BLM80315 - Sale of lessor companies and similar arrangements: establishing change of ownership: identifying a qualifying change in ownership

CTA2010/S393

There is a qualifying change in ownership whenever there is a relevant change in the relationship between company A (the lessor company) and its principal company. In essence, there is a relevant change when the 75% subsidiary relationship is broken. A change from (say) 100% ownership to 75% ownership does not trigger Schedule 10.

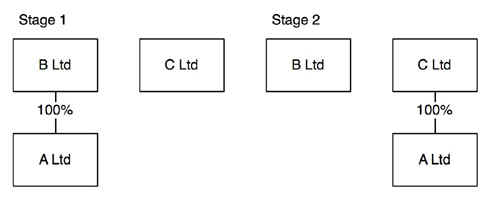

The simple example of the direct sale of a lessor company is illustrated in Example 1.

Use this link to view Example 1

{kind=link}

Here, the principal company of A Ltd is B Ltd. B Ltd sells all shares in A Ltd to C Ltd. The sale of shares means that A Ltd stops being a 75% subsidiary of B Ltd. There is a relevant change in the relationship between company A and its principal company.

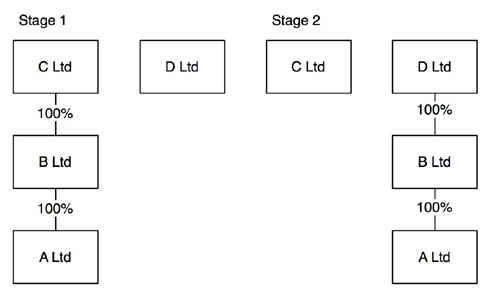

Where the principal company does not hold shares directly in A Ltd there is a relevant change in the relationship between company A and its principal company whenever any of the links of the chain that establish the relationship between A and its principal company are broken because any company in the chain ceases to be a 75% subsidiary of another company. This is illustrated by example 2.

Use this link to view Example 2

{kind=link}

The principal company of A Ltd is C Ltd. C Ltd sells all of the shares in B Ltd to D Ltd. No shares in A Ltd are sold.

The chain of 75% relationships runs from A Ltd to B Ltd and B Ltd to C Ltd. There is a change in the relationship between B Ltd and C Ltd so that B Ltd stops being a qualifying 75% subsidiary of C Ltd. This change is a relevant change in the relationship between A Ltd and C Ltd as a principal company.