CFM97320 - Interest restriction: public infrastructure: limited recourse of financial instruments

TIOPA10/S438(4),(5),(6)

For a tax-interest amount to be excluded under the infrastructure rules, the recourse of the creditor must be limited to ‘relevant infrastructure matters’. This means if a qualifying infrastructure company fails to perform its obligations under the instrument, the creditor’s recourse is limited to:

- Income of a QIC;

- Assets of a QIC;

- Shares in a QIC; or

- Debt issued by a QIC.

It does not matter whether the recourse relates to the company that has entered into the particular financial instrument, or another QIC.

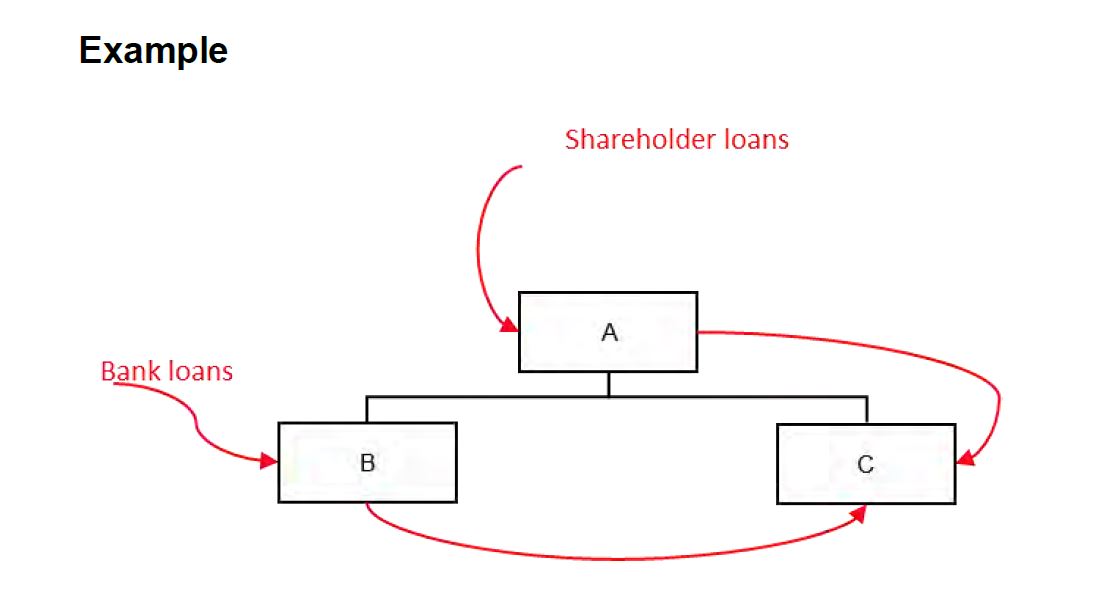

Example 1

Link to the structure diagram for this example

{kind=link}

Company A owns shares in Company B and Company C.

Company C was incorporated to hold and undertake a PFI contract to construct a school. It borrows from its only shareholder, Company A, and its sister company, Company B. It meets the conditions in S433 and has elected to be a QIC.

Company B acts as a finance company, and borrows from a bank to lend to Company C on back to back terms. Company B meets the conditions in S433 (by virtue of its only income and assets deriving from its loan to Company C) and has elected to be a QIC.

Company A borrows from its shareholders, X and Y, to fund its lending to Company C. It also meets the conditions in S433 (by virtue of its only income and assets deriving from its shareholdings in Company B and Company C and its loan to Company C) and has elected to be a qualifying company.

Company A and Company B grant the bank recourse over the shares and loan notes issued by Company C, held by Company A. This is recourse limited to ‘relevant infrastructure matters’ i.e. shares in and debt issued by QICs.

Company A borrows from its shareholders, who are related parties. Tax-interest amounts will therefore in any case only by excluded if it is a qualifying old loan relationship, as well as if the creditors' recourse is limited to relevant infrastructure matters. The shareholders recourse is limited to the assets of Company A on winding up i.e. the assets of a QIC, again ‘relevant infrastructure matters’.

Example 2

Company X (which meets the conditions to be a QIC) has borrowed funds from a third-party lender, with security given over not only Company X shares but also the shares of its sister company, Company Y. However, Company Y is currently dormant.

A dormant company is unable to be a QIC because without an accounting period, it cannot meet S433(d).

When applying S438(4) in respect of Company X’s position, the recourse of the third-party lender over Company Y’s shares must be considered, and there is no insignificant proportion carve out. Therefore, the inclusion of Company Y within the security net could prevent Company X from obtaining the benefit of the public infrastructure rules.

Guarantees

Typically any guarantee, indemnity or other financial assistance provided in favour of the creditor should be taken into account for the purposes of ascertaining whether the recourse of the creditor is sufficiently limited. However, there are particular provisions which allow the effect of guarantees to be disregarded in certain circumstances.