BLM80130 - Sale of lessor companies and similar arrangements: business of leasing plant or machinery: adjustments to the balance sheet figures: example 1 of 2

Example 1: Assets transferred on relevant day:

{kind=link}

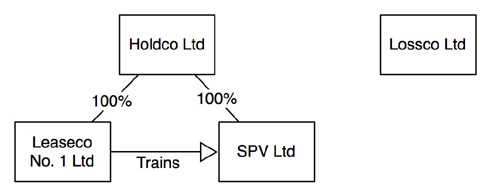

Holdco Ltd is the holding company of a leasing group. It sets up SPV Ltd on 1 December 2010.

The balance sheet shows £100 share capital £100 cash.

Holdco Ltd agrees to sell SPV Ltd to Lossco Ltd on 15 December 2010.

Holdco Ltd agrees that on 15 December and prior to the sale it will transfer 2 trains subject to finance leases with a value (net investment) of £10m into SPV Ltd from another wholly owned subsidiary, Leaseco No 1 Ltd.

The leases on these trains are about to become tax profitable. The price paid by Lossco Ltd reflects the transfer of the assets.

The relevant day is 15 December 2010.

At the start of that day SPV Ltd has no plant or machinery assets on its balance sheet and is therefore not carrying on a business of leasing plant or machinery. But, by adjusting the opening balance sheet figures to include the leased trains the picture is changed.

SPV Ltd has £10m of plant or machinery assets subject to leases. The company is carrying on a business of leasing plant or machinery.