BLM81095 - Sale of lessor companies and similar arrangements: partnerships: amount of income - change in ownership of partner company

Section 429 CTA2010

Where there is a change in ownership of the partner company the income amount must reflect not only the change in the ownership of the partner company but also its interest in the partnership business and any changes in that interest. This is achieved by limiting the amount of the income.

Example 1

To calculate the income amount:

Step 1 - find the basic amount as if the company were the partner company in section 421. This is the amount found by the formula PM - TWDV.

Step 2 - adjust this amount if the sale is other than an outright sale to reflect the appropriate percentage change in the ownership of the company in line with sections 404 to 406 (company becoming a member of a consortium). See BLM80540.

Step 3 - limit this amount according to the circumstance of the change:

- If the company’s interest in the business remains constant then the amount is limited to the appropriate percentage share in the business.

- If the company’s interest in the business also changes then the limit is the appropriate percentage share in the business at the end of the day.

Examples 2 to 4 follow.

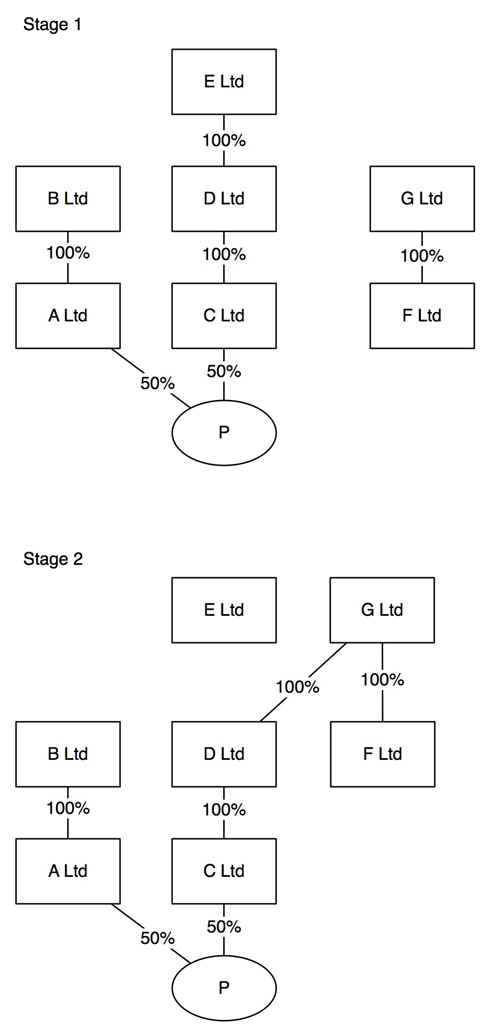

Example 2: income amount - change in ownership of partner

{kind=link}

In this example there is a qualifying change in the ownership of C Ltd.

Step 1

Calculate the basic amount. If PM - TWDV = 1000 then the basic amount is 1000.

Step 2

The sale is an outright sale of C Ltd so there is no need to make an adjustment in line with sections 404 to 406. The basic amount remains at 1000.

Step 3

There is no change in the company’s interest in the business and so the appropriate percentage is the percentage share in the profits on the relevant day - 50%.

The charge is therefore 500.

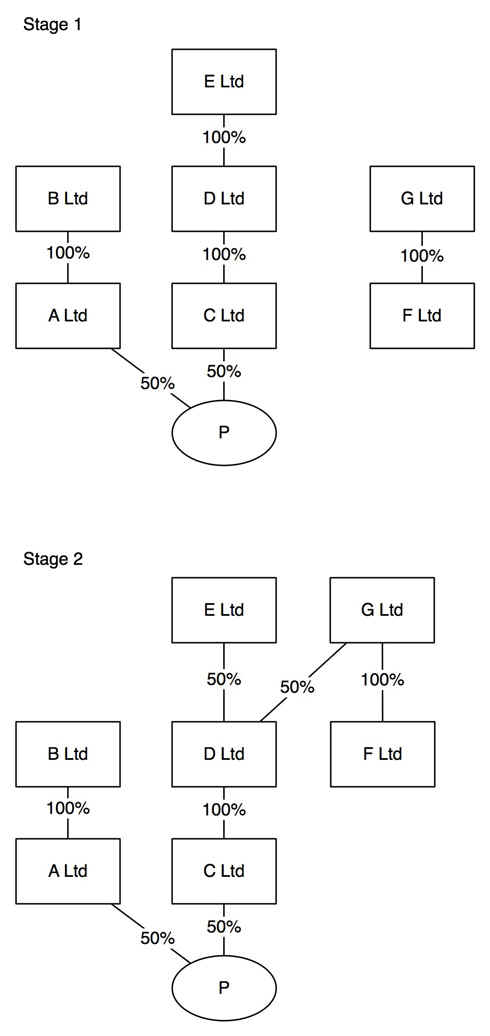

Example 3: income amount - change in ownership of partner

{kind=link}

In this example there is a qualifying change in the ownership of C Ltd.

