should not be completely ignored when arriving at a valuation. Conversion to Rent Factors (CRF) are therefore applied separately and as following:

| CRF | |

| Lottery | 1% |

| Paypoint and Payzone | 0.25% |

- Valeting

The value of automated valeting is derived from two elements; car washes and jet washes.

Like forecourt shops, the valuation of valeting services on the PFS is based on the level of turnover generated.

4.1 Car Washes

Table 4: 2010 sets out the Conversion to Rent Factor (CRF) and value to be attributed to total fair maintainable turnover generated by automated car washing facilities on site. Where this turnover is generated by more than one machine a single 10% reduction is applied to the car wash value.

4.2 Jet Washes

A CRF of 17.5% is applied to the total turnover generated by jet washes.

There is no reduction for more than one machine.

5. Non-forecourt Buildings And Other Sources Of Income

Non-forecourt buildings other than the shop, such as workshops and showrooms and other sources of income, such as from land used as car sales or hand car washes, which are not separately assessed, and which are considered subsidiary to the PFS use, should be valued on the basis of local comparable evidence and included in the valuation.

1. Introduction to the Petrol Filling Station Market

A brief look at a number of aspects of the market will help the valuer to appreciate the state of the market at the appropriate antecedent valuation date. This will enable a better understanding of the difficulties involved in valuing Petrol Filling Stations (PFS) and increase awareness of the factors that are crucial to the valuation process. The Petrol Filling Station (PFS) market in the years leading up to the 1980s was relatively settled and buoyant. Although the number of sites was declining average site throughputs tended to be consistent and on a gradual upward curve. With the exception of the superstores and a few cut price sites, pricing policies were generally on an even level. Post the 1980s the market changed dramatically. The closure of sites accelerated, superstores captured a larger slice of the market, pricing policies became more competitive, and forecourt shops and car washes became more important and profitable. Since the late 2000s the closure rate of PFS has slowed down and by 2015 site numbers appeared to have stabilised.

2. The Number of Sites and Market Share / Average Volumes

2.1 Site Numbers

Throughout the 1990s and 2000s the fuel retailing sector encountered significant site closures. These were due in part to Oil Company rationalisation programmes and closures of smaller, uneconomic sites unable to generate sufficient sales to cover rising operating costs. The expansion of superstores into the industry has also contributed and also the rise of many large independent dealers.

However, research undertaken by Experian Catalist indicates the trend of a shrinking PFS network within the UK is slowing down. Statistics showed an increase of active UK forecourts, in 2014, of 8,616 compared with 8,600 in 2013.

Although only a marginal increase it was the first in recent years and indicated the market was levelling out. 2015 however saw a slight fall to 8,490 sites. Despite these figures it is expected the number of new to industry sites will increase over the coming years with further site closures anticipated for sites unable to survive in a competitive market. Appendix 4 - UK Site Numbers shows the changes in active UK PFS numbers up to 2015.

2.2 Market Share

Leading up to and during 2015 Oil Companies have continued to dispose of large tranches of forecourt numbers that have been acquired mostly by independent groups/dealers seeking to increase their market share. Superstores continue to seek opportunities to increase and develop their stand alone forecourt presence with convenience store offering. Other sites identified by the superstores often sit adjoining or close to their foodstores as the provision of fuel provides an extra selling point for the store. These sites will generally look for annual fuel sales in excess of 10ML, in some cases achieving over 20ML. The statistics below indicate the 2015 UK PFS Fuel Market by ownership (source: Experian Limited 2015).

| Ownership | No. of Outlets | % Fuel Market Share | %Fuel Outlet Share |

| Superstore | 1,429 | 44% | 16.8% |

| Dealer | 5,465 | 33.6% | 64.4% |

| Oil Company | 1,596 | 22.4% | 18.8% |

| Total | 8,490 | 100% | 100% |

The statistics show superstores despite only owning 16.8% of UK fuel outlets, control 44% of overall fuel volumes sold.

The superstores’ market share is expected to increase but at a much slower rate compared with recent years. As Oil Companies continue to dispose of sites this has started to result in a dramatic industry reshuffle, with independent forecourt owners/dealers given opportunities to establish themselves and increase site numbers significantly. By the end of 2015 it is expected independent dealers may occupy approx 70% of UK fuel outlets.

