CFM96780 - Interest restriction: joint ventures: interest allowance (non-consolidated investment) election: example 1: opaque JV

Link to the structure diagram for this example

{kind=link}

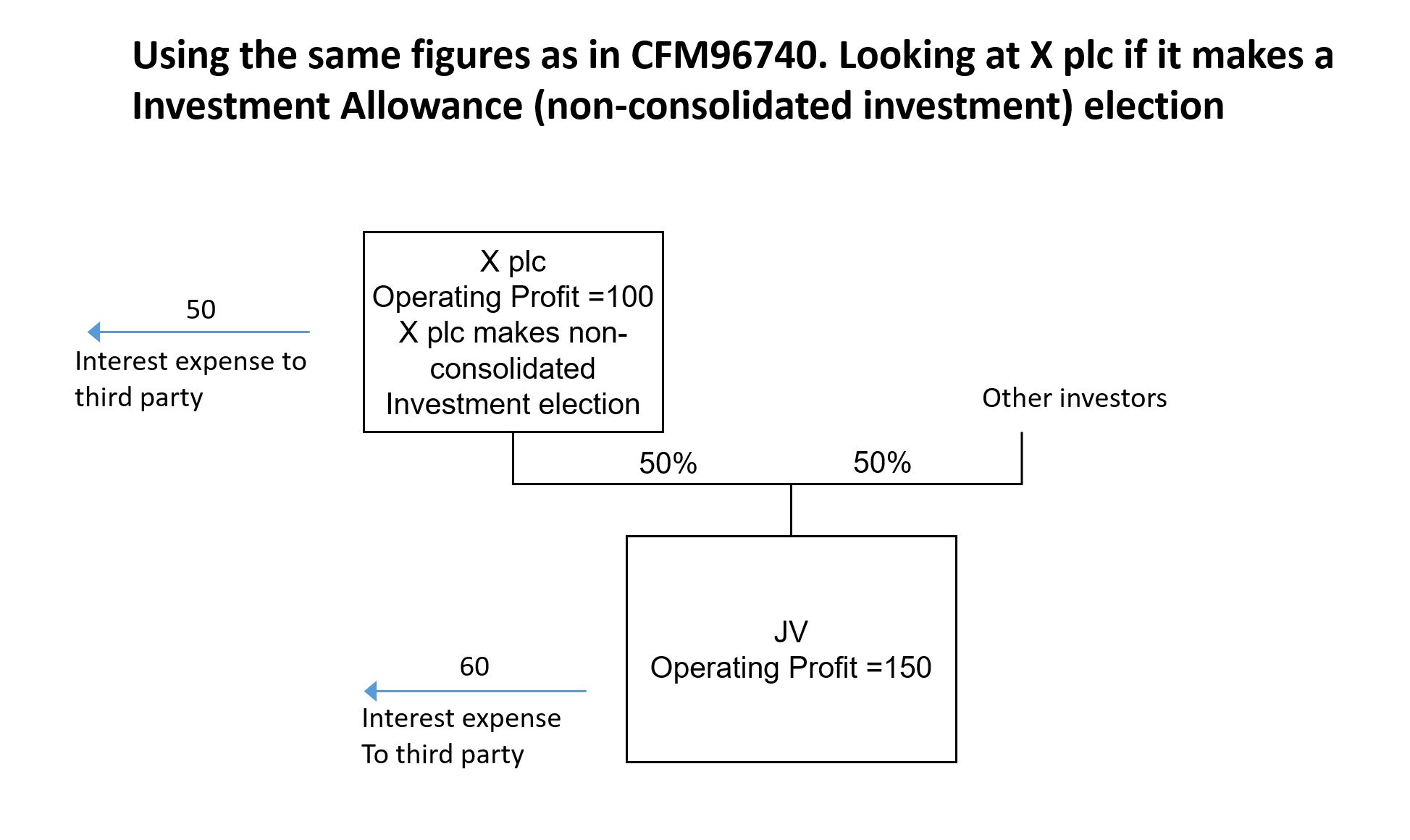

Here the same figures from the example at CFM96740 are used but consider that X plc has now made an investment allowance (non-consolidated investment) election. Note that qualifying net group-interest expense is referred to as QNGIE in the calculation.

| Accounts | X plc | JV | X plc Group |

|---|---|---|---|

| Operating profit | 100 | 150 | 100 |

| 3rd party interest expenses | - 50 | - 60 | - 50 |

| Share of profits of JV | - | - | 45 |

| Profict Before Tax | 50 | 90 | 95 |

- X plc group share of profits from JV - 50%

| Calculation of QNGIE | X plc Group |

|---|---|

| QNGIE in X plc group ( pre-election) | 50 |

| Share of JV QNGIE | 30 |

| Total QNGIE - (A) | 80 |

| Calculation of group -EBITDA | X plc Group |

|---|---|

| Group - EBITDA of X plc group ( pre-election) | 145 |

| Reduction in group - EBITDA | - 45 |

| Increase in share of group - EBITDA from JV group -EBITDA | 75 |

| Group - EBITDA - (B) | 175 |

- Group ratio with election - 46% - ( A/B)

| Interest allowances | X plc |

|---|---|

| Tax - EBITDA | 100 |

| X plc group ratio | 46% |

| Interest allowance | 46 |

| Net tax- interest expense for X plc group | 50 |

| Less interest allowance | - 46 |

| Restriction | 4 |

With the election X plc is now able to calculate a group ratio of 46%. If this is compared to the example in CFM96740 when the election has not been made, this is a significant increase and leads to a reduction in the interest restriction.