CFM96940 - Interest restriction: joint ventures: qualifying infrastructure company JV: example of interaction of S444 with both S427 and S401

Link to the structure diagram for this example

{kind=link}

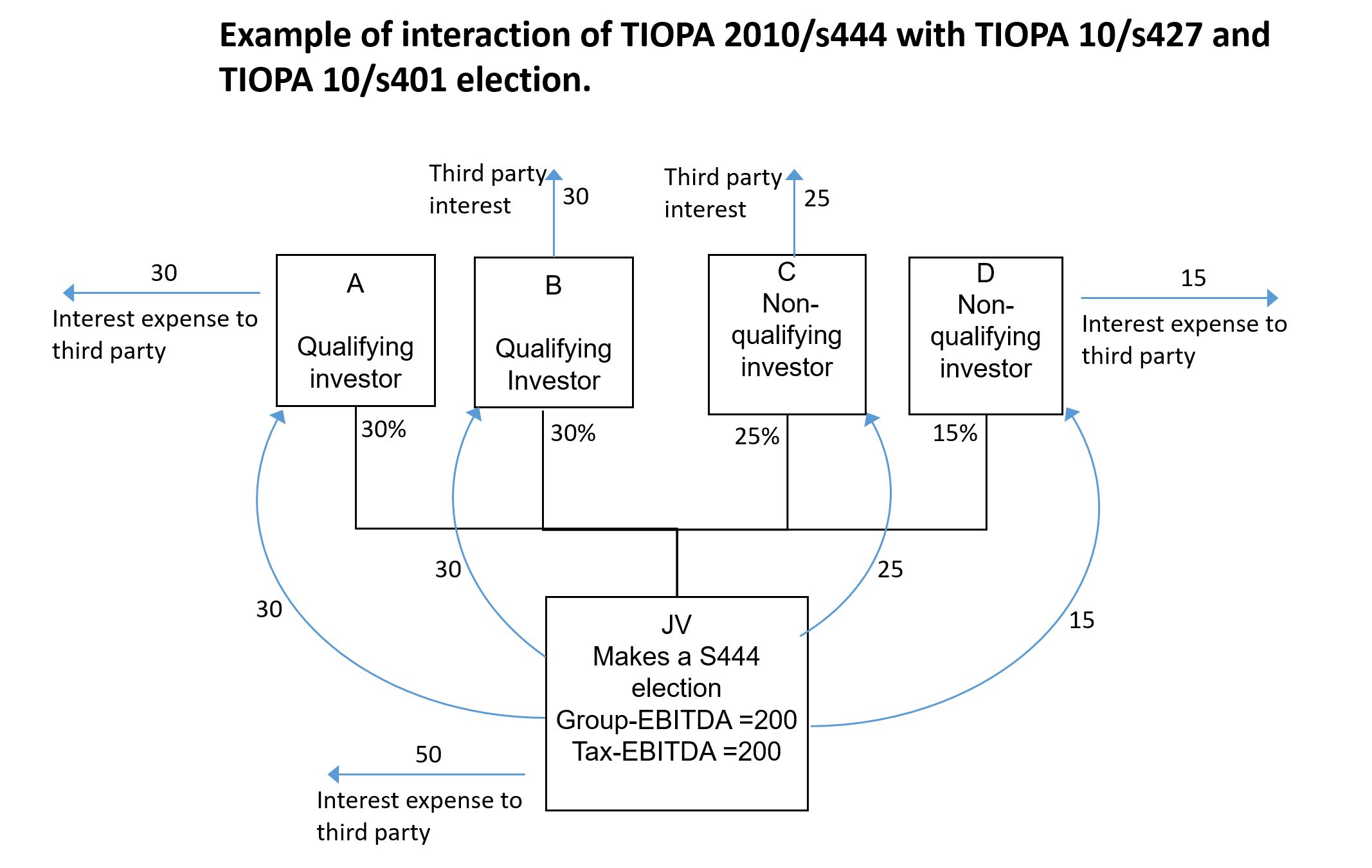

Here the investors raise third party debt and lend this on to JV. This lending is done in proportion to their shares as required by TIOPA10/s444(1)(d). The JV also raises third party debt. Investors A and B are qualifying infrastructure companies. Investors C and D are non-qualifying infrastructure companies. The only activity in A, B, C and D is the holding of the JV and the taking out of third party loans and the on-lending of these loans to JV.