2.3 Average Volumes and Prices

Following the economic downturn in 2008 although oil and fuel prices dropped during the recession, decreased activity and fears of future price increases curbed retail fuel sales in many areas. A 2014 poll by the AA of 18,000 members suggested due to increases in household bills such as gas and electricity, consumers were choosing carefully how they used their cars. This was despite pump prices being at their lowest for three years.

In March 2014, average petrol prices were at their lowest for three years – below 129.5ppl, compared with 139.9ppl a year earlier and a record of 142.48p in April 2012. The early part of 2015 saw prices fall to approx. 110ppl. Appendix 5 - Average UL prices 07-15 shows the average pump prices for UK unleaded fuel between 2007 and the early part of 2015.

The poll also found:

- 57% had adopted fuel-saving driving techniques and intended to stick with them despite lower prices,

- 50% automatically considered restricting car use if their family and personal budgets were squeezed,

- 18% had replaced their car in the last 12 months with a more fuel efficient one.

Many drivers have been gradually switching to more fuel-efficient diesel-powered cars, which has challenged the industry because it means motorists can drive further on less fuel.

Despite these challenges for forecourt operators there are more cars on the road than ever before. This means there are more cars that need filling up, but fewer petrol stations in which to do so.

Appendix 6 - UK Market by Brand shows the 2014 UK market in terms of number of outlets, average volumes and percentage of market share.

3. Oil Company rationalisation / Rise of independent groups/dealers

As already stated leading up to 2015 some of the main Oil Companies disposed of large numbers of forecourts as they sought to rationalise the estate of UK sites they own. This was been in part due to longer term strategies of having what they consider to be the best assets for their business. Oil Company owned site numbers are expected to continue to decrease and may reach less than 1,000 by the end of 2015.

This has led to opportunities for some of the major independent groups/dealers to increase their portfolio significantly in terms of site numbers. It is expected by the end of 2015 a total of 1,400 sites (16% market share) will be owned by the top 4 major independent groups alone. Many smaller independent dealer groups have also acquired some of the former Oil Company sites increasing their numbers.

Recent years have also seen the opening of many first class new to industry sites operated by independent dealers, often with large convenience style forecourt shops and well known food to go options offering the consumer a wide variety of hot and cold products with recognised brands. Independent dealers have invested heavily in sites with many KDRB (knock down and rebuilds) costing well in excess of £2M.

4. Superstores

Leading up to the late 2000s the advent of superstore petrol filling stations radically altered the UK petrol market.

From relatively humble beginnings in the late 1970’s when they had less than 50 sites with only a 1% share of the fuel sales market, the superstores expanded dramatically so that at the end of 1999 they had over 1000 outlets with an estimated market share of 24%. By 2014 the number of outlets stands at approx 1,358 with a market share of 43.5%. Planning policies in the 1980’s were favourable to out of town retail developments, and these policies, together with the food retailers drive for growth, fuelled a very large increase in the number of superstores with fuel forecourts throughout the country. Superstores invested in service stations to attract customers to their stores, as the provision of fuel provided an extra selling point for the store. As each generation of foodstore became more sophisticated, so did the petrol forecourts. The trend with later developments was to place the forecourt so as to maximise its prominence on the site.

The operators initially adopted a policy of significant price discounting as against the prices charged by the majority of oil companies. This was to advertise the value for money ethos of the superstores and so to attract the maximum number of customers. In the late 1980’s and early 1990’s, savings of between 2p and 4p per litre could frequently be enjoyed at a superstore forecourt. Much of the rise in the superstores share of the retail petrol market can be traced back to the summer of 1990 and the start of the Gulf War. As petrol prices climbed steeply on fears of shortages the motorists became increasingly price sensitive, and throughputs at superstore forecourts, where price discounts of up to 4p per litre were typical, increased due to the increased price sensitivity in the market.

