BLM80555 - sale of lessor companies and similar arrangements: calculating the income amount: adjustments to the basic amount: consortium relationships

Section 405 CTA2010

There is an adjustment to the basic amount where the qualifying change of ownership is a result of s394. That is that the lessor company is a consortium company or a 75% subsidiary of company owned by a consortium and the ownership proportion is less at the end of the day than it was at the start. See BLM80325.

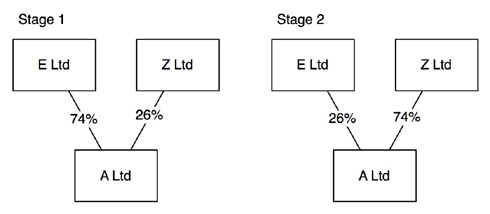

Example: change in ownership proportion

{kind=link}

In this example the ownership proportion of E Ltd falls from 74 to 26. The appropriate proportion is found by deducting the ownership proportion at the end of the day from that at the start of the day to give an appropriate proportion of 48%.

Where a consortium member leaves a consortium altogether there will be no ownership proportion at the end of the day. Sub paragraph (4) limits the income amount to the appropriate proportion of the basic amount that reflects the ownership proportion at the start of the day.