CDSSG08020 - Step-By-Step Guide, Step 3 - the Commodity Code and the Customs Declaration (DEs 6/14 - 6/17): Commodity Codes and Taxes

The taxes that apply to the goods being declared can be identified by using the UK Global Tariff or NI Online Tariff on Gov.UK.

The correct Online Tariff must be used according to:

- where the goods are being declared (in GB or NI)

- and whether the goods are ‘at risk’ of moving on to the EU or not.

The following table indicates, for goods being imported to Northern Ireland, which:

- Control measures (documentary requirements) will be applied and

- Which duty rates will be applied

Which Tariff Measures apply in Northern Ireland?

| Status of the goods | Tariff Measures Applicable |

|---|---|

| NIDOM | EU control measures applied only |

| NIIMP | UK and EU control measures applied |

Which Customs Duty applies in Northern Ireland?

| AI Code | Duty Calculation |

|---|---|

| NIDOM with NIREM | No duty calculated |

| NIDOM without NIREM | Duty calculated based on EU duty rates |

| NIIMP with NIREM | Duty calculated based on UK duty rates |

| NIIMP without NIREM | Duty calculated based on EU duty rates |

Failure to use the correct tariff may result in incorrect assumptions being made on revenue charges and documentary requirements being omitted from the declaration.

Once you have found the specific commodity code to be declared, you can identify the taxes that apply by completing the 4-steps outlined below:

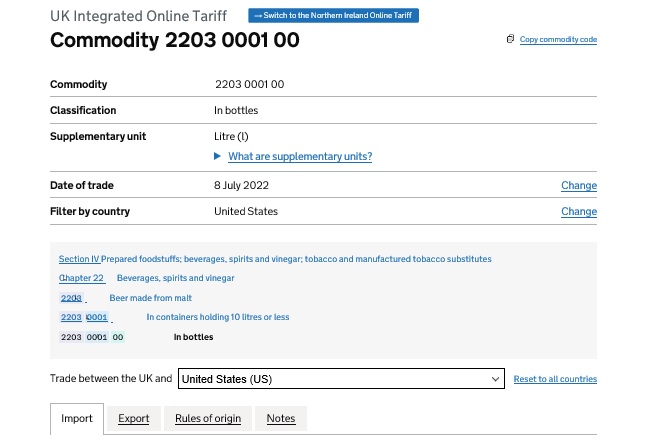

Step 1: Select the Import Tab

Once the Commodity Code has been identified and the summary page for the code opened, the Imports Tab should be selected to view information on what taxes and duties apply to the goods.

Use this link to view an example of a commodity code’s summary page with the option to select Import details or Export details using the appropriate tab

{kind=link}

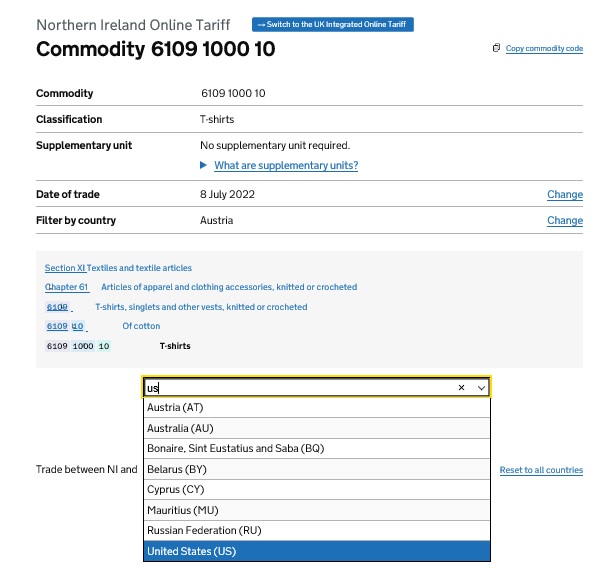

Step 2: Select the country of origin for the goods

The Commodity Code’s information can be filtered to only show details for a particular country. This can help to identify any duty rates or requirements for the chosen country of origin for the goods.

Use this link to view a screenshot of the Country filter drop down box

{kind=link}

Selecting the appropriate country from the drop down list filters the information on the measures to those which apply to the chosen country only.

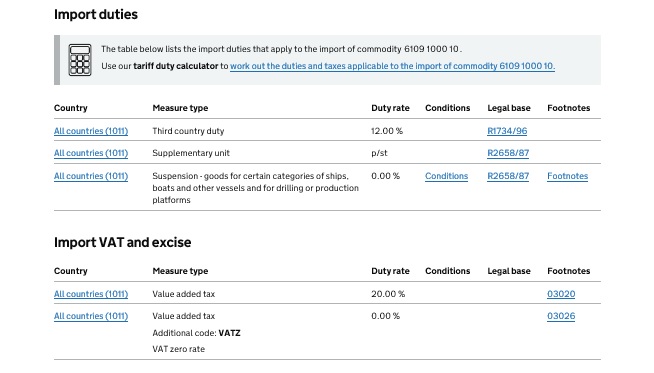

Step 3: Identify any taxes that apply to the goods

It is important to ensure you know which country of origin is being declared as this may affect the rate of duty that applies. It is also important to ensure you are in the correct Online Tariff according to the ‘at risk’ status of the goods for Northern Ireland or the UK Global Tariff if the goods are being imported into GB.

Any preferences claimed will required documentary evidence to be declared in support of the claim.

Please see CDSSG08030 and CDSSG12000 for more details.

Use this link to view an example of a commodity code’s import duties and VAT rates

{kind=link}

Step 4: Identify the correct Tax Type Codes

Once the taxes that apply have been identified, the declarant needs to check these taxes against Appendix 8: DE 4/3 Tax Types to identify the codes to be declared in DE 4/3 for each tax that applies.

Please note Third Country Duty is referred to In Appendix 8 as Customs Duties.

Where there is no tax to be paid or secured for a given tax type, this data element may be left blank.

The tax type only needs to be declared where revenue has to be paid or secured on the declaration or CCR.

Additional revenue charges may be due on some goods moving between GB and NI depending on their ‘at risk’ status. See the Northern Ireland Supplement for details.