Between the end of 1987 and the end of 1992 the number of superstore sites almost doubled, increasing from 236 to 467 and the market share of total volume increased by more than two and a half times, from 4.6% to 12%. This growth continued unabated until the end of 1995, with the number of forecourts increasing to 823 and an increase in the market share to approaching 22%. This expansion and increase in market share was obtained by retailer’s policies of continuing to open new stores and the development of new forecourts on existing sites. Many superstore forecourts were also operating outside store opening hours.

The natural outcome for the superstores of a greater increase in market share against the number of forecourts (together with a market increasing in size, albeit quite modestly) is that average throughputs at superstore forecourts initially increased quite dramatically up to the mid 1990’s. The average 2015 volume of throughput for a superstore currently stands at approximately 11ML p.a. It is considered by some that the superstores share of the fuel market may have reached something of a plateau and future increases in market share are not totally certain, due to factors such as tighter planning restrictions on out of town developments and the rise of major independent dealers.

5. Pricing Policies

In the late 1980’s and early 90’s the oil companies, with a few exceptions, traditionally focused on position and brand image as the keys to maintaining volumes and thereby market share, pricing was generally on an even level. With the advance into the market in the early 1990’s of the superstore operators and their aggressive pricing policy of generally under-cutting the market price, by up to 4 pence per litre, the profile of price in the market was however raised significantly.

Initially however, it was common practice among the oil companies to continue trading at a normal market price after a superstore forecourt opened in competition, with the result that fuel volume was lost. This followed the sound commercial logic that in most cases the cost of reducing the price on the remaining volume would outweigh the additional profit on added volume generated by a price cut. This practice began to change in late 1991 and 1992 when it became more likely that a site closely affected by a superstores new hyper would have endeavoured to safeguard volume by reducing the pump price. Since most superstores serve the local population the level of the reduction was likely to depend on how much the station was in competition for that customer base.

As the oil companies in the main still ran promotions, distinct from most of the superstores who at this time did not run promotions instead concentrating purely on price, it was unusual to find exactly similar prices but those most seriously affected stations may have been at or close to the superstore price, generally around 1 penny above (the price difference representing the average cost of a promotion). Those stations further away but affected nevertheless may have adopted prices a further 1 or 2 pence higher, or remained unaltered depending on the perceived commercial merits as outlined as above.

In determining the relative value of sites it is the combination of price and promotion offered which should be considered. Clearly a site selling 2m litres at 2 or 3p below market price is unlikely to have the same value as another site also selling 2m litres but at the full market price. Similarly a site selling 2m litres with a promotion may not be worth the same as a site selling 2m litres at the same price but without the need for a promotion.

In response many oil companies introduced their own pricing policies such as Pricewatch, Focus on Price, Price Check and Price Aware.

As a result of the above price initiatives, by 1997 the vast majority of oil companies were competing to within at most 1p per litre of the superstores. The superstores responded to Pricewatch by undertaking that they would not be undercut on price. Effectively from the introduction of Pricewatch through to the end of the 1990’s, a degree of equilibrium existed with most brands indistinguishable on price.

Leading up to 2014/15 some superstores continue to offer discounted fuel in the form of loyalty spending bonuses based upon purchases within their food stores. For example a customer may spend £50 in store and subsequently receive 5p a litre off their next fuel purchase. However many independent retailers now also promote similar discounted fuel incentives such as having one or two days a week where fuel is priced lower than normal.

6. Fuel Price Fluctuations

Fluctuations in fuel prices are a common occurrence. For the most part a change in the price of petrol, diesel and other fuels is caused by many factors such as:

- Market forces (inflation, seasonal demands, taxes, cost of crude oil and refined fuel)

- Global events (wars, gas shortages, security threats to oil supplies), and

- New technology (alternative fuel sources, new types of vehicles)

7. Types of Fuel Sold – a brief history

In 1988 over 80% of all fuel sold was 4 Star with Diesel accounting for less than 10% and unleaded approximately 1%.

During the 1990s Increasing environmental awareness coupled with a more favourable rate of duty resulted in significant increases in the demand for unleaded fuel.

By 1993 unleaded fuel accounted for around 45% of all retail fuel sales whereas 4 Star had dropped to around 40%. During the same period diesel sales rose to almost 12.5% and 3 Star and 2 Star fuels had disappeared. By 1998 demand for unleaded fuel significantly outstripped the demand for 4 Star, and diesel sales had steadily increased.