The 60 of interest paid from JV to investors A and B is an exempt amount by virtue of TIOPA10/s438(3)(b) as in each case the creditor is a QIC. Only the qualifying proportion of the 50 that is paid by JV to a third party is an exempt amount. Applying TIOPA10/s444(5)(b) and (6) this is 60% x 50 = 30. Therefore the total exempt amount is 60 + 30 = 90. This amount is therefore excluded from tax-interest. In addition, this amount is not included in adjusted net group-interest expense or qualifying net group-interest expense.

The interest of 40 which is paid to investors C and D is included with tax-interest expense. It therefore is also included in the adjusted net group interest expense for the JV group. However as this interest is paid to related parties it is not qualifying net group-interest expense. The balance of 20 paid by JV to the third party is included as adjusted net group-interest and qualifying net group-interest.

Overall in this example the tax-interest expense is 20 + 40 = 60. Likewise, the adjusted net group interest is 60 and the qualifying net group-interest expense of the JV group is 20.

Restriction in JV if no blended election made

If JV does not make a group ratio (blended) election then its group ratio will be 20/200 = 10%. As this is less than 30% the JV has to rely on the fixed ratio rule. The tax-EBITDA of JV is reduced to the non-qualifying proportion which is 40% x 200 = 80.

The interest allowance is calculated by the fixed ratio rule is therefore 30% x 80 = 24. Therefore there would be an interest restriction of 36.

Making a group ratio (blended) election in isolation

Applying TIOPA10/s444(2) excludes the qualifying investor for the purposes of calculating the blended group ratio election. However without investors C and D making a non-consolidated investment election the blended election would not reduce this interest restriction. This is because both C and D do not have any qualifying net group-interest expense. In C the 25 of interest expense paid to the third part is netted off by the 25 of interest income received from JV. The situation in D is similar with the interest expense of 15 netted off by the interest income of 15. Therefore B and C have group ratios of nil without the benefit of the non–consolidated investment election.

C and D make a non-consolidated investment election

We now assume that C and D each make an interest allowance (non-consolidated investment) election or are treated as making such an election (under s403(2)).

Investor C

Applying TIOPA10\s444(3) means that we ignore the qualifying investor’s share of the profits and the interest income from JV. This means for the purposes of section 427 investor C just has qualifying net group-interest expense of 25. This is the third party interest. JV has qualifying net group-interest expense of 20 (see above). Applying TIOPA10/s427(5) and s444(3) means that C takes the appropriate proportion of this qualifying net group interest. This qualifying net group interest expense of 20 is then divided between the non-qualifying investors.

Applying TIOPA10\s427(6) means that B takes the appropriate proportion of the JV’s group-EBITDA. The total group-EBITDA of JV is calculated by applying TIOPA10\s444(10). This is therefore 40% x 200 = 80 (the non-qualifying proportion of the original 200).

This group-EBITDA of 80 is then divided between the non-qualifying investors. C has a 62.5% share (25/40) and D has a 37.5% share (15/40).

Additional qualifying net group interest in C = 62.5% x 20 = 12.5 which gives a total qualifying net group-interest expense of 25 + 12.5 = 37.5.

Group-EBITDA for C = 62.5% x 80 = 50.

Which gives a group ratio for C = 37.5/50 = 75%.

Investor D

The same treatment applies to D as with investor C.

Additional qualifying net group interest in D = 37.5% x 20 = 7.5.

Investor D has qualifying net group-interest expense of 15 + 7.5 = 22.5.

Group-EBITDA of D = 37.5% x 80 = 30.

Group ratio of D = 22.5/30 = 75%.

JV company

Now apply to the blended group ratio calculation of JV.

Using the group ratios of C and D after applying the non-consolidated investment allowance election, the blended group ratio of JV = (62.5% x 75%) + (37.5% x 75%) = 75%.

This blended group ratio is applied to the tax-EBITDA so interest allowance = 75% x 80 = 60. Therefore there is no interest restriction and the remaining tax-interest can be deducted.