BLM80135 - Sale of lessor companies and similar arrangements: business of leasing plant or machinery: adjustments to the balance sheet figures: example 2 of 2

Example 2: Consortia

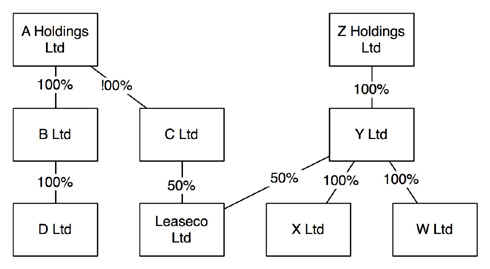

In this example Leaseco Ltd is a consortium company.

{kind=link}

The members of the consortium are C Ltd and Y Ltd.

Y Ltd sells its shareholding in Leaseco Ltd so that there is a qualifying change of ownership in relation to the holding of shares by Y Ltd.

The associated companies of Leaseco Ltd are

- Y Ltd as it is the ‘relevant’ consortium member at the start of the day (the consortium member in relation to which the change of ownership occurs), and

- all the members of the Z Holdings group of companies (the associated companies of Y Ltd).

The adjustment required by section 389 CTA2010 ensures that a group cannot set up an SPV that is a consortium company that owns no leased assets, contract to sell the company and then bundle leased assets held elsewhere in the consortium member’s group into the departing company on the day of sale.

In this example the Z group could set up a consortium company, Leaseco Ltd, and transfer leased assets into Leaseco Ltd on the day of the sale. At the start of the day Leaseco Ltd has no leased plant or machinery assets on its balance sheet and is therefore not carrying on a business of leasing plant or machinery. But, by adjusting the opening balance sheet figures to include the assets transferred into the company by the Z group the picture is changed.