Step 1

Calculate the basic amount.

If PM - TWDV = 1000 then the basic amount is 1000.

Step 2

The sale is not an outright sale of C Ltd. D Ltd becomes a consortium company. The relevant fraction at the end of the day is 50% so an adjustment is made to the basic amount in line with section 405 CTA 2010to give an amount which is the appropriate percentage 100 - 50 = 50%. The amount is now 500.

Step 3

There is no change in the company’s interest in the business and so the appropriate percentage of the amount now calculated is the percentage share in the profits - 50%.

The income amount is therefore 250.

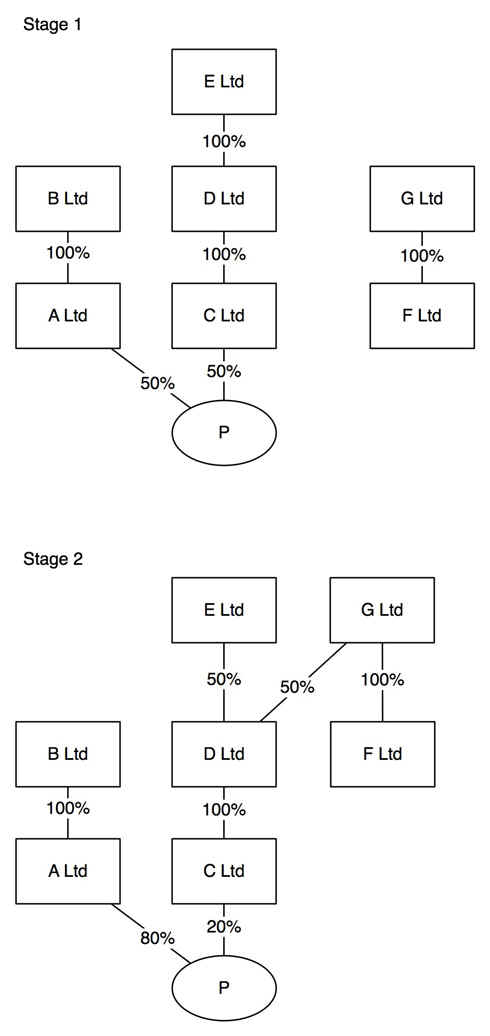

Example 4: income amount - change in ownership of partner + interest in business

{kind=link}

In this example there is both a qualifying change in the ownership of C Ltd and a change in the interest of C Ltd in the partnership business. The change in the interest of C Ltd in the partnership business generates an amount of income and expense in addition to that generated by the qualifying change in the ownership of C Ltd.

Step 1

Calculate the basic amount.

If PM - TWDV = 1000 then the basic amount is 1000.

Step 2

The sale is not an outright sale of C Ltd. D Ltd becomes a consortium company. The relevant fraction at the end of the day is 50% so an adjustment is made to the basic amount in line with section 405 CTA 2010 to give an amount which is the appropriate percentage 100 - 50 = 50%. The amount is now 500.

Step 3

There is also a change in the company’s interest in the business and so the amount is limited to the appropriate percentage of the amount now calculated. The appropriate percentage is the percentage share in the profits at the end of the day- 20%.

The income amount is therefore limited to 20% of 500 = 100.

The change in the interest of C Ltd in the partnership generates a further income amount.

If PM - TWDV = 1000 then the basic amount is 1000. This is adjusted to reflect the fall in the company’s relevant percentage share: 50 - 20 = 30%. A further income amount of 1000 x 30% = 300 is brought into charge.

The total income amount arising as a consequence of this transaction is therefore 100 + 300 = 400. This reflects the change in the economic ownership of the business by the D group. At stage1 D Ltd owned 50% of the business, at stage 2 D Ltd owns only 10% of the business through its 50% holding of the 20% partner. This overall fall of 40% is reflected in the income of 400.