BLM81035 - Sale of lessor companies and similar arrangements: partnerships: identifying a qualifying change in the ownership of a partner company

Section 425 CTA2010

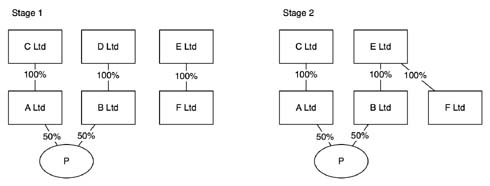

A change in ownership can be achieved by a change in the ownership of a partner company rather than by a change in the partner’s share in the partnership business.

Example

{kind=link}

In this example the partnership sharing arrangements remain constant but partner B Ltd is sold to E Ltd. This change is a ‘qualifying change in ownership’ as defined in sections 392 to 398, see BLM80305.

The principal company of B Ltd is a 75% subsidiary of D Ltd. D Ltd is the principal company of B Ltd. B Ltd ceases to be a 75% subsidiary of D Ltd and this is a relevant change in the relationship, see BLM80315.