By the end of 2001, unleaded sales accounted for almost 70% of the market with diesel at just over 26%. The late 2000s saw demand for diesel increase and by 2007, annual diesel fuel sales had overtaken unleaded - diesel 25.5BN litres compared with unleaded 24BN litres.

This trend has continued to grow with 2014 annual volumes dispensed showing 27.9BN litres of diesel compared with 17.6BN litres of unleaded. This is due in part to more and more motorists switching to diesel for better fuel economy and lower carbon dioxide emissions. However 2015 media attention regarding certain car manufacturers and emission levels may have an effect on the popularity of diesel cars in the future.

Other products such as bio fuels / LPG (liquid propane gas) continue to be available at many PFS but only account for less than 1% of total UK fuel sales.

8. Fuel Profit Margins

Most independent service station owners, or dealers, enter into ‘supply’ or ‘tie’ agreements with an oil company, undertaking to take supplies only from that company for a fixed period of up to five years. The price that the dealer pays is set on the signing of the agreement and generally is linked to the volume of fuel the site sells, and increasingly to the price of two or three competitor sites in the area (the marker sites). That difference in price represents the retail margin. The level of price competition from the mid 1990’s put substantial pressure upon the margin and rebate deals which oil companies are prepared to offer to independent dealers. Guaranteed price related supply agreements are now available from the oil companies only on the basis of substantially reduced margins.

In some cases higher margins may be available but often these were offset by limited price support. In such cases, for a dealer to retain competitive pricing he has to cut his profit by providing his own discounting, or face a loss in volume, which might in turn mean a loss of rebate for bulk purchase.

The lack of a profitable supply agreement meant many low volume sites became unviable, and at the height of price competition some oil company sites were alleged to be retailing fuel at less than the wholesale purchase price. Consequently there was a sharp increase in the number of site closures and of sites coming onto the market. A number of oil companies have been taking a harder line on the volume level and location at which they will renew supply agreements, leaving some dealers with low volume sites struggling to obtain a new agreement on any terms.

Although margins on fuel have remained relatively robust during 2013/14, many PFS have to rely on margins from other income streams such as shop sales and valeting to supplement profits from fuel.

9. Fuel Duty and Value Added Tax (VAT)

In the United Kingdom, tax on fuel for road use is made up of two elements - fuel duty and VAT. Fuel duty is applied at a fixed amount per litre by fuel type, and VAT is then added as a percentage of the combined total of the cost of the fuel and the fuel duty. Typical costs for a litre of fuel Below shows an example of approximate breakdown costs which make up a litre of Unleaded at 107.9p and Diesel at 114.9p (costs taken from 2015 – source: autofuelfix.com)

Fuel Duty

In the UK a fuel duty exists which is essentially an additional tax that is added to the price of petrol before it is sold. This duty applies to all hydrocarbon fuels such as petrol, diesel, biodiesel and LPG’s that are sold for use in cars and makes up a significant proportion of the price of fuel. As this duty is applied to the price of fuel before VAT, any change to the level of duty will also have an affect on the amount of VAT paid.

Product

The second largest portion of the cost of fuel goes to the companies who supply the crude oil and those who refine it into fuel products like petrol and diesel. The cost of refining diesel is substantially higher than that of petrol which, along with VAT, makes the price charged for diesel higher.

VAT

The petrol purchased at the pumps is subject to VAT which is another addition to the cost of all consumer fuels. The introduction of a new VAT rate of 20% at the start of 2011 saw the price of petrol rise further still.

Retailer

Given these costs the retailer’s margin on fuel dispensed is the lowest of all. The competitive nature of the petrol stations to have the lowest price is also an important factor in the money an operator makes from the price of a litre.

1. Introduction

Valuations of petrol filling stations (PFS) are made on a direct rental basis; suitably adjusted rents being devalued for analysis purposes to a price per thousand litres of maintainable throughput. Analysis is also carried out on turnovers achieved from shop and any valeting with regard had to the Fair Maintainable Trade a PFS can achieve.

