BLM80325 - Sale of lessor companies and similar arrangements: establishing change of ownership: consortia: relevant changes in relationships

CTA2010/S394

Special rules are needed to deal with changes in consortium relationships. These changes might be used to shift access to losses.

{kind=link}

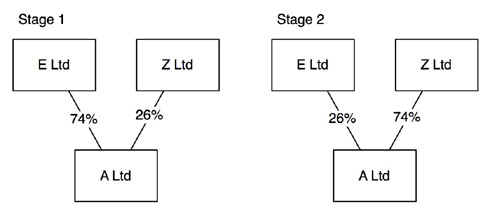

In this example A Ltd, the lessor company, is owned 74% by E Ltd and 26% by Z Ltd. If E Ltd is a member of a profit making group 74% of the early tax losses of A Ltd can flow to the E group. When A Ltd moves into profit E Ltd sells shares in A Ltd to Z Ltd so that after the sale A Ltd is owned 74% by Z Ltd and 26% by E Ltd. If Z Ltd is a member of a loss making group 74% of the tax profits of A Ltd can be absorbed by group relief flowing from the Z group.

The legislation treats this fall in the shareholding of E Ltd in A Ltd as a ‘relevant change in the relationship’ so that there is a qualifying change of ownership in relation to A Ltd.

There is a ‘relevant change in the relationship’ whenever the ‘ownership proportion’ is less at the end of the day than it was at the start of the day.

The ownership proportion is the lesser of:

- The percentage of the ordinary share capital of company A owned by company E;

- The percentage to which company E is beneficially entitled of any profits available for distribution to equity holders of Company A;

- The percentage to which company E would be beneficially entitled of any assets of Company A available for distribution to its equity holders on a winding up.