An established method of valuation for the variety of PFS exists where rental values are inextricably linked to the trading potential and profitability of a PFS. In the market the assessment of future (genuine) sustainable trading potential, and the profit that will be generated, is one of the fundamental principles - if not the fundamental principle - when valuing a petrol filling station. This method of valuation is applied to the varying types of PFS ranging from low volume sites with a basic forecourt shop offering, to larger volume sites with substantial convenience stores attached.

The approach to PFS valuation has regard to Royal Institute of Chartered Surveyors (RICS) Red Book Professional Guidance on the valuation of PFS.

2. Maintainable Throughput

Maintainable throughput can generally be defined as the volume of fuel sales which is capable of being achieved by the hypothetical tenant, pursuing normal, prudent, trading practices having regard to the trading policies of other, competing, stations in the locality.

The use of actual throughput figures, suitably adjusted for any variation between the trading practices of the actual tenant and those to be envisaged under the rating hypothesis, was approved by the Lands Tribunal in the case of Petrofina (Great Britain) Ltd v Dalby (VO) (1967) RA 146.

3. Disclosure of Throughput on Forms of Return

Following the decision in Watney Mann Ltd v Langley (VO) 1964, 4 RVR 22, it is considered that particulars of actual throughput are information that a VO reasonably believe will assist in carrying out their statutory function.

This statutory function is under the provisions of paragraph 5 of Schedule 9 to the Local Government Finance Act 1988, as amended by paragraph 46 of Schedule 5 to the Local Government and Housing Act 1989 and appropriate questions have been included in the relevant Forms of Return.

Any instance of refusal to complete the questions on Forms of Return relating to throughput should be referred to the National Specialists Unit.

4. Scheme of Valuation

The scheme of valuation for each Rating List involves the application of a scale relating rental value to maintainable throughput and the value arrived at in this way reflects all the usual elements of a petrol filling station forecourt. Additions are required for forecourt shops, car washes and non-forecourt buildings such as showrooms, repair workshops etc.

See the relevant Practice Note for details.

5. Evidence

5.1 Rental Evidence

The primary evidence of value is that of open market rents passing for petrol filling stations, free of any petrol “tie” between landlord and tenant. Assessments are based on the application of a national scheme of valuation, derived from wider rental evidence taken from a variety of PFS types e.g. rural, suburban, independent, oil company, superstore, with forecourt shops varying from small kiosk types to large convenience stores, to certain superstore sites having a small kiosk simply accepting payment for fuel.

5.2 Licences and Tied Tenancies

Evidence from tied rents and licence payments has not been found to be of assistance, other than in the most general terms, in establishing the levels of open market rental value.

5.3 Fuel Supply Agreements

The nature of supply agreements has changed over the last 10 yrs. Previously an operator was able to negotiate a deal with their supplier for a fixed period e.g. 5 years. In return they could achieve guaranteed minimum margins, price support, and extended credit terms.

In many cases these have been replaced by target margins and margin-sharing plus ‘Platts’ related deals.

Platts who are a leading price reporting agency for the oil market, set the benchmarks for oil prices using information provided by oil companies.

In some cases ‘Solus’ agreements still exist whereby terms of supply are negotiated between the oil company and the occupier of the PFS. These agreements last for five or less years and, in return for exclusive supply contracts, the oil companies are frequently prepared to offer retailers discounts or rebates on their wholesale prices, low interest or interest free loans, capital grants, or free pumps and equipment

5.4 Exclusion of Tied Tenancies and Licences from Analysis

All Forms of Return should be carefully examined at the analysis stage to distinguish those which relate to genuine open market rents from those relating to tied tenancies or licences. The following features of licences or tied tenancies should assist in drawing the necessary distinctions:

a. The agreement will be for a short term, typically 3 years. b. The landlord or licensor will be an oil company. c. The petrol pumps and other plant will belong to the oil company and be included in the letting or licence. d. The operator will be obliged to purchase all petroleum products from the oil company landlord, or licensor. e. The landlord or licensor will frequently pay the rates. f. The rent or licence payment may include an amount which increases with petrol throughput.

5.5 Rental Analysis

Open market rents should be checked to ensure they equate to the terms of Rateable Value before further analysis is carried out. The rental value of any bunkered fuel income, low margin fuel card income, non-forecourt buildings, such as showrooms and workshops, non-rateable plant, car-washes and forecourt shops should then be stripped out at appropriate levels. The resultant figure will represent the apportioned value of the petrol forecourt, the kerbs and settings for petrol pumps, the canopy and rateable tanks together with their pits and chambers.

Analysis should reflect elements of fuel and shop that are of lesser value than full retail such as bunkered fuel, low margin fuel cards and lottery, paypoint income respectively. Any PFS rental analysis should always be carried out in consultation with the NSU PFS CCT lead.

6. Valuation of Forecourt

6.1 Valuation

Valuation will be in accordance with a national scheme derived from rents analysed on the foregoing basis. Additions to valuations made in accordance with the scale will be required for all other rateable parts of the hereditament, such as forecourt shops, the rateable parts of car washes and non-forecourt buildings. Any income from bunkered fuel and low margin fuel cards will also need to be reflected in the valuation.

Because of the complexities of the petrol filling station market it is important to have a clear understanding of the operating practice of all the sites within a given locality.

Valuers should consider all available evidence of throughputs, pricing policies and be aware of all material changes of circumstances (MCC’s) which may have affected a particular site and the date the MCC occurred.

The starting point of the valuation is to establish a maintainable throughput which will determine the value to be attributed to the forecourt and will also affect the value attributed to the forecourt shop. The maintainable throughput is also crucial for the adjustments to be made for such factors as low margin fuel card or bunkered fuel sales.

The basis of assessing maintainable throughput will depend on the trading conditions leading up to and at the AVD. The definition may therefore vary from revaluation to revaluation. Guidance on any assumptions that should be made in the assessment of maintainable throughput will be set out in the appropriate Scheme Practice Notes.

Small variations in the maintainable throughput can have a major impact on the final rateable value because throughput is valued on a sliding scale and it can impact on the value adopted on the forecourt shop. Great care is therefore required to ensure that the maintainable throughput is correctly quantified. Valuers will need to study the combination of 3 years volumes on the subject and competing forecourts, the pricing policy which existing during that time, and any MCCs in the locality to determine the maintainable throughput.

The throughput of all fuels sold during the year preceding the AVD should be the starting point in determining the maintainable throughput, but adjustments may be required where an MCC has taken place and its impact is not reflected in those volumes. Adjustments may also be required if that throughput, or any other throughput that is being considered has been influenced by a cut price, low price or high price policy that appears out of the ordinary.

If there are no subsequent MCCs to take into account and the site was trading on the basis defined by the maintainable throughput in the relevant Practice Note, the throughput for the year preceding the AVD may be adopted as being the maintainable throughput of the site. This is however subject to the proviso that all assessments must be capable of being justified by comparison.

If a FOR has not been returned or does not include a minimum of 2 years throughput i.e. in cases of new sites opening or changed ownership/occupation, the maintainable throughput should be estimated having regard to any historic throughput information available for the site or by comparison with other sites in the locality.

6.2 Rateability of Plant and Machinery

The rateability and valuation of plant and machinery are dealt with in RM:4:3.

Petrol pumps are not specified in any of the classes in The Valuation for Rating (Plant and Machinery) Regulations (1989, 1994, 2000), and are not therefore rateable.

Tanks are rateable under Class 4 of the Plant and Machinery Regulations subject to the exceptions under (a) to (e) thereof. In the case of Shell Mex and BP Ltd v Holyoak (VO) (1959) HL 52 RIT 134 it was held that tanks, each of 3,000 gallons capacity and 4.1m long, 2.1m in diameter and 2 tons in weight, enclosed in chambers of brick and concrete construction but resting by their own weight, were not in the nature of structures and therefore did not form part of the rateable hereditament. To be rateable as a structure the tank must therefore be so substantially attached to the surrounding chamber or compartment as to become one physical entity with it, e.g. by being encased in concrete, as in the case of Shell Mex and BP Ltd v James (VO) [1961] LT 1 RVR 106. The underground chambers or compartments themselves are, of course, structures and, being identifiable under class 4, are rateable under the Regulations.

7. Factors Affecting Throughput or Value

7